Written by: Fintax

1. Introduction

On November 3, 2025, coinciding with the grand opening of "Hong Kong Fintech Week," the Hong Kong Securities and Futures Commission (SFC) simultaneously released two landmark regulatory circulars: one concerning shared liquidity among crypto asset trading platforms and the other expanding the product and service offerings of crypto asset trading platforms. The circulars state that, subject to regulatory requirements and prior written approval, licensed crypto asset exchanges can share listings with compliant overseas platforms to consolidate liquidity and expand their product and service offerings, including providing short-term virtual assets to professional investors. The timing of this policy announcement during a major event gathering tens of thousands of fintech elites from around the world clearly demonstrates Hong Kong's unprecedented determination to leverage crypto assets as a key tool for consolidating its position as an international financial center. This article will explore the significance of these new circulars in the regulatory governance of the crypto economy, within the context of the path outlined in the SFC's ASPIRe roadmap, and discuss their potential impact on platforms, investors, and market structure in the future.

2. Interpretation of the content of the circulars

2.1 (Circular regarding the sharing of liquidity by cryptocurrency trading platforms)

(Circular regarding the sharing of liquidity by cryptocurrency trading platforms) focuses on enhancing market liquidity under compliance, primarily allowing licensed virtual asset trading platforms (VATPs) to share order books with their overseas affiliated platforms to merge into a larger, deeper global liquidity pool, thereby improving price discovery, enhancing trading efficiency, and reducing cross-regional price differences.

The circular emphasizes strict settlement risk management, including the adoption of DVP (delivery-versus-payment) mechanisms, daily settlements, establishing compensation mechanisms, ensuring the safe custody of clients' cryptocurrency assets, and requiring platforms to establish legally binding shared order book rules, create cross-border collaborative market monitoring mechanisms, and fully disclose relevant risks to clients (especially retail investors) before providing this service, obtaining their clear choice to participate.

In addition, platforms must apply for approval from the Securities and Futures Commission in advance and incorporate corresponding terms and conditions into their licenses. The core of this circular is to allow licensed virtual asset trading platform operators to integrate order books with qualified overseas platform operators, creating a shared liquidity pool to achieve cross-platform matching and transaction execution. This mechanism requires platforms to adopt DVP settlement methods, implement intraday settlement, and monitor unsettled transaction limits, as well as establish a reserve fund and insurance or compensation arrangement in Hong Kong at least equal to the upper limit scale to cover settlement asset risks. Market monitoring must be uniformly implemented and can provide transaction and client data to the Securities and Futures Commission in real-time, with sufficient risk disclosure to retail investors and obtaining client confirmation of choice beforehand.

2.2 (Circular regarding the extension of cryptocurrency trading platform products and services)

(Circular regarding the extension of cryptocurrency trading platform products and services) focuses on expanding the range of products and services that platforms can offer, clarifying that "digital assets" include cryptocurrencies, stablecoins, and tokenized securities, while relaxing requirements for asset inclusion, such as eliminating the 12-month track record requirement for professional investors (PI) in cryptocurrencies and allowing stablecoins regulated by the authorities to be issued directly to retail investors.

The circular also proposes to amend the licensing conditions for platforms, allowing VATPs to participate in the distribution of digital asset-related investment products and tokenized securities and to provide custody services for digital assets (including tokenized securities) that are not traded on the platform, as long as they meet corresponding technical, security, monitoring, and anti-money laundering requirements. This circular focuses on "product diversification," removing the requirement for a 12-month track record for cryptocurrencies (including stablecoins) sold to professional investors, and allowing licensed stablecoin issuers to issue stablecoins directly to retail investors. At the same time, platforms can distribute tokenized securities and digital asset-related investment products, and may provide custody for digital assets not traded on the platform through affiliated entities, as long as they comply with current regulations.

3. Why issue the circular: Strategic continuation and market response

3.1 Strategic continuation of the ASPIRe roadmap

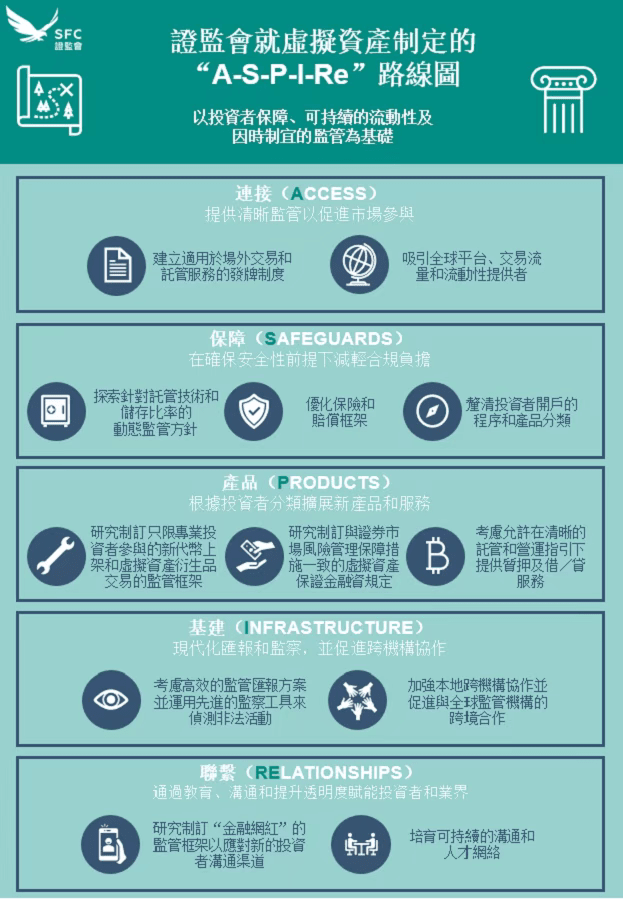

The issuance of the two circulars is not an isolated policy measure but can be viewed as the specific implementation of the "ASPIRe" roadmap released by the Hong Kong Securities and Futures Commission on February 19, 2025, at the institutional level. This roadmap is framed around five pillars: Access, Safeguards, Products, Infrastructure, and Relationships, clearly defining the long-term regulatory direction for the Hong Kong cryptocurrency market.

Specifically, the circular (regarding the sharing of liquidity by cryptocurrency trading platforms) primarily responds to the Access pillar in the ASPIRe roadmap — aimed at enhancing the liquidity connection between Hong Kong and overseas, improving market efficiency, and providing Hong Kong investors with deeper and broader global liquidity. Meanwhile, the circular (regarding the extension of cryptocurrency trading platform products and services) responds to the Products pillar in the ASPIRe roadmap, aiming to meet the diverse needs of different types of investors while balancing risk control and investor protection.

The CEO of the Securities and Futures Commission, Ms. Laura Liang, pointed out at a forum during Fintech Week that Hong Kong's closed-loop ecosystem, initially built around protecting investors and licensed cryptocurrency trading platforms, is gradually evolving to an important stage of "connecting the local market with global liquidity." This arrangement allows licensed platforms to share a single order book with affiliated overseas platforms, enabling local investors to utilize global liquidity while attracting this liquidity to the Hong Kong virtual asset market.

Illustration of the ASPIRe roadmap (Source: Hong Kong Securities and Futures Commission)

3.2 Responding to the liquidity dilemma in the market

The second reason for the SFC's issuance of the two circulars is to respond to the liquidity dilemma in the Hong Kong cryptocurrency market.

According to Fu Rao, Executive Director of the Hong Kong International New Economy Research Institute, the Hong Kong cryptocurrency market has long faced two interlinked practical problems: first, local platforms have thin trading volumes and sparse order books, many tokens have visible prices but cannot facilitate transactions; second, price discrepancies frequently occur between onshore and offshore markets, where the same asset often sees significant differences and slippage between Hong Kong and large offshore platforms. This not only affects investor experience but also undermines Hong Kong's credibility as a pricing hub. The design of the shared liquidity mechanism in the circular is a systematic response to this pain point — by selectively "bringing in" compliant liquidity from overseas, using a regulatory framework rather than purely market-driven behavior to address the two dilemmas of insufficient liquidity and price differences. For the Hong Kong market, price discovery is no longer limited to a single small local pool but connects to the global mainstream liquidity pool under a regulated mechanism, naturally narrowing price differences and bringing transactions closer to the true global level.

From a deeper perspective, the issuance of these dual circulars marks a shift in Hong Kong's cryptocurrency regulation from "gatekeeping" to "empowerment": new regulations are no longer just limitations, but actively pave the way for institutions to participate in cryptocurrency activities; not only blocking risks but also dedicated to guiding innovation, bringing gray areas into the regulatory framework. According to Fu Rao's perspective, Hong Kong's regulation has never been simply a free pass, but conditional opening under the premise of controllable risks. The design of the shared order book mechanism clearly reveals several red lines: only cooperate with licensed institutions, share data only within a regulated framework, synchronize assets only under the core requirement of delivery-versus-payment (DvP) settlement logic... This locks the legal, technical, and counterparty risks that cross-border cooperation may bring into a verifiable and accountable regulatory closed loop.

4. Impact on the Hong Kong cryptocurrency market

4.1 Rebuilding trust in digital asset hubs

From a regulatory perspective, the issuance of the dual circulars reflects Hong Kong's core regulatory principle of "same business, same risk, same rules." Dr. Yip Chi-hang, Executive Director of the Intermediaries Division of the Securities and Futures Commission, emphasizes that the new roadmap adheres to the core principles of investor protection, sustainable liquidity, and flexible regulation, precisely responding to the challenges of the emerging cryptocurrency market.

It is worth noting that the Securities and Futures Commission emphasizes strict risk control requirements in the dual circulars, in addition to promoting market development. The shared liquidity mechanism requires overseas affiliated platforms to establish a regulatory framework aligned with FATF recommendations and IOSCO cryptocurrency policy suggestions and to accept ongoing supervision from local regulatory authorities; the settlement mechanism requires full prepayment, delivery-versus-payment, intraday settlement, and other measures; in terms of investor protection, it requires the establishment of a customer compensation reserve fund and insurance arrangements.

At the same time, the Securities and Futures Commission continues to strengthen anti-money laundering supervision. An important circular issued on November 17, 2025, urges licensed corporations and cryptocurrency trading platforms to remain vigilant regarding suspicious fund transfers that show signs of layered trading activities to prevent money laundering. A "24/7 payment stop" mechanism has been established in collaboration with the police to enhance the detection and prevention capabilities against virtual asset crimes.

4.2 Shaping an investment landscape of opportunities and challenges

For platforms and practitioners, the primary benefit brought by the dual circulars is the significant expansion of business development space. The product extension circular allows platforms to quickly list emerging tokens and stablecoins, distribute tokenized securities and digital asset products, and explore custody services. The shared liquidity circular helps enhance trading depth and efficiency, improving user experience.

The increase in compliance costs is also a challenge that cannot be ignored. Participating in shared liquidity requires establishing complex cross-border settlement systems, unified market monitoring programs, reserve fund mechanisms, etc. This places higher demands on platforms' technical capabilities, financial strength, and compliance levels.

From an industry ecosystem perspective, the Hong Kong cryptocurrency industry in 2025 shows a clear trend of integration. Traditional financial institutions are actively embracing cryptocurrency business, with over 40 brokerage firms, 35 fund companies, and 10 large banks involved in cryptocurrency asset businesses. The tearing and integration of Crypto Native culture, internet finance culture, and traditional finance culture are shaping the unique ecosystem of Hong Kong's cryptocurrency industry.

5. Summary and outlook

The issuance of the dual circulars by the Securities and Futures Commission marks a new stage in the regulation of cryptocurrency assets in Hong Kong. This is not only a systematic response to the liquidity dilemma in the local market but also a strategic move for Hong Kong to seize a regulatory high ground in the global digital asset competitive landscape.

On one hand, the Securities and Futures Commission and the Monetary Authority are promoting the deep integration of traditional finance and blockchain technology. The "Fintech 2030" vision announced by the Monetary Authority will promote financial tokenization, leading by example for asset tokenization. The e-HKD pilot program is also continuously advancing, focusing on three major application scenarios: tokenized asset settlement, programmable payment, and offline payment; on the other hand, from a global perspective, the regulatory frameworks of markets such as Hong Kong, Singapore, and the UAE are increasingly converging. The EU's MiCA legislation, Dubai's VARA system, and Hong Kong's VASP licensing system are becoming increasingly similar in core principles, all emphasizing investor protection, anti-money laundering compliance, and market integrity. By aligning with international standards, Hong Kong is expected to play a more important bridging role in global digital asset regulatory coordination.

Looking to the future, as product services continue to expand, the stablecoin ecosystem accelerates, and traditional finance deeply integrates with Web3, Hong Kong is expected to truly become a global digital asset hub connecting the East and the West. As Dr. Yip Chi-hang of the Securities and Futures Commission stated: "Hong Kong has developed from a small fishing village into a leading financial center in the world, and we have the capability to achieve the same in the virtual asset market."