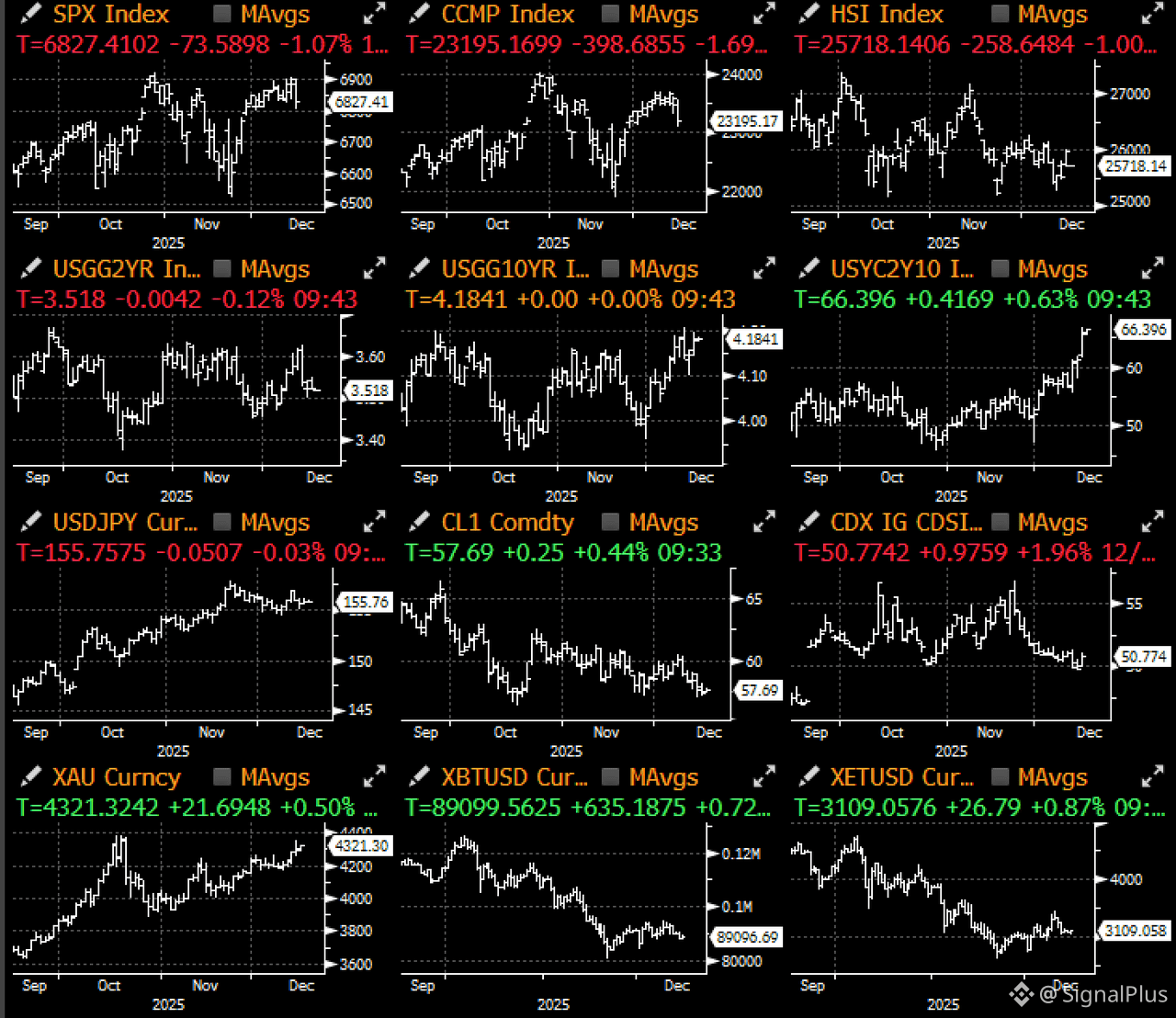

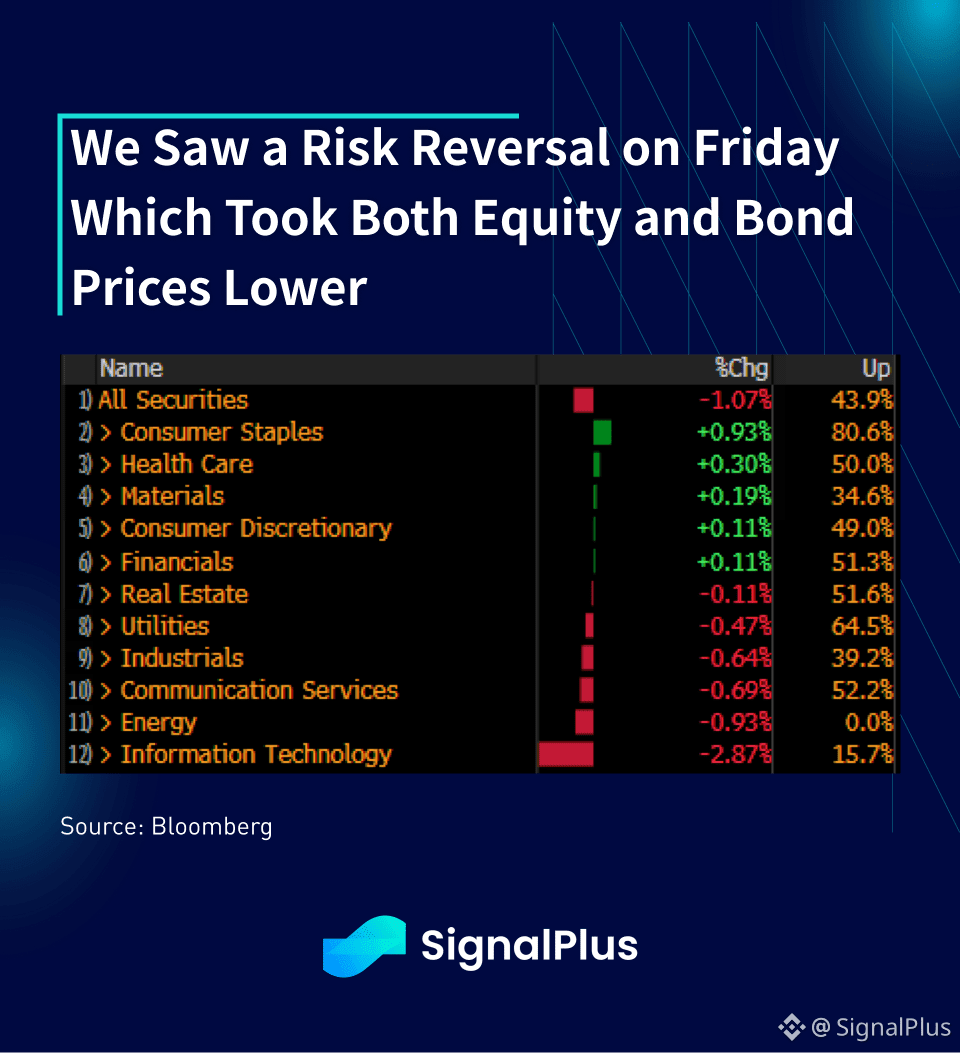

Risk sentiment made a 180 degree turn on Friday as macro assets sold off across the board, led by significant weakness in tech stocks with a bear steepening in the yield curve. Concerns over Oracle and Broadcom earnings dragged overall risk complex lower, while year-end profit-taking and sector rotation dragged Nasdaq lower by -2% intraday at one point.

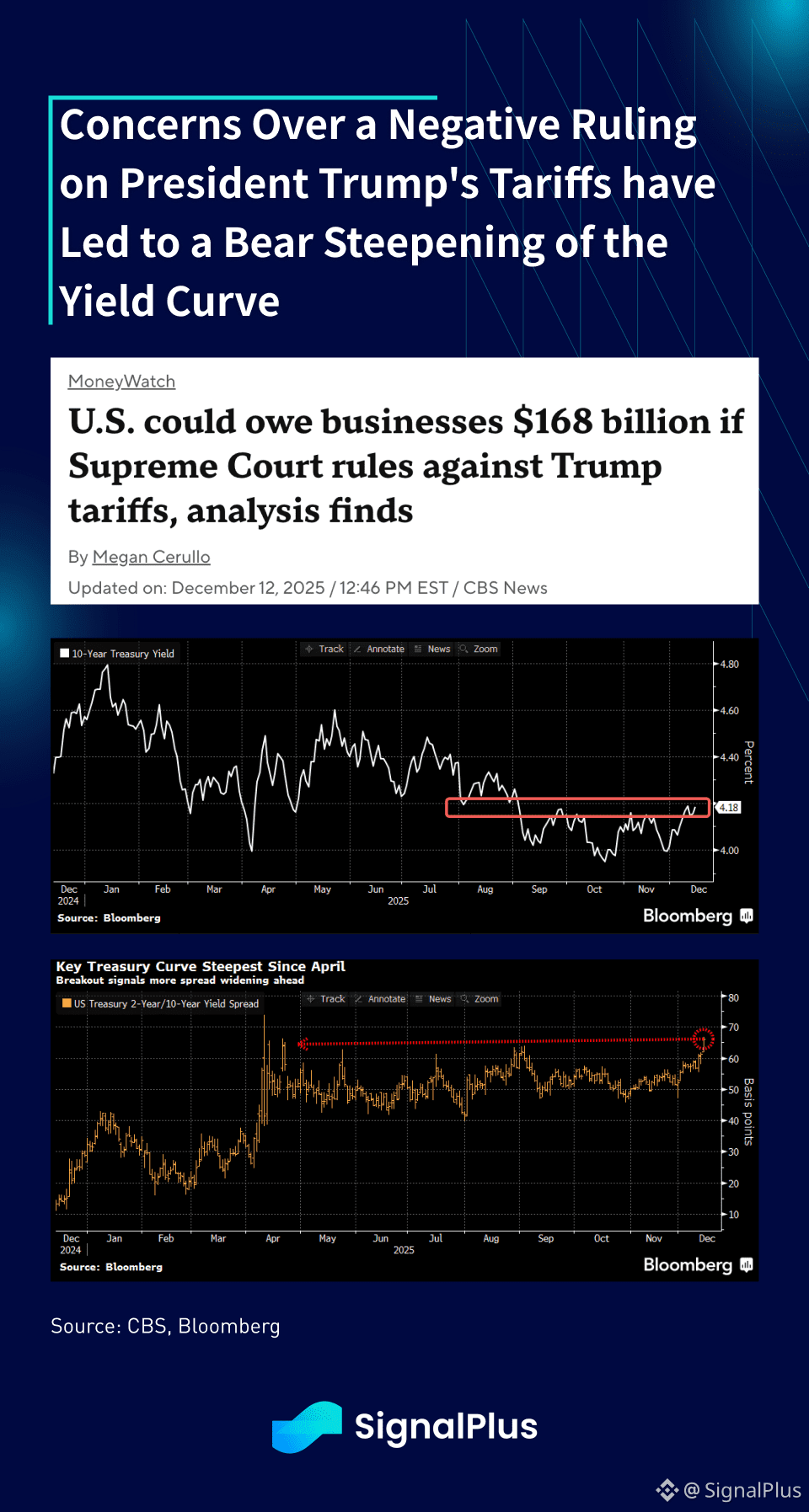

Furthermore, the Supreme Court is set to rule on President Trump’s tariff authority as early as this week, and a negative ruling would mean that the US government could owe ~$200b in refunds to importers over the next year. That would need to be funded out of further bond issuance, along with significant impact on the future government budget as tariffs were earmarked as a major revenue source. As a result, 10y yields tested and are looking to breach the multi-month ceiling at ~4.20%, with the 2/10s yield curve also steepening by ~15bp over the past 2 weeks alone.

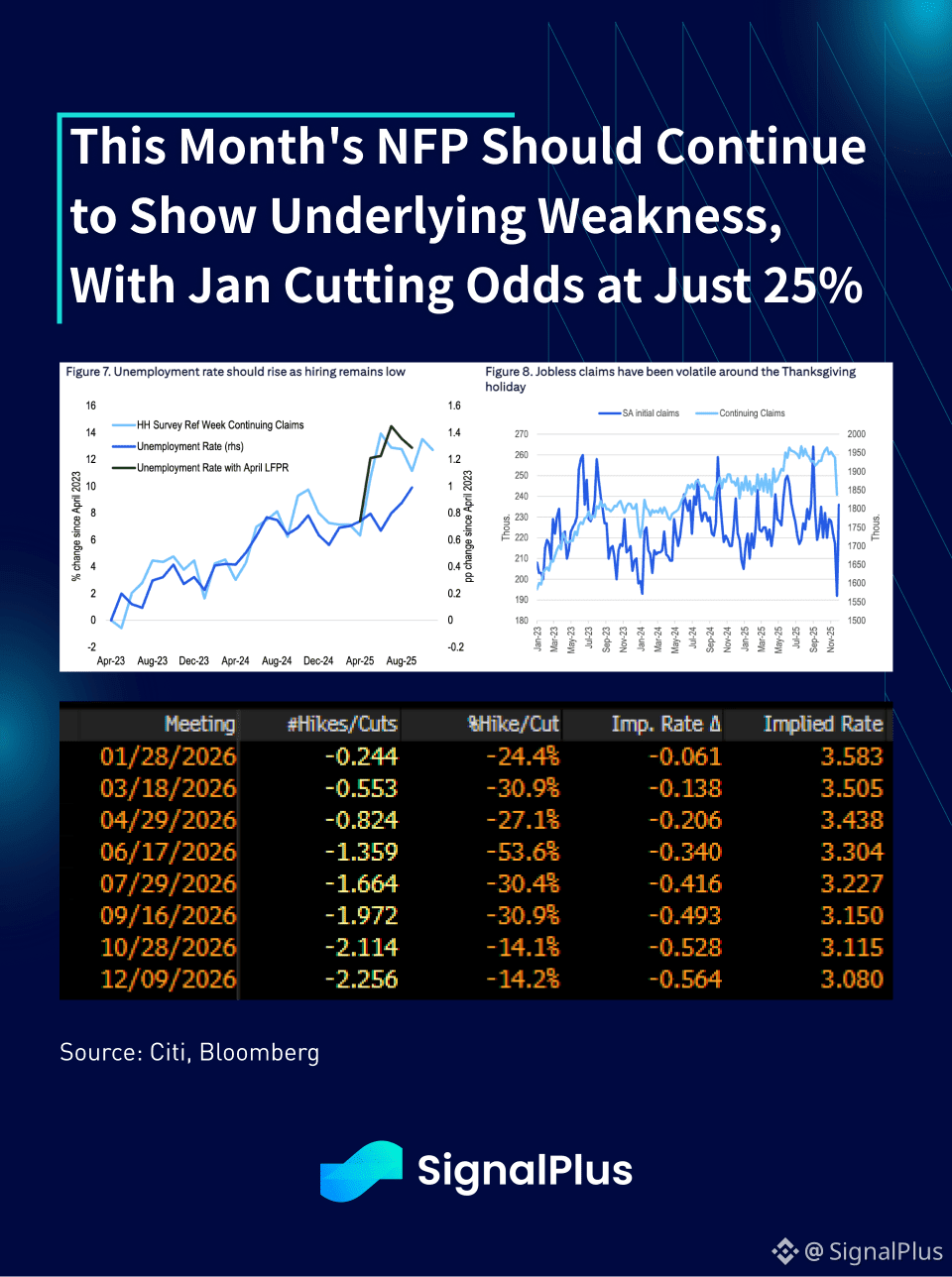

Furthermore, long-end yields are facing upward pressure from Hasset’s likely nomination as Fed chair, given his proclivity to easing polices, offsetting the dovish impact of the FOMC’s recent emphasis on downside employment risks. While the unemployment rate is likely to rise in this weeks’ NFP report, January cutting odds are at just ~25% at the moment, with the market still pricing in just over 2 cuts for all of 2026 at the moment.

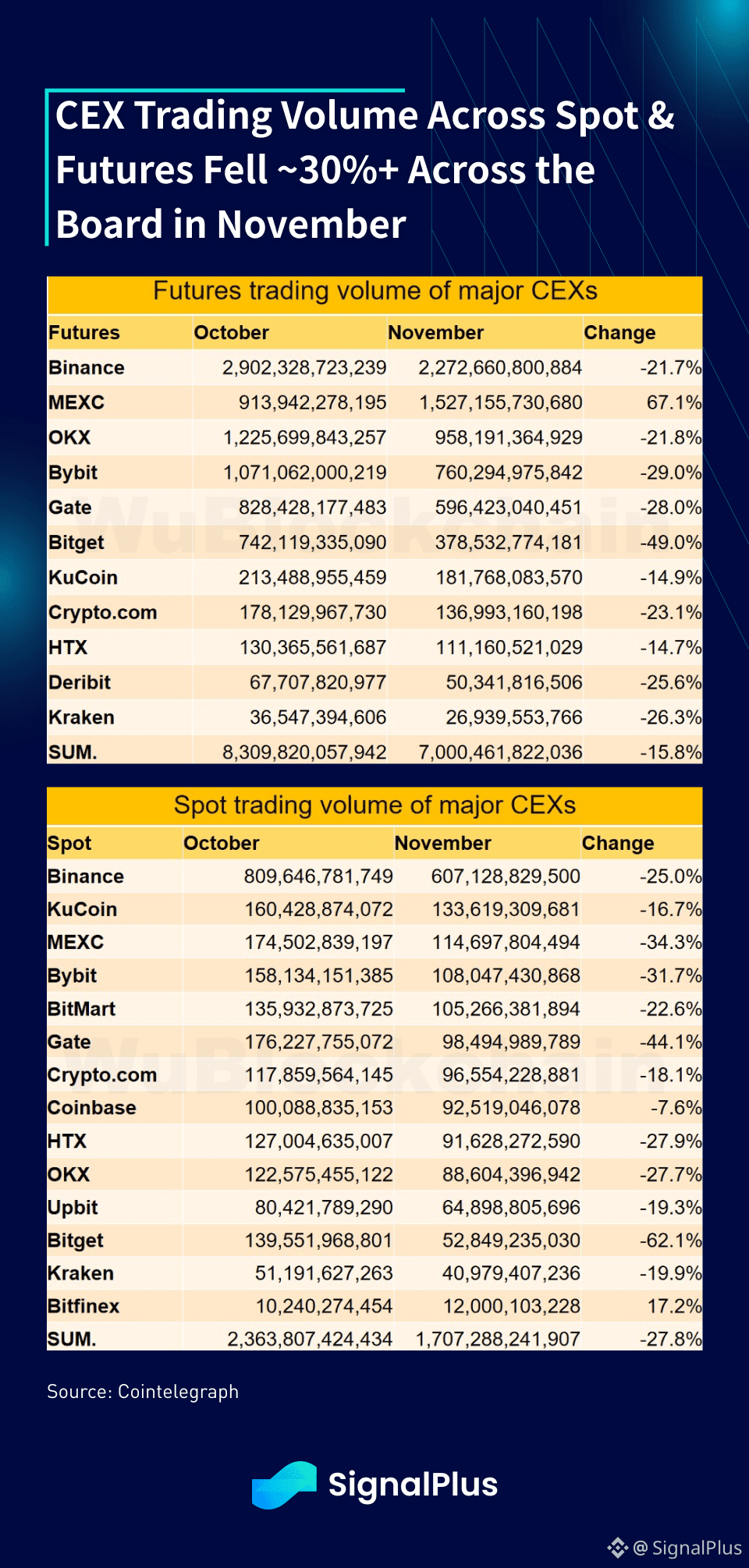

Crypto continued its recent streak of weakness as prices tumbled both on Friday and Monday on extremely thin liquidity conditions. Rumors of a large market-maker selling of inventory didn’t help matters, as the fallout from 10/10 continuing to rear its ugly head. As liquidity and trading volumes have dwindled noticeably in recent weeks, particularly in the OTC market, and BTC/ETH will be increasingly used as the hedging proxy as they are the only major tokens with any sort of institutional-sized liquidity.

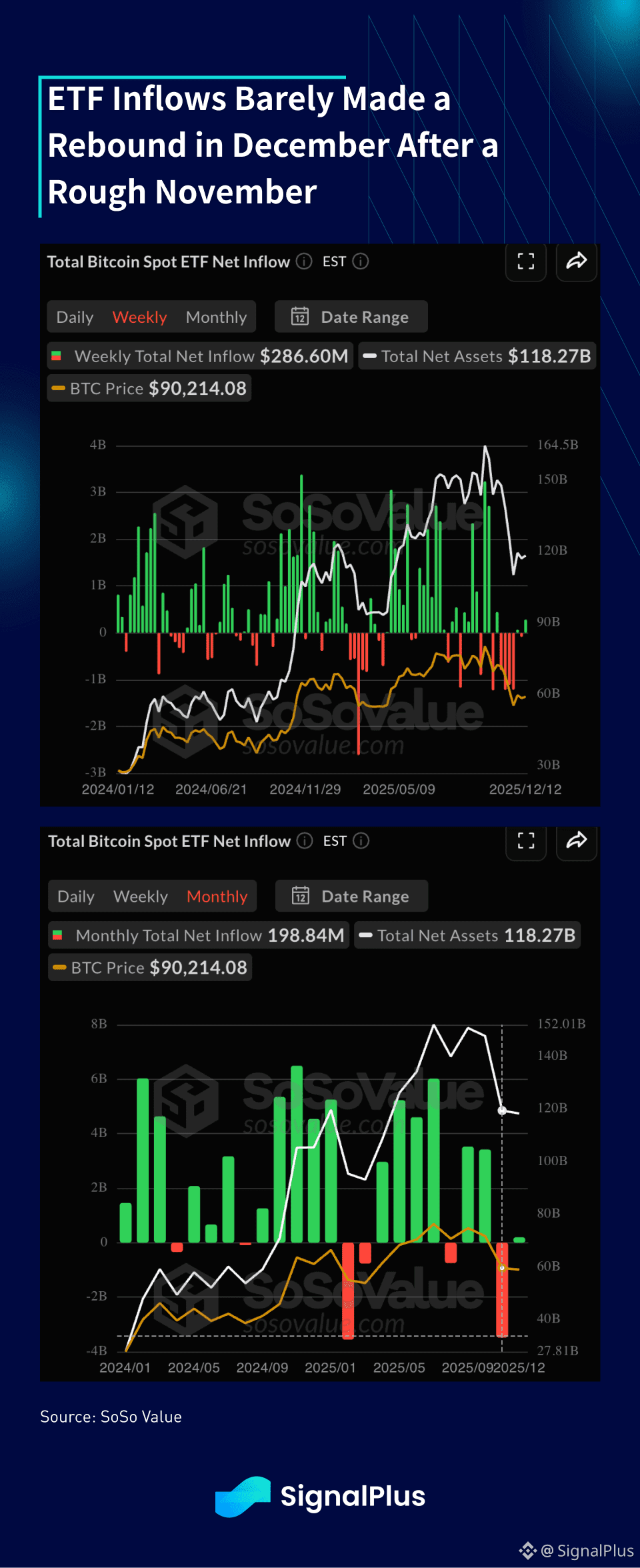

With global markets about to enter holiday mode, the 24/7 nature of crypto could be a detriment heading into year-end, with price movements likely to be exacerbated, particularly on further risk-offs and de-risking moves. ETF inflows made a tiny rebound last week following weeks of outflow, with December MTD numbers coming in at +0.2B vs -3.5B last month.

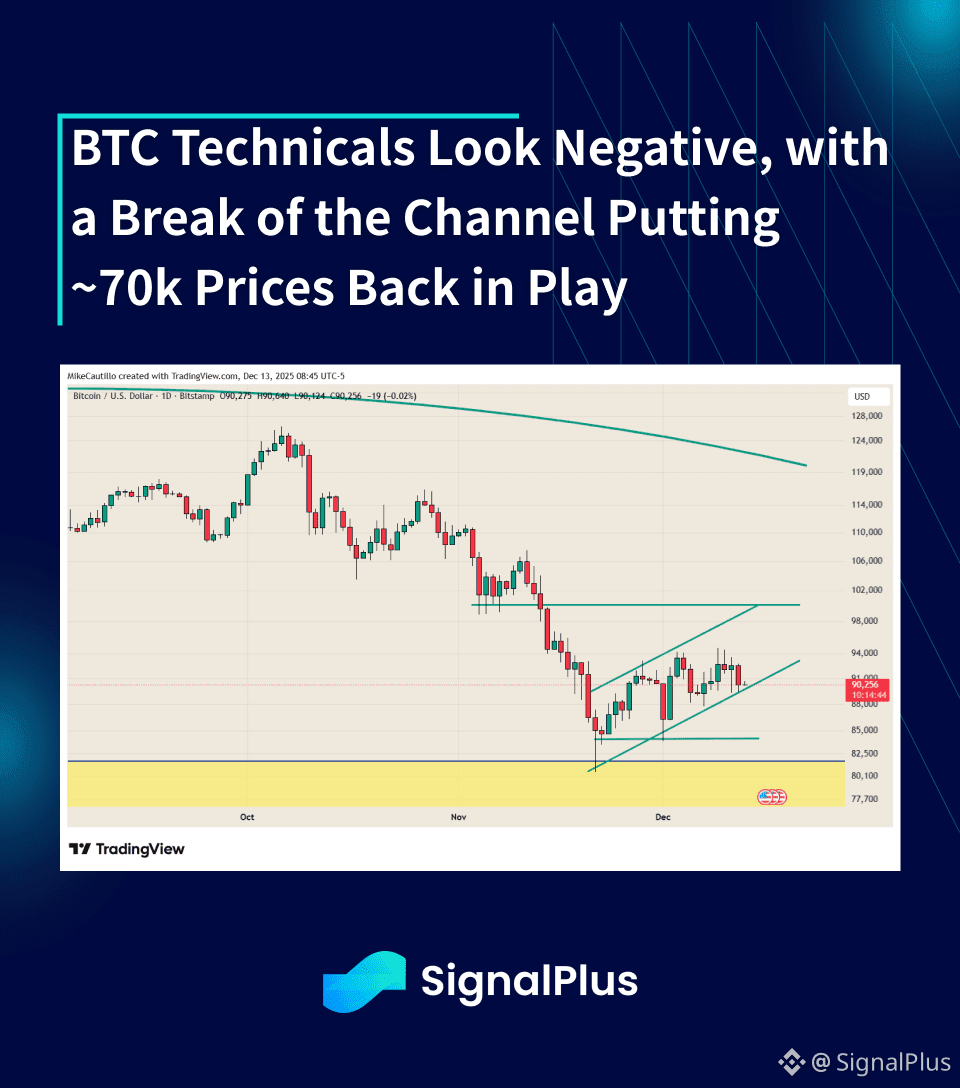

Technically speaking, price action still looks ominous, with a break of the current channel possibly putting ~70k prices back in play. Our bias remains negative, and would suggest extreme caution heading into CPI/NFP this week, especially amidst anemic holiday trading conditions.

Good trading & good luck!