From the financial truth of the AI frenzy to the resilient turnaround of the real economy, the market's choices are being recalibrated.

In the past 24 hours, the global market has been stirred by a seemingly traditional tech giant—Oracle.

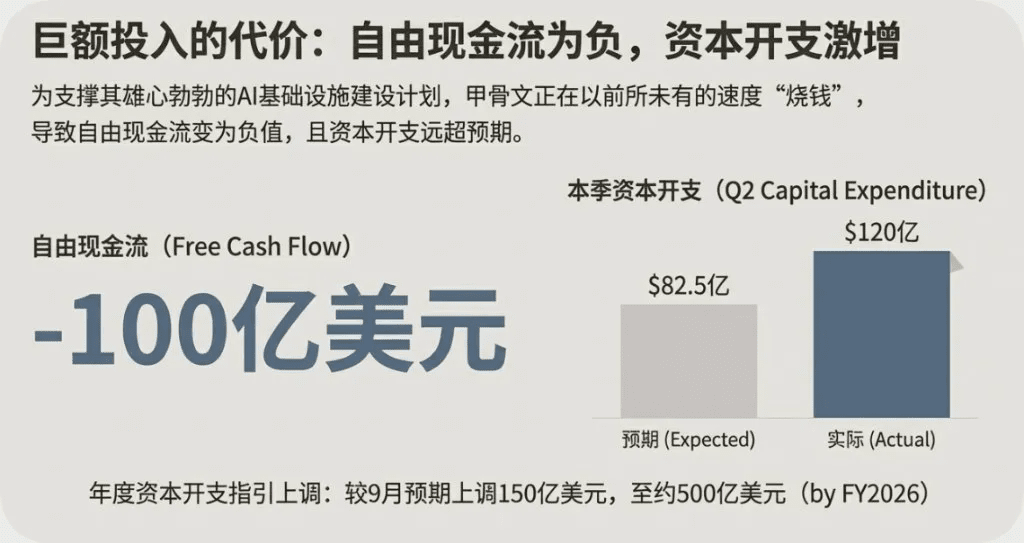

The company's latest financial report shows that to support its AI business, its annual capital expenditure expectation has been significantly raised by $15 billion to $50 billion, with quarterly free cash flow rarely turning to -$10 billion. As soon as the news broke, the stock price plummeted.

This is not an isolated case. Almost simultaneously, Broadcom's stock price fell due to AI revenue growth but pressured gross margins; while the Federal Reserve announced interest rate cuts, the market responded with long-term government bond yields reaching a 16-year high, revealing deep concerns about 'fiscal dominance' and the credibility of the dollar.

A series of events point to the same core: After experiencing the dual frenzy of technological explosion and monetary easing, global capital is undergoing a serious 'certainty re-evaluation' of various assets.

When Oracle, hailed as the 'pillar of AI infrastructure,' suddenly shows weakness, and the awkwardness of OpenAI's trillion-dollar computing order behind its 12 billion revenue is brought to light, the market finally begins to question: is the high-leverage game that supports the entire AI frenzy really about to face a liquidation moment? In this storm, what signals are conveyed by Bitcoin's counter-trend rebound and silver's doubling celebration? The answer lies in the leverage maze of AI and the logic of asset interconnection.

I. The 'circular financing game' in the AI circle: 12 billion revenue supporting a trillion-dollar order?

Oracle's plunge can be traced back to a bizarre 'triangular loop' within the AI ecosystem. Since 2025, OpenAI has signed a trillion-dollar computing power procurement order, with suppliers including Nvidia, Oracle, CoreWeave, etc. - but the problem is, OpenAI's total revenue for the year is only 12 billion USD.

Where does the money come from? The answer lies in the 'closed-loop game' of Nvidia, OpenAI, and Oracle:

Nvidia's financial support: as an investor in OpenAI, continuously providing funding support, binding its computing power needs;

OpenAI's purchase order: paying Oracle for data center operation costs with financing and advance payments;

Oracle's chip purchase: using the money earned to buy Nvidia's GPU chips to expand capacity.

This is essentially a leveraged play of 'cash flow from future orders.' Oracle's CEO Ellison once boldly claimed, 'OpenAI is our biggest GPU customer,' but now this 'largest customer' is in a dilemma: the larger the scale, the more it loses, subscription revenue can't even cover reasoning costs, let alone fulfill the trillion-dollar procurement promise.

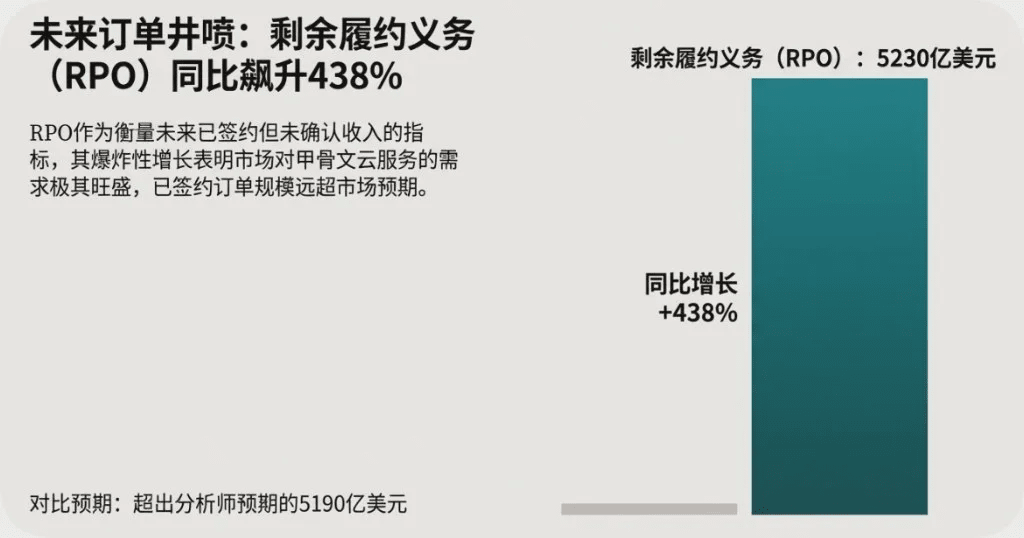

In September, when Oracle announced a backlog of 455 billion USD contracts, the market believed its 'growth story'; now everyone has awoken: orders are one thing, whether they can be converted into revenue is another.

II. Google's rewritten rules: In the AI war, computing power is no longer king

What also crushed Oracle was the logical mutation in the AI industry - the emergence of Google Gemini3, which directly overturned the iron law that 'whoever has computing power wins.'

Since the beginning of this year, Oracle and CoreWeave have been crazily building data centers and hoarding GPUs, betting on the 'scarcity of computing power.' However, Gemini3 has proven with its performance that, after surpassing GPT-5 in critical dimensions like objective reasoning and multimodal understanding, the real decisive factor has become the conversion efficiency of 'computing power → model → product → ecosystem.'

This is a fatal blow to Oracle: its core competitiveness lies in the 'GPU cluster + liquid cooling network' infrastructure capability, but it lacks the ability to implement models and products. When OpenAI has to face competition from Gemini3 and Claude 3.5, and has no money to pay for computing bills, Oracle's 'growth fundamental' collapses.

Worse, on December 13, news broke that 'some data center deliveries from OpenAI have been delayed until 2028,' and Oracle's stock fell another 7% - the market has already voted with its feet, determining that in this AI infrastructure gamble, it is bound to lose.

III. 100 billion debt hanging over: Oracle's tightrope cannot move

Oracle's crazy expansion is built with real money, most of which is borrowed.

The financial report data is heartbreaking: quarterly free cash flow (FCF) is -10 billion USD, unpaid debt exceeds 100 billion USD, making it the 'debt king' among investment-grade tech companies. More aggressively, it raised its capital expenditure for the fiscal year 2026 from 35 billion to 50 billion, euphemistically called 'investment in revenue-generating equipment,' but the market saw through it - this is borrowing to fill the hole in AI infrastructure.

The most intuitive signal is 'credit default swaps (CDS)': Oracle's five-year CDS costs have surged to the highest since October 2023, traders are betting wildly on its debt risk. After all, when customers can't pay, and industry logic changes, 100 billion dollars of debt turns from 'expansion ammunition' into 'detonation fuse.'

The storm spreads: Bitcoin gets hit, but silver celebrates against the trend?

Oracle's butterfly effect has already swept into the crypto and precious metals markets:

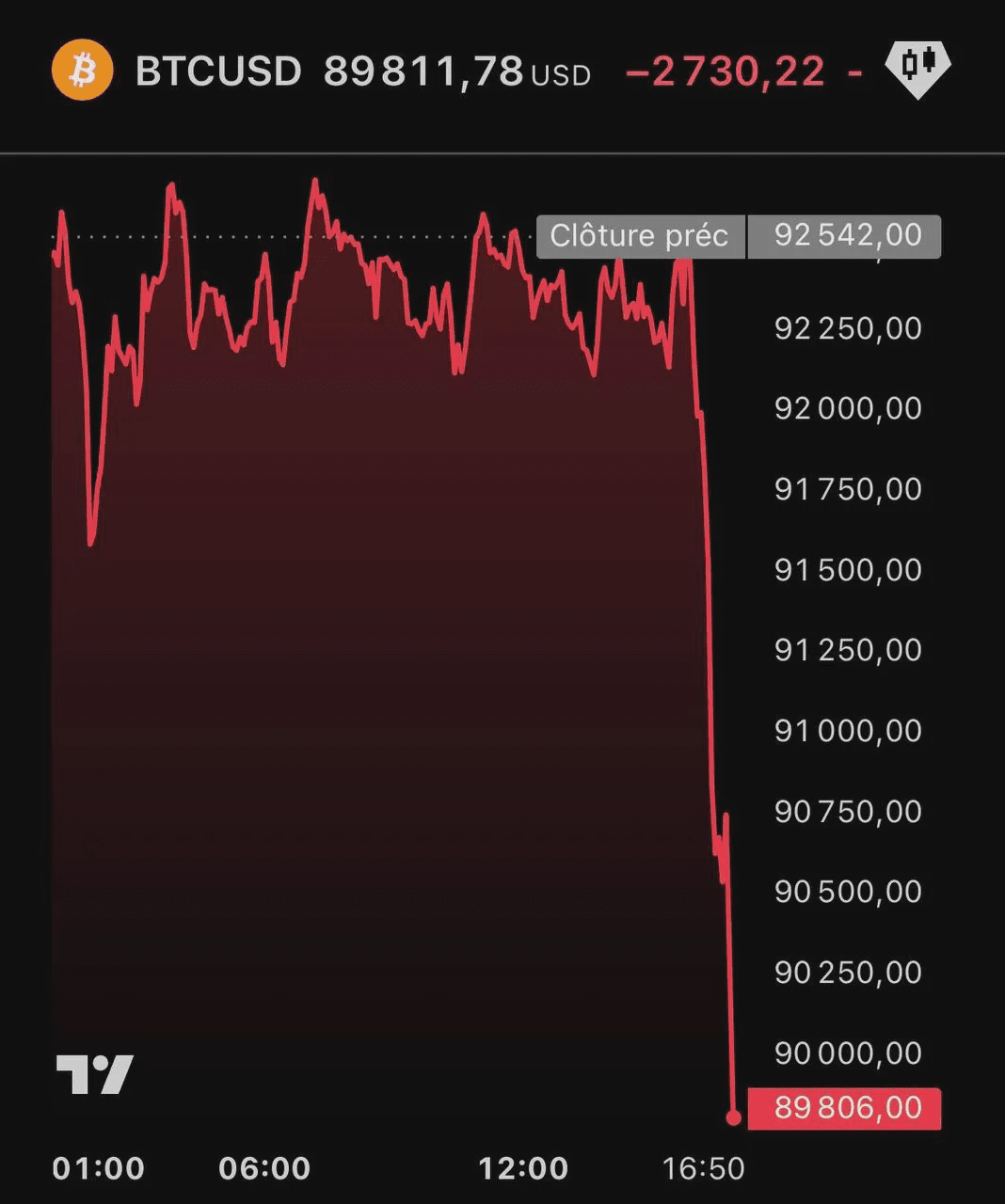

Bitcoin: after getting hit, a turning point hides

On December 13, Bitcoin fell from 92,000 USD to below 89,000 USD. On the surface, it seemed to be 'Nvidia-related sentiment transmission,' but the core issue is the market's panic selling of risky assets. However, a turning point is also emerging: the Federal Reserve dismissed the Atlanta president who opposed interest rate cuts, easing expectations have risen, and Bitcoin has rebounded to around 91,000 USD.

Fidelity analysts have provided long-term confidence: Bitcoin's fifth wave of rise may reach 151,360 USD, and the current correction looks more like 'fluctuations in a mature market' rather than a trend reversal.

Silver: doubling in a year, is the celebration not over?

Unlike Bitcoin's fluctuations, silver is迎来 'Davis double hit': On December 12, Shanghai silver futures first broke 15,000 yuan/kg, London silver rose above 64 USD/ounce, with an increase of over 120% this year, and Shenzhen silver jewelry prices have doubled compared to last year.

CITIC Futures pointed out that there are three core logics: the Federal Reserve's interest rate cuts suppress the dollar, silver spot is squeezed, and industrial demand for photovoltaics is surging. Looking ahead to 2026, with dollar credit contraction + economic recovery, silver's upward elasticity will be greater than that of gold.

In the face of the AI storm and asset differentiation, different investors can layout like this:

AI sector: Avoid the 'pure infrastructure' trap: steer clear of high-leverage computing infrastructure providers like Oracle, and shift towards companies with the capability to implement models (like Google and Anthropic) or core suppliers upstream of AI chips.

Coin: Bitcoin holds key support: short-term focus on the 90,000-91,000 USD support zone, if it holds, it can be a buying opportunity; for the long term, refer to Fidelity's logic, ignoring short-term emotional fluctuations.

Precious metals: silver can be bought on the dips: short-term support looks at 63 USD, and long-term benefits from easing and industrial demand, corrections are buying opportunities.

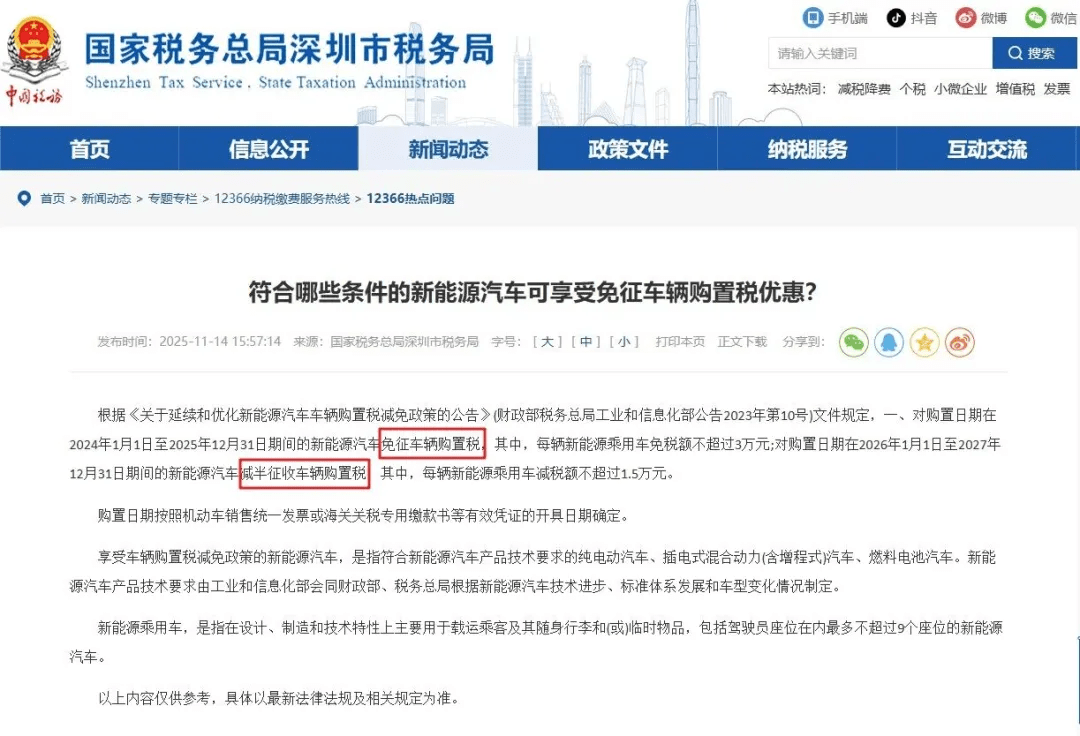

🚗 New energy vehicle bonus: Buy a new energy vehicle before December 31, 2025, to be exempt from purchase tax, and starting in 2026, it will be halved. For a 100,000 vehicle, an additional 4,425 yuan, for a 200,000 vehicle, an additional 8,850 yuan, essential vehicle owners should not miss the last window period (based on the invoice date).

Finally: using 'consensus' thinking to see through the bubble

The current chaotic signals in the market have ended the simple bull-bear narrative. We are in a complex period where multiple paradigms coexist and new and old risks intertwine.

Cognitive psychologist Steven Pinker said in (When Everyone Knows That Everyone Knows) that the essence of a bubble is 'self-reinforcing consensus': the AI circle first reached a consensus that 'computing power is king,' driving up Oracle's stock price; now the consensus has reversed, triggering a stampede.

For investors, the key to clarity is distinguishing between 'facts' and 'consensus': Oracle's 455 billion order is 'consensus,' 12 billion revenue is 'fact'; AI needs computing power is 'fact,' but computing power ≠ success is 'new consensus.'

History shows that the greatest wealth often arises from the process of the old paradigm fracturing and the formation of new consensus. This AI storm is not the end, but the beginning of industry reshuffling. Just as Bitcoin has transformed from a speculative tool into a safe-haven asset, the AI industry will also return from 'leveraged frenzy' to 'value essence' - those that survive will certainly be the companies that turn technology into real revenue.

In the wave of uncertainty, the real anchor may be the change itself. Understanding and embracing this structural reconstruction, rather than resisting it, is the premise for survival and progress in the new era.

Do you think the AI leverage will completely blow up? Let's discuss your judgment in the comments~

Note: The views in this article do not constitute investment advice; the market has risks, and entering the market requires caution.