Ethereum is currently trading below its 'fair value' according to most models on the ETHVal dashboard created by CEO Hashed Simon Kim.

As of the end of November, the composite 'fair value' on ETHVal gives approximately +50-60% upside to the market, and the median across models is also significantly higher than the spot price.

ETHVal attempts to answer a simple but uncomfortable question:

"How much should ETH be worth if we look not at memes and sentiment, but at the fundamental metrics of the network?"

So, friends, I will go through 10 key models that mostly show Ethereum being undervalued, and then two that, on the contrary, say: “ETH is too expensive.” For each one, how it works, what its strengths are, and where its weaknesses are.

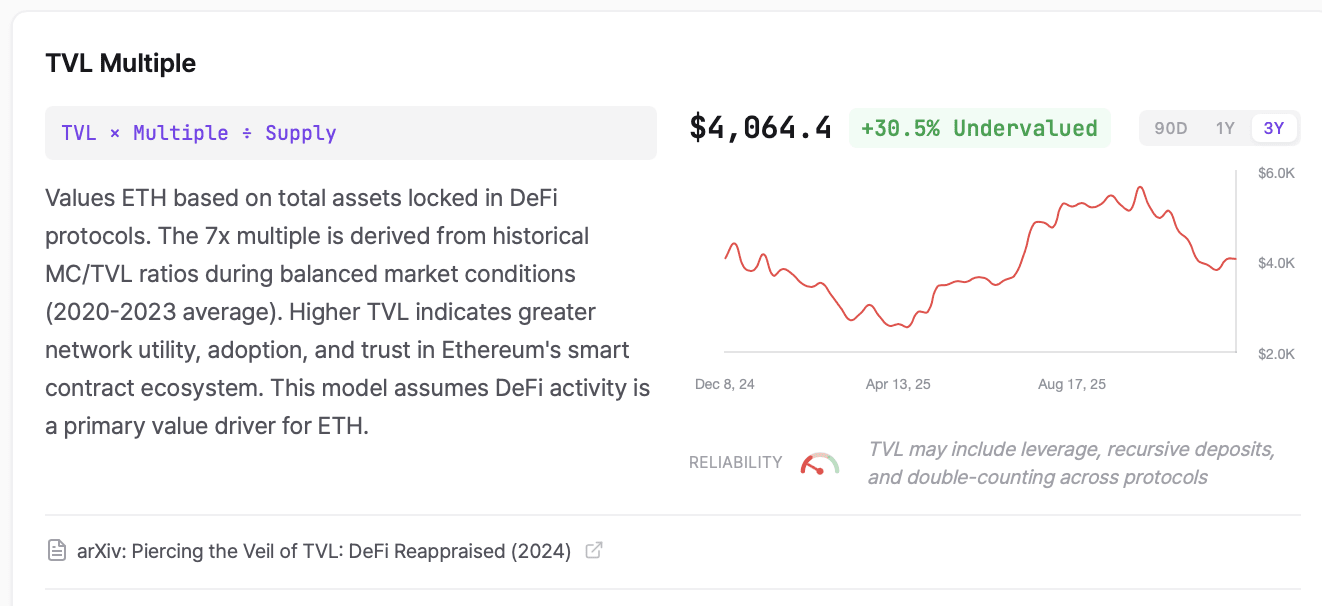

1. TVL Multiple

The idea: if a large amount of assets are locked in DeFi on Ethereum, the network must be expensive.

The formula typically looks like: TVL × multiplier ÷ ETH supply. ETHVal is assumed to have a multiplier of ~7×, derived from the average MC/TVL values for 2020–2023.

Strengths:

Directly ties the price of ETH to the utility of the DeFi ecosystem.

Simple, intuitive: more real activity → more TVL → higher rating.

Weaknesses:

TVL is a metric with problems: double counting, recursive deposits, “drawn” protocols. Academic works directly indicate the non-standardization and limited verifiability of TVL.

The 7x multiplier is a product of past cycles. If the market sentiment changes, the “norm” could become 3x or 4x — and the model would cool down dramatically.

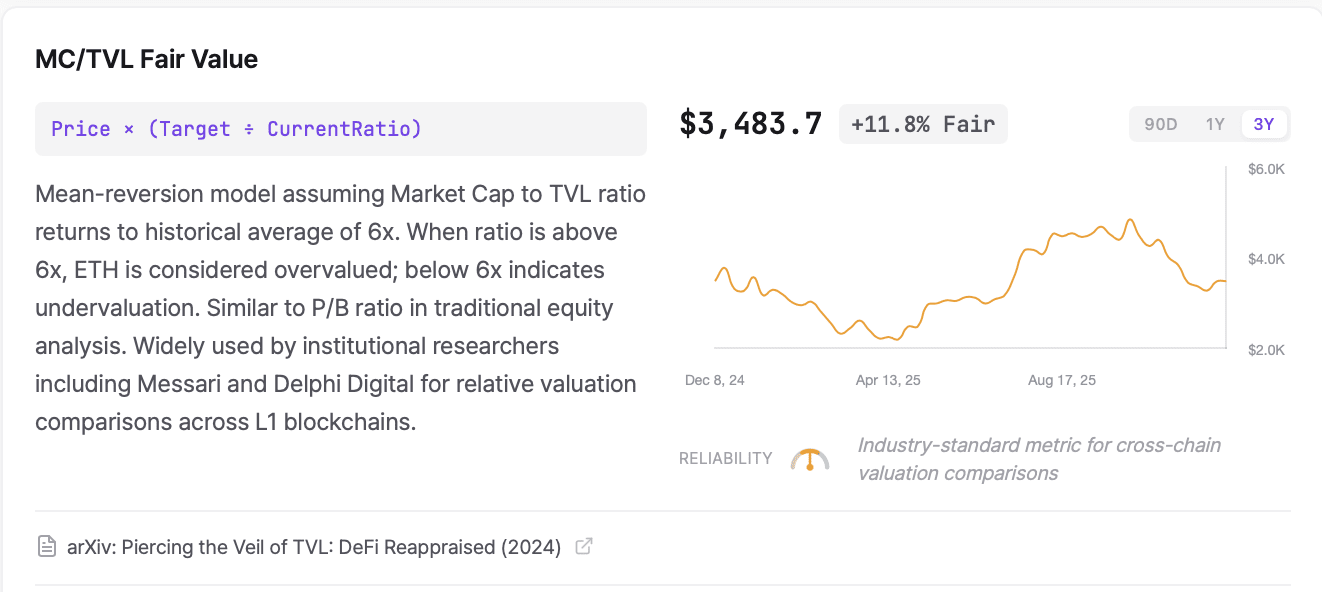

2. MC/TVL Fair Value

Idea: return to the historical average ratio of Market Cap / TVL ≈ 6×. If MC/TVL is lower now, ETH is undervalued, if higher, it is overvalued.

Strengths:

This is something like a P/B for L1 blockchains, actively used by Messari, Delphi Digital, and other institutional researchers as a standard for cross-chain comparisons.

Works well for relative valuation: where Ethereum stands relative to other L1s in terms of capital productivity.

Weaknesses:

Again, it all depends on the quality of the TVL. If the TVL is overestimated, the model will overestimate the “fair price.”

The historical 6× is not a law of nature. A new macrocycle may “recalibrate” the normal range.

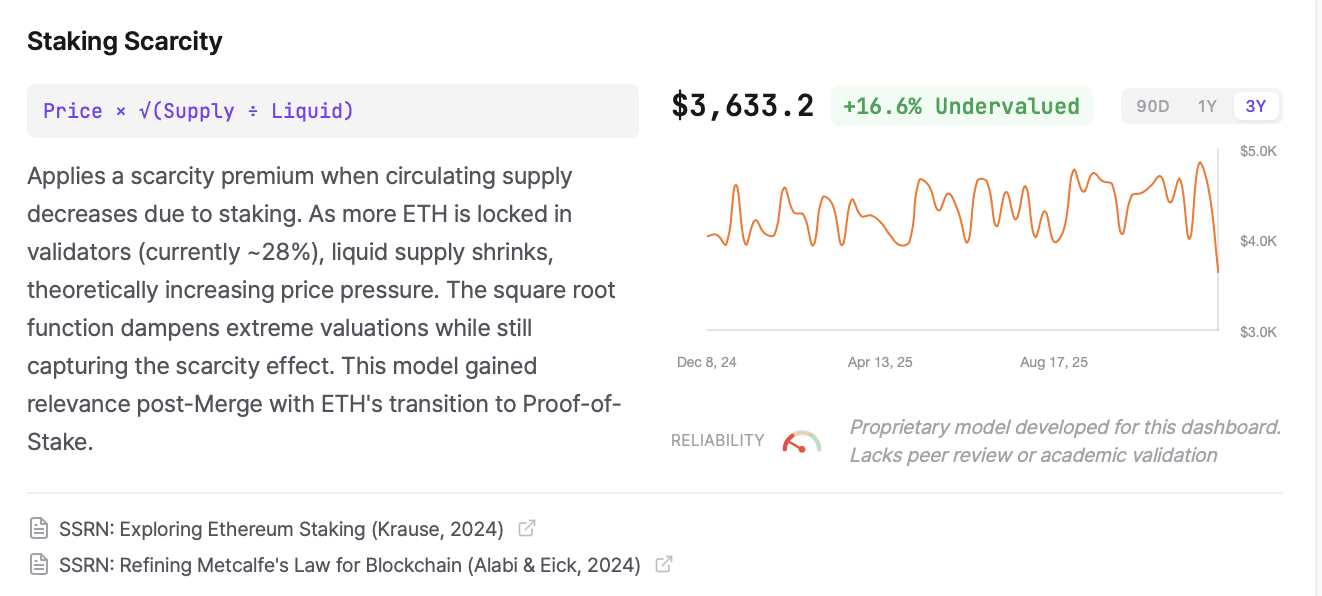

3. Staking Scarcity

The idea is that the more ETH is staked, the less liquid supply there is and the higher the price. The model uses the function Price × √(Supply ÷ Liquid), where the square root smooths out overly extreme estimates. ETHVal currently assumes that ~28% of the supply is staked.

Strengths:

Reflects the obvious: lockup = shortage = potential upside if demand doesn't fall.

Especially relevant after Ethereum's transition to Proof-of-Stake.

Weaknesses:

The model is proprietary, without academic validation: the formula is an engineering assumption of the authors of ETHVal.

Ignores the risk that staked ETH can quickly return to circulation in case of stress (staking derivatives, liquid “stETH-like” tokens).

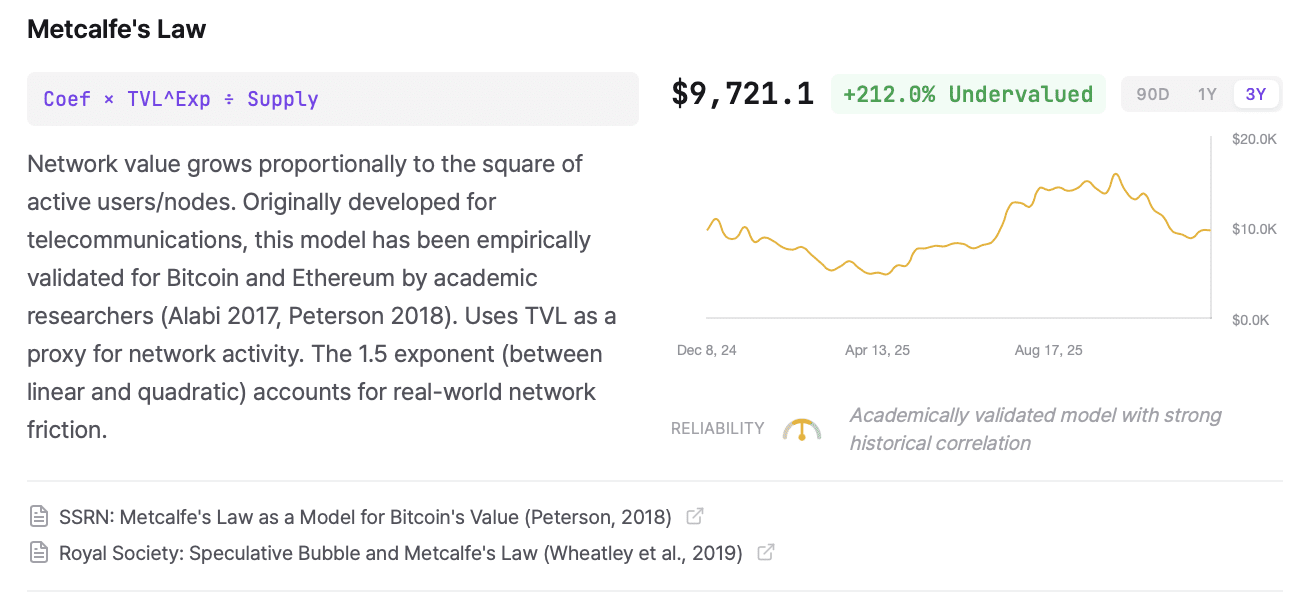

4. Metcalfe’s Law

The idea: the value of the network grows approximately as n^α, where n is the number of active users/nodes/economic ties. ETHVal uses TVL as a proxy for activity and an exponent of ~1.5 (between linear and quadratic) to approximate the real world.

Strengths:

There are academic papers that support the suitability of Metcalfe's model for Bitcoin and Ethereum.

It well reflects the network effect: each new user adds not one, but many potential interactions.

Weaknesses:

Choosing a proxy (TVL instead of the actual number of active addresses/transactions/dApp users) is a simplification that can distort the picture.

The coefficient and exponent are fitted to historical data, not derived from first principles—in new market regimes, the correlation may break down.

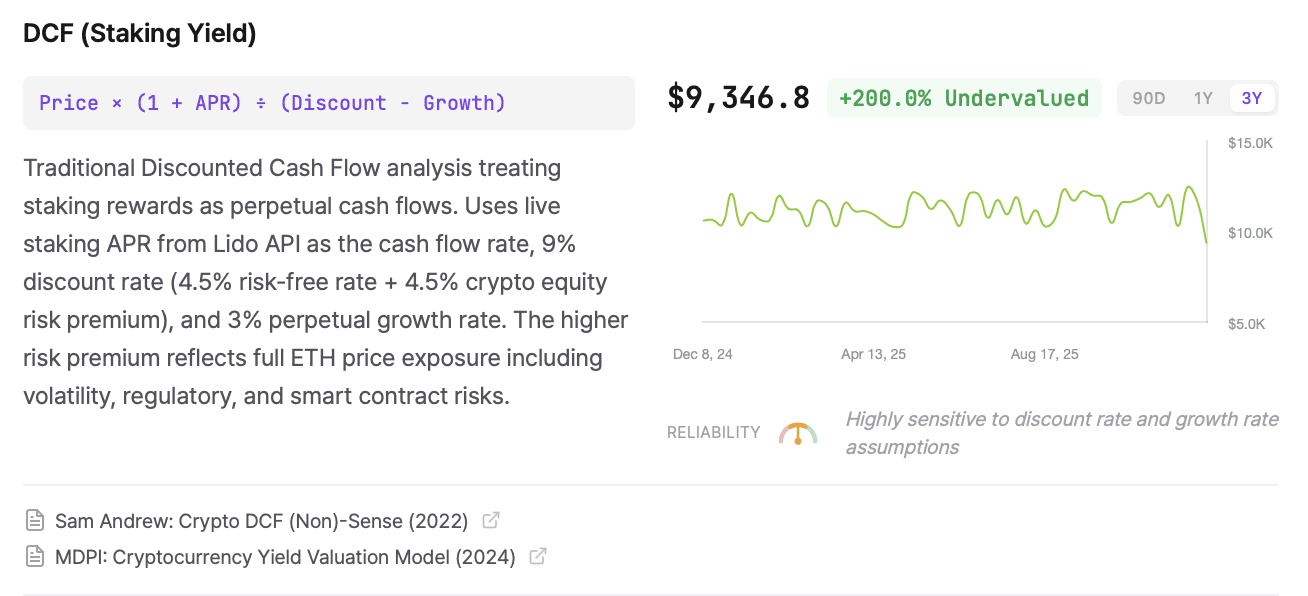

5. DCF (Staking Yield)

Idea: Classic Discounted Cash Flow, but instead of dividends, ETH staking yield treated as a perpetual cash flow. Current APR (according to Lido), discount rate ~9% (4.5% risk-free + 4.5% crypto risk premium), perpetual growth ~3%.

Strengths:

This is a bridge between TradFi and crypto: a model that institutional players understand from corporate finance.

Puts ETH on a par with cash-flow generating assets, not just "digital gold."

Weaknesses:

Extremely sensitive to parameters: change the discount rate by +1–2%, and the “fair value” collapses.

He believes that the current staking yield and risk structure are more or less stable — which is far from a fact for the crypto market.

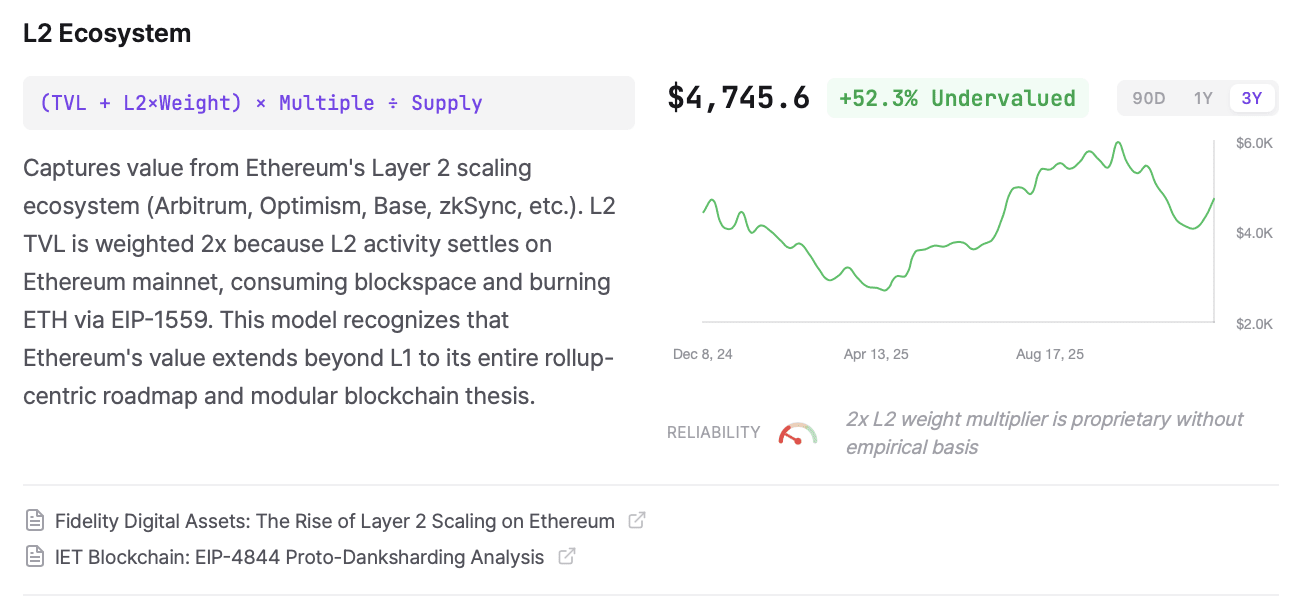

6. L2 Ecosystem

Idea: Ethereum = not just L1, but all the rollups and L2s that live on it. The model adds the TVL of all L2s (Arbitrum, Optimism, Base, zkSync, etc.), often with double weighting, as their activity burns ETH via EIP-1559 and consumes mainnet blockspace.

Strengths:

Correctly reflects that the "Ethereum economy" is broader than the L1 chain.

Emphasizes the value of a “rollup-centric” roadmap: the more L2 → the more fee generation and ETH burning.

Weaknesses:

L2-TVL also suffers from all the problems of TVL: double deposits, variable asset valuations, concentration risk.

The model hardly takes into account competition from alternative L2 and L1, which can drag down activity.

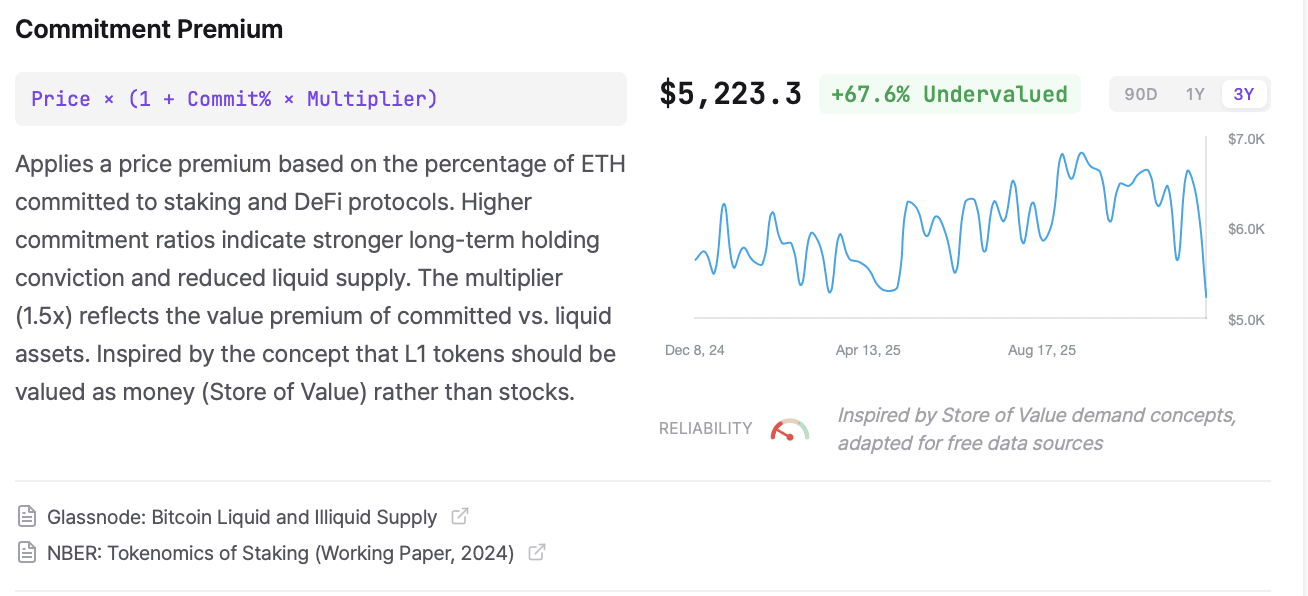

7. Commitment Premium

The idea: the larger the proportion of ETH “locked in trust” (staking + DeFi), the greater the premium the asset should receive as “long-term money.” ETH is valued here more as a money / store of value, rather than as a stock. ETHVal uses a multiplier of something like ~1.5× to the base valuation.

Strengths:

It captures the behavioral aspect well: the more holders do not sell, but stake/put in DeFi, the less free float.

Emphasizes the role of ETH as a collateral for the entire ecosystem.

Weaknesses:

The 1.5× multiplier is an assumption, not a law derived from the data.

Does not distinguish between “holding by conviction” and “holding by infrastructure constraints” (e.g., lockups, technical barriers).

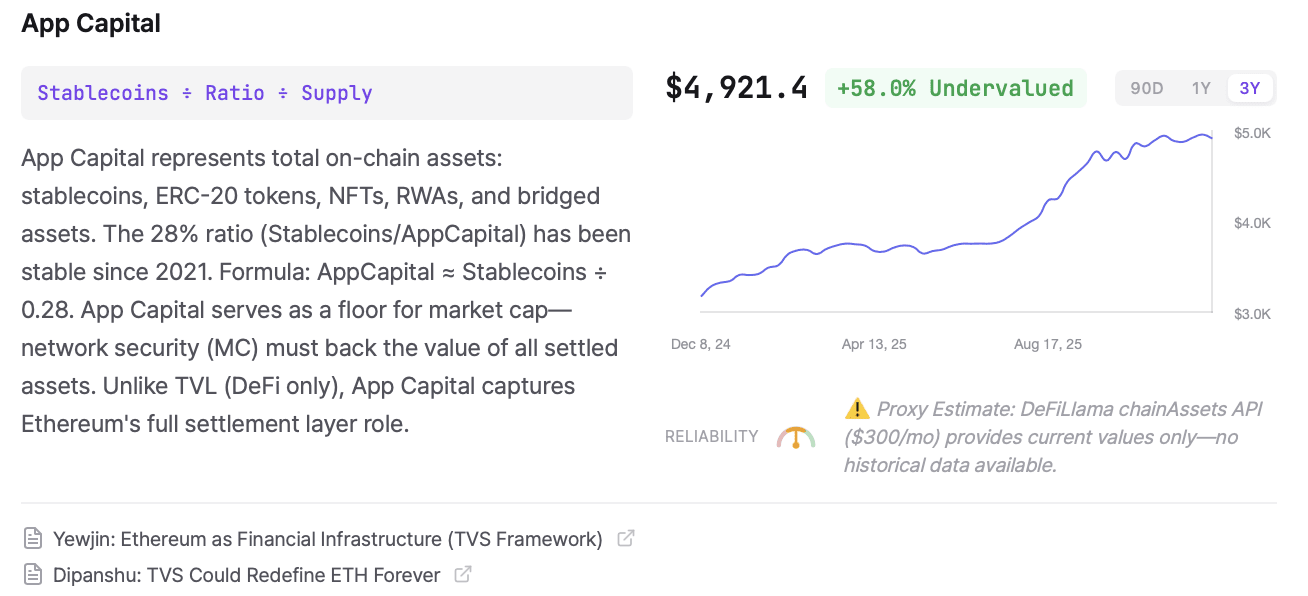

8. App Capital

Idea: Ethereum is a settlement layer for the entire on-chain asset class: stablecoins, ERC-20, NFTs, RWAs, bridged assets. ETHVal assumes that stablecoins account for ~28% of total App Capital and uses this to estimate the minimum required market cap for the network.

Strengths:

It looks broader than TVL DeFi: it includes NFTs, RWAs, and everything that lives in the EVM ecosystem.

The logic is simple: if Ethereum has N trillion on-chain assets, the network security (MC ETH) cannot be “too small.”

Weaknesses:

Assumptions about the stability of the 28% share may not withstand new market structures.

Not all assets on the network are equally dependent on Ethereum security (some may be duplicated on other chains).

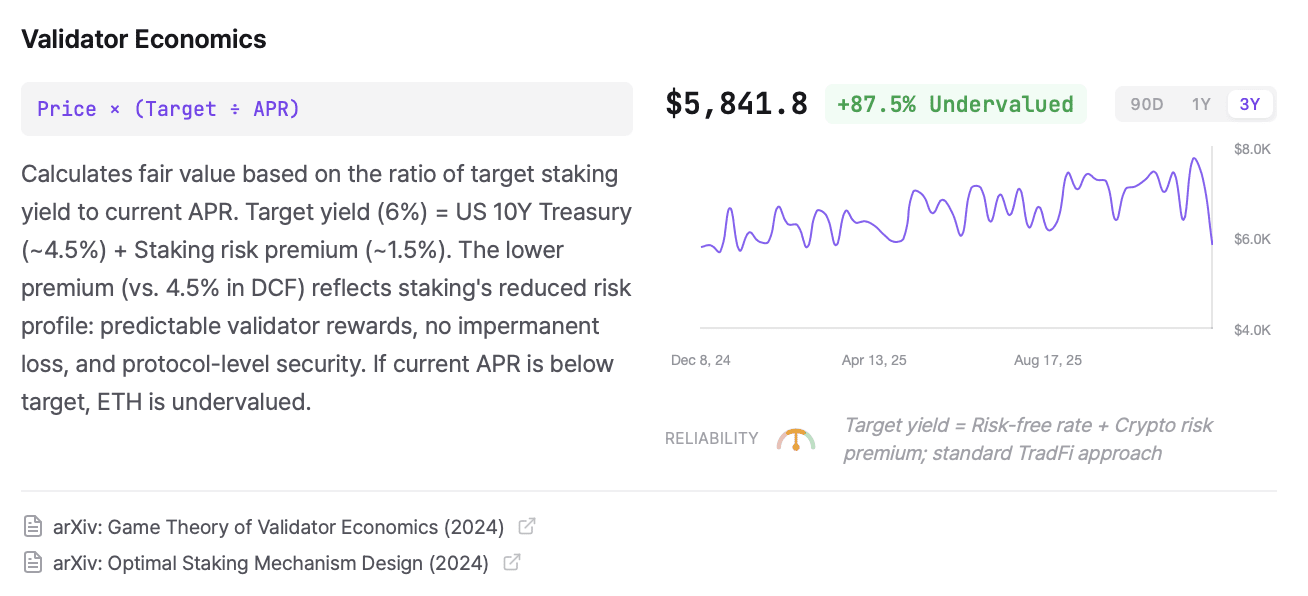

9. Validator Economics

The idea: ETH is valued by the “validator’s desired return.” If the noble staker’s target is, say, ~6% per annum (≈ USTreasuries + staking risk premium), and the actual APR is lower, ETH is considered undervalued (the price must rise for the return to fall to the target), and vice versa.

Strengths:

Looking at ETH through the eyes of an investor, comparing staking to bonds/income assets.

Fits well into the “Ethereum as a global income asset” narrative.

Weaknesses:

It is based on the assumption that a target return of 6% is adequate for all participants, which is not the case in the real world.

Ignores non-price factors: technical risks, regulatory restrictions for institutions, liquidity of staking derivatives.

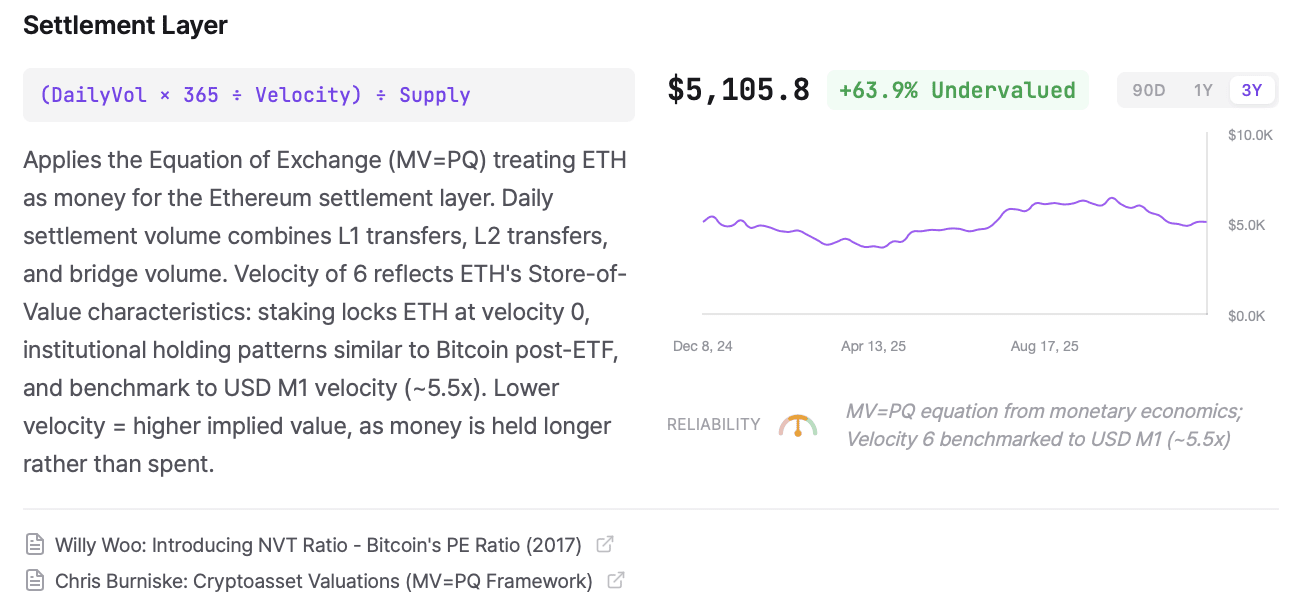

10. Settlement Layer (MV = PQ)

Idea: ETH is the money of the settlement layer. The model uses the equation of exchange MV = PQ, where:

M — “money supply” ETH

V — circulation velocity (for ETHVal, the velocity is taken to be ≈6, close to USD M1)

PQ is the actual volume of calculations (L1 + L2 + bridges).

Strengths:

Fits Ethereum into the macroeconomic framework as an infrastructure for global payments, not just an “asset.”

Takes into account the role of staking and holding in reducing the velocity of circulation (lower V → higher implicit price).

Weaknesses:

Estimating V is a difficult task: different types of transactions have different economic weights.

Strong dependence on the correctness of the calculation of the settlement volume (whether to include internal DeFi swaps, NFT trading, etc.).

Models that say: “ETH is overvalued”

ETHVal honestly shows that not all frameworks scream "buy":

11. Revenue Yield

The idea: we take the annual network revenue (fees + MEV) and divide it by the price, we get the “earnings yield”. If a certain yield is required for an adequate risk premium, and the actual yield is lower, the asset is overvalued. In the current ETHVal snapshots, this model gives a “fair value” significantly lower than the market — in the region of $900–1500, depending on the parameters.

The bottom line: Ethereum is viewed here as a “share of the fee-generating network,” and at a given discount rate, the current return looks small.

12. P/S (Price-to-Sales) Ratio

Idea: classic P/S = Market Cap / Revenue. A target coefficient of ~25× is taken for ETHVal. At the current level of network revenues, the model gives an even lower “fair” price than Revenue Yield — conditionally $700–1000 per ETH, which is 70+% below the spot.

The bottom line: If you view Ethereum as a fixed-revenue company, the market is paying “too much” for it per dollar of revenue.

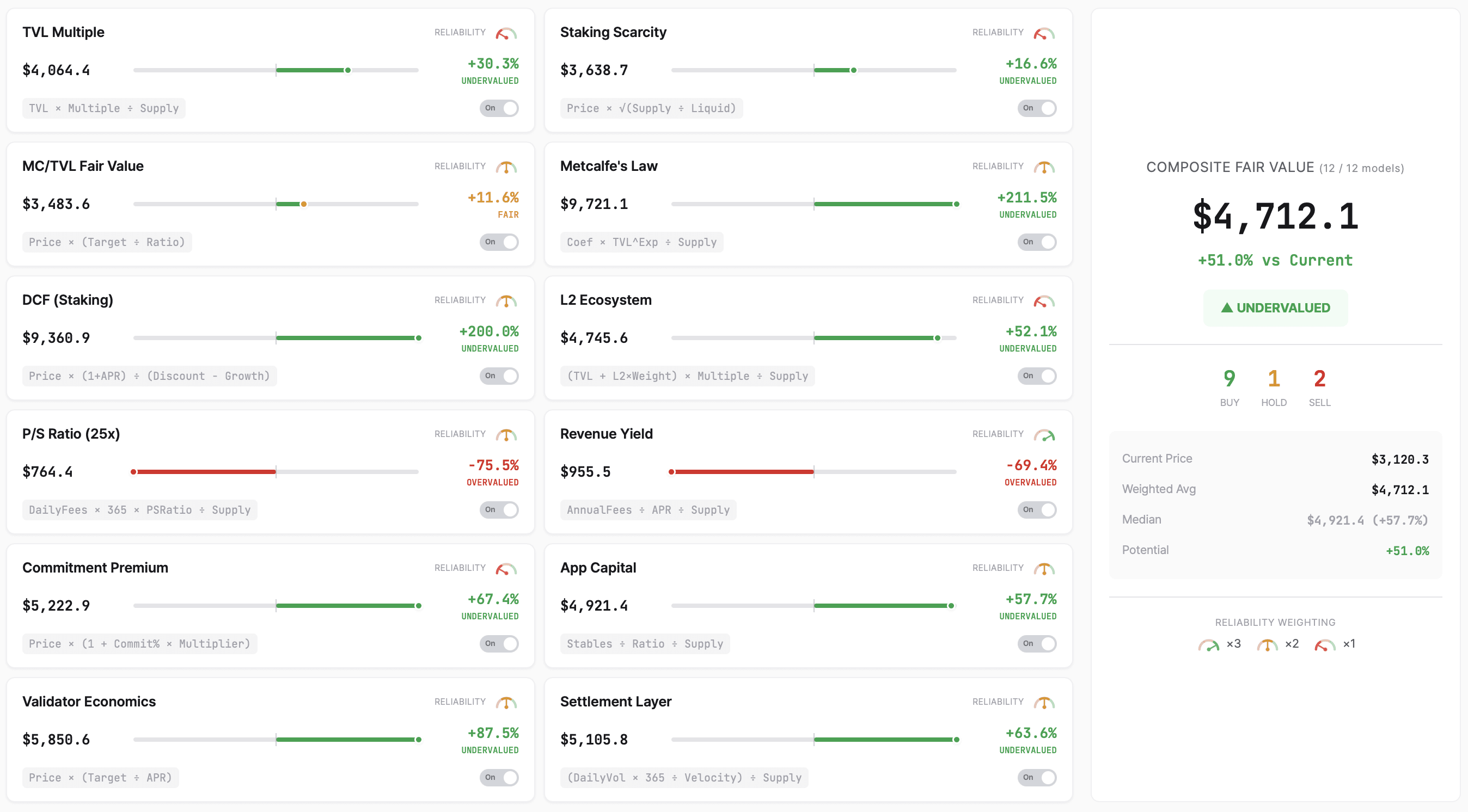

How to put it all into one picture

ETHVal doesn't just show 12 distinct numbers. The panel builds:

Composite Fair Value is a weighted average where academically and industrially more grounded models (Metcalfe, MC/TVL, App Capital) have greater weight than experimental frameworks.

Median across models — to reduce the impact of extreme estimates (such as DCF/Metcalfe by >+200%).

The “UNDERVALUED / FAIR / OVERVALUED” indicator for ETH is currently in the “UNDERVALUED” zone, according to several independent media outlets, with a potential upside of ~30–60% to the current price.

It is important to understand that this is not an “objective truth,” but an aggregate view of a set of models with different assumptions. Changes in rates, TVL, on-chain activity, or regulatory background can easily shift this picture.

Conclusion Moon Man 567

ETHVal is not a magic button “tell me the fair price of ETH”, but a tool that forces you to think fundamentally:

If you believe models based on network effects, DeFi activity, and Ethereum's role as a settlement layer, ETH appears undervalued.

If you look coldly through Revenue Yield and P/S — Ethereum is already “not cheap” in relation to its current revenue.

In my opinion, a healthy approach is this:

Baseline scenario: Ethereum is a Web3 core infrastructure with a positive imbalance in favor of undervaluation if:

The L2 ecosystem continues to grow;

staking remains attractive;

DeFi/on-chain activity is not degrading.

Strategic risk: as soon as:

TVL starts to “empty”,

network revenues are stagnating,

L2 and alternative L1 delay activity —

Models that give $4–9k per ETH may be too optimistic.

What this means for the trader and investor:

ETHVal models should not be used as a “buy today” signal, but as a framework for thinking: what exactly the market is evaluating/ignoring in Ethereum.

If you are building a long position in ETH, it makes sense to focus on the development of the foundation (L2, fees, App Capital, staking share), and not just on price curves.

👉 If you are interested in seeing further analysis of such fundamental instruments and understanding where Ethereum, Bitcoin, and alts fit into this picture, subscribe to Moon Man 567. There will be even more macro transparency and analytics that go beyond the usual “ETH to the moon”.