For those who have been listening to my commentaries over the recent months, I have been intimating that the market structure has fundamentally been unfavorable for meaningful price gains because the continued supply from OG Bitcoin holders while natural demand from ETFs and DATs have simultaneously slowed down.

At the same time, I have been also harping on the importance of Bitcoin to find meaningfully higher implied volatility level through a sustained fashion, especially towards the upside. I hollered “give me volatility or give me death” while optimistically sharing what was the first unusual breakout sign in November where we finally observed some uptick in volatility that gave me hope.

Unfortunately, that implied volatility has been getting crushed again over the past two weeks. From having reached as high as 63% in late November, it is now back to 44%. Bummer.

But why do these two behavioral patterns matter so much?

How are the two points about the OG selling and volatility amplification related at all?

Why is BTC not going up?

This is why it’s all related. Here is the one definitive chart to explain a big reason, its story and the problem.

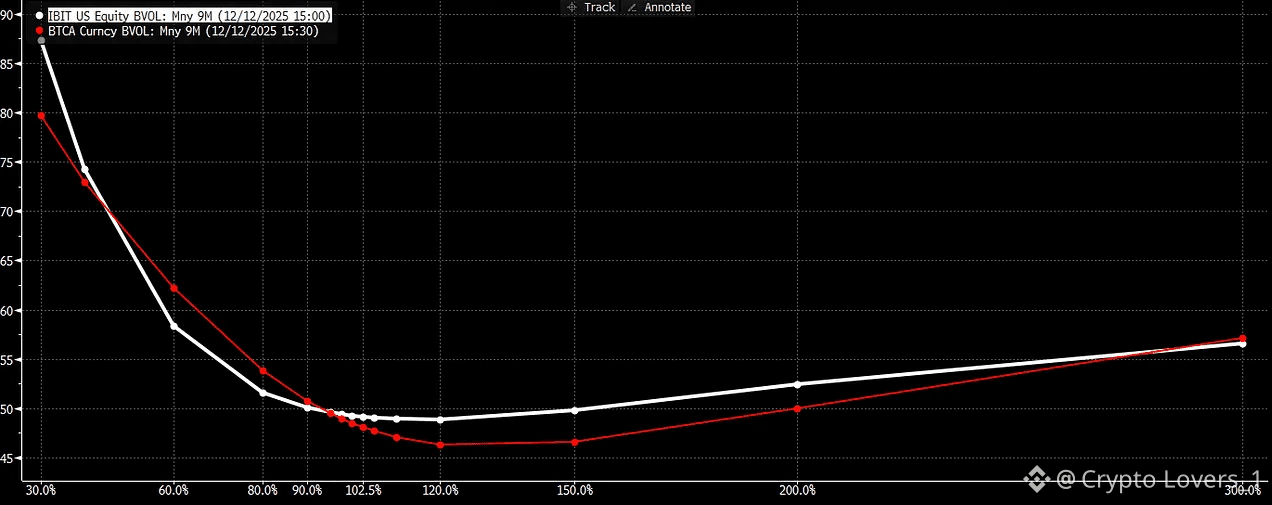

There is currently (and has been for a while now) a major divergence on upside skew between IBIT and BTC, in which the upside vol premium is much higher for IBIT than it is for native BTC when you go out beyond 3+ months and increasingly pronounced in longer duration. In theory with the same cost of capital, this spread should not be as sustainably pronounced as it is.

To explain how to read the graph, observe that in IBIT there is a positive call skew premium where the more you go out in the term structure, it slopes up in the 120-150% range, whereas BTC skew does not as its still downward sloping through 150%.

(Note that the redline above is referencing CME futures as the underlying, which is not exactly Deribit’s volatility skew because I couldn’t find a way to overlay that data conveniently but directionally is a correct substitute)

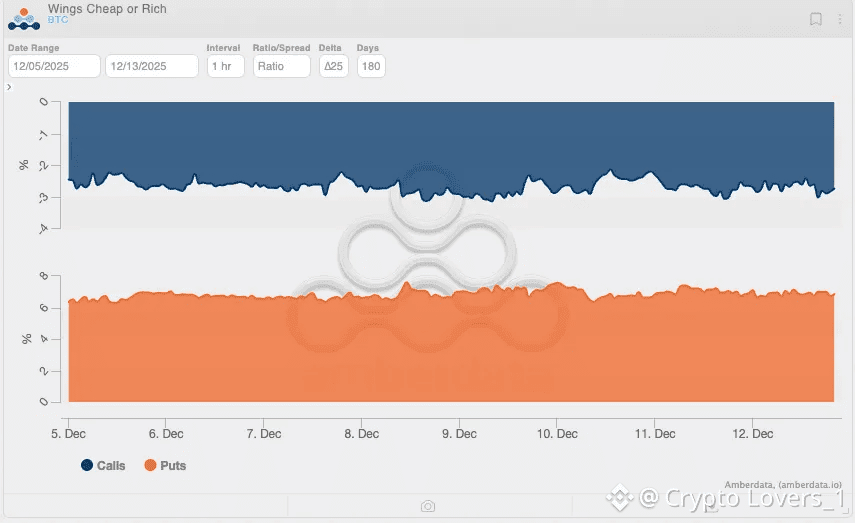

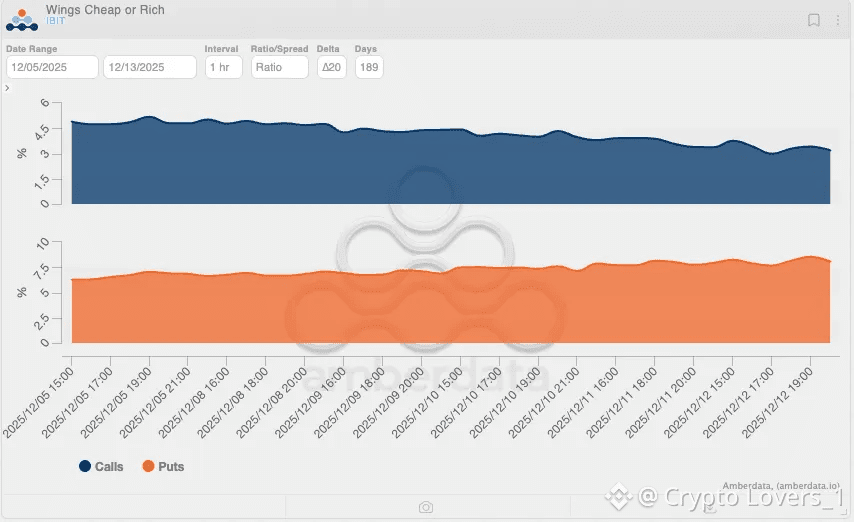

The “smile of the skew” becomes more obvious when we extend in duration beyond the 6 month mark when you look at the additional Amberdata charts comparing IBIT vs Deribit options. Take a look below:

Notice that IBIT’s call skew flipped positive (ie. upside calls are richer than ATM vol), whereas BTC skew remains negative (ie. upside calls are cheaper than ATM vol). In other words, IBIT has a volatility smile, but BTC does not.

Why might this happen? One way to explain this phenomenon is that BTC coin holders are selling vol in the open market on the upside much more aggressively creating a structural downward pressure, while the IBIT holders are buying upside vol creating a structural upward pressure. Simply, it means traditional market participants and crypto-native market participants are creating divergent flows that are resulting in divergent market structures.

“Ok Jeff, so it sounds like some are buying, some are selling so net net they cancel each other out so sounds like a nothingburger, right?”

Not quite. Here is the problem. All things equal, this creates a net delta for sale. Let me break it down why:

When you buy IBIT and sell calls against it, you are net buying delta in the market because you are buying the ETF (100% delta) and then selling calls (20-50% delta). So if you do a packaged trade, you are net adding partial delta. Most of the ETF flows that are seen as “net creates” are true inflows coming into Bitcoin for the first time, which has generally been the trend since launch (and is only 2 years old).

But when you already have the Bitcoin inventory that you’ve had for 10+ years that you sell calls against it, it is only the call selling that is adding fresh delta to the market—and that direction is negative (you are a net seller of delta when you sell calls). This is simply because the OG Bitcoiner’s existing position is already the existing collateral to fund the position so they do not need to buy delta one outright first.

This “BTC covered call” strategy, in part, explains the relentless continued selling from OG Bitcoiners that have now been widely documented and observed. In fact, this behavior has been continuing for years before the ETF launch, arguably since 2021. And while many are spot selling, the monetization of the existing collateral via options create another more serious adverse effect to the market as a whole.

This is because covered calls add long gamma across dealer desks. When BTC OGs are selling calls, it is the market makers on the other side that end up engaging in a dynamic hedging behavior that recreates mean reversion around the various strikes.

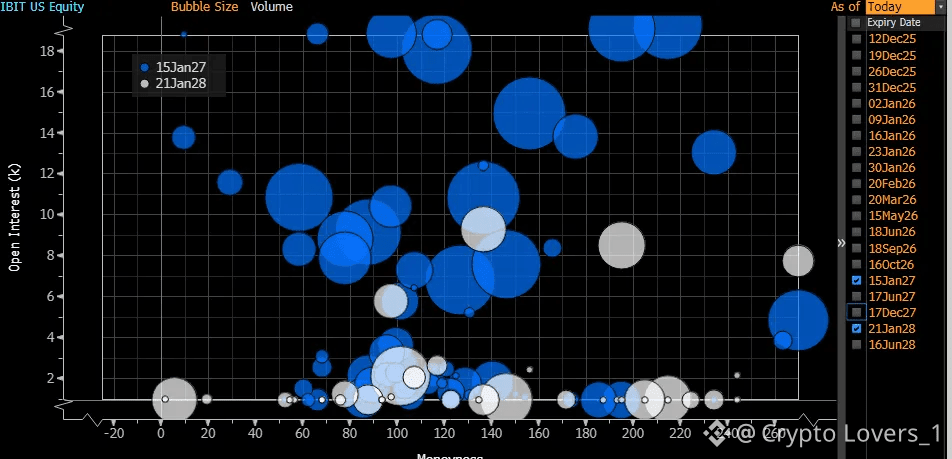

In fact, it is actually the natural IBIT call buyers that create negative gamma for the market makers that can potentially lead to a squeeze up. When you look at the Jan LEAPs in IBIT, the direction is clear: investors are mostly skewed to buying upside insurance.

This is why it is important that IBIT options continue to take a bigger share of the options market than Deribit. This is not because Deribit is bad by any means, but because of the reality that IBIT options are fresh collateral in addition to fresh speculation. It is because the only way to create an upside vol melt-up is when IBIT short gamma demand takes over Deribit’s long gamma supply.

Many crypto investors wrongly call out that Bitcoin ETFs are “paper Bitcoin” and options on Bitcoin ETFs are the culprit for muting price action. I make the case that it’s actually the reverse. Bitcoin ETFs have not only been net positive delta into the system it has been a net been vega contributor to the market as well; it’s actually the OG supply that is overwhelming on the margin on both delta and vega.

I posted this back in July as a historic milestone in which IBIT options are close to 50% of the options market.

IBIT today is now a whopping $41Bn in OI as of Dec 12. That is simply breathtakingly incredible. To put that in context, the OI on IBIT is more than 50% of its actual total AUM, and the notional itself doubled in less than half a year. In other words, options flow are becoming increasingly important price setters, and will definitively be the marginal flows that move markets in the near future.

However, Deribit’s OI has also grown to around $46Bn as I can read, which means that while the total notional market grew for both markets, IBIT has not been materially able to close the gap further. Given that CFTC has now announced pilot programs to let FCMs use native Bitcoin as collateral for derivatives, it is likely that the native supply coming online will continue to mute volatility, and we may even see the volatility arbitrage compress.

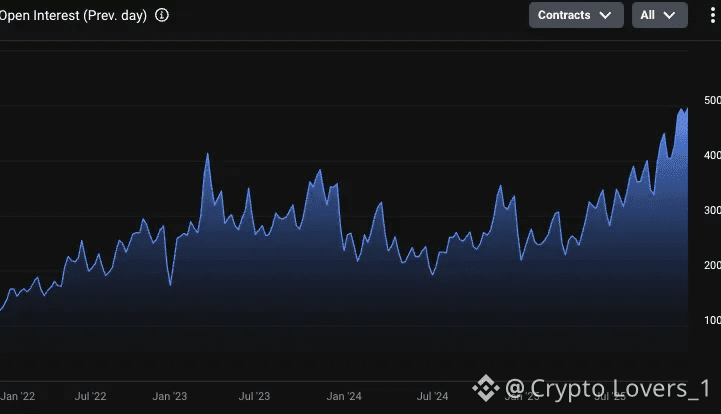

Further, the most compelling way to observe this trend is to see Deribit’s BTC Options OI in terms of BTC units (not dollar notional, which is affected by BTC price itself). You can see visibly below that BTC options on Deribit has nearly 5x’ed since 2022, and in particular - see the trend line from January 2025 to now— a straight upward linear slope. In addition, call OI is 2x put OI (312k vs 165k as of 12/12). The action is in the calls.

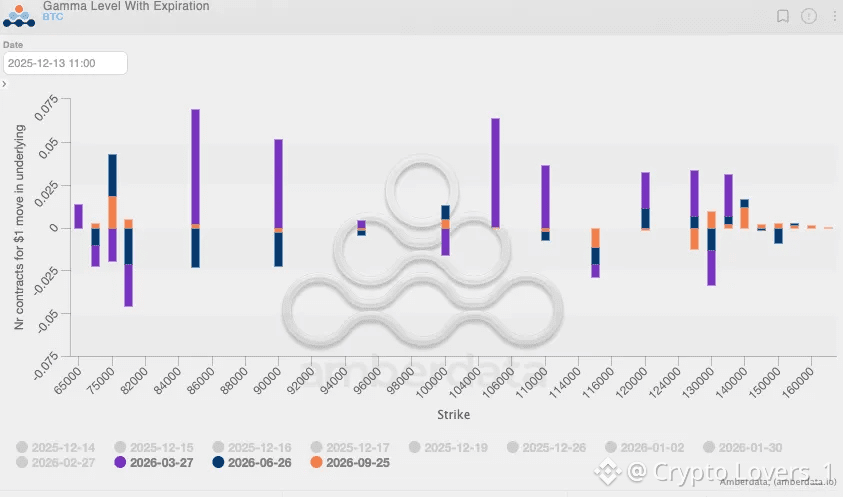

Now that we confirmed 1) Deribit OI is increasing, 2) it is call-driven, the most important question is— are these calls being sold? At the center of this analaysis is to confirm that this is what gives market makers long gamma profiles that are vol-muters. While this is not an easy exercise, it is theoretically possible by seeing whether the OIs that are created are done via ask/bids to know whether the aggressive takers were hitting bids or lifting offers. Based on that, the below gamma exposure paints a confirmatory picture: the three longest duration expirations available on Deribit all show that gamma is POSITIVE from 1004k and above for the most part, in size.

That is essentially all you need to know about the story of 2025.

2025 was a paradoxical year for many Bitcoin traders because the mainstream risk-on assets like Mag7, AI, and even Gold have all performed spectacularly on the debasement case while Bitcoin itself has been idiosyncratically lagging. I believe that one of the root causes for this divergent outcome is not only because the Bitcoin-natives are the net sellers of delta, but more critically because they are net sellers of vega too. And vega matters more than delta because while futures/perps liquidations are incredible tools to predict short-term market movements, it is actually the contour of liquidity that the options market creates with duration over a long period of time that can create really powerful moves.

One of the signs I am looking at to see when the next leg up would be therefore is to see a 1) decrease in vol supply from the Bitcoin options market, or 2) a significant increase in IBIT options market vol demand. Until that happens, a reluctant admittance that Bitcoin is likely to remain a trader’s market in its choppiness must be considered a strong possibility.