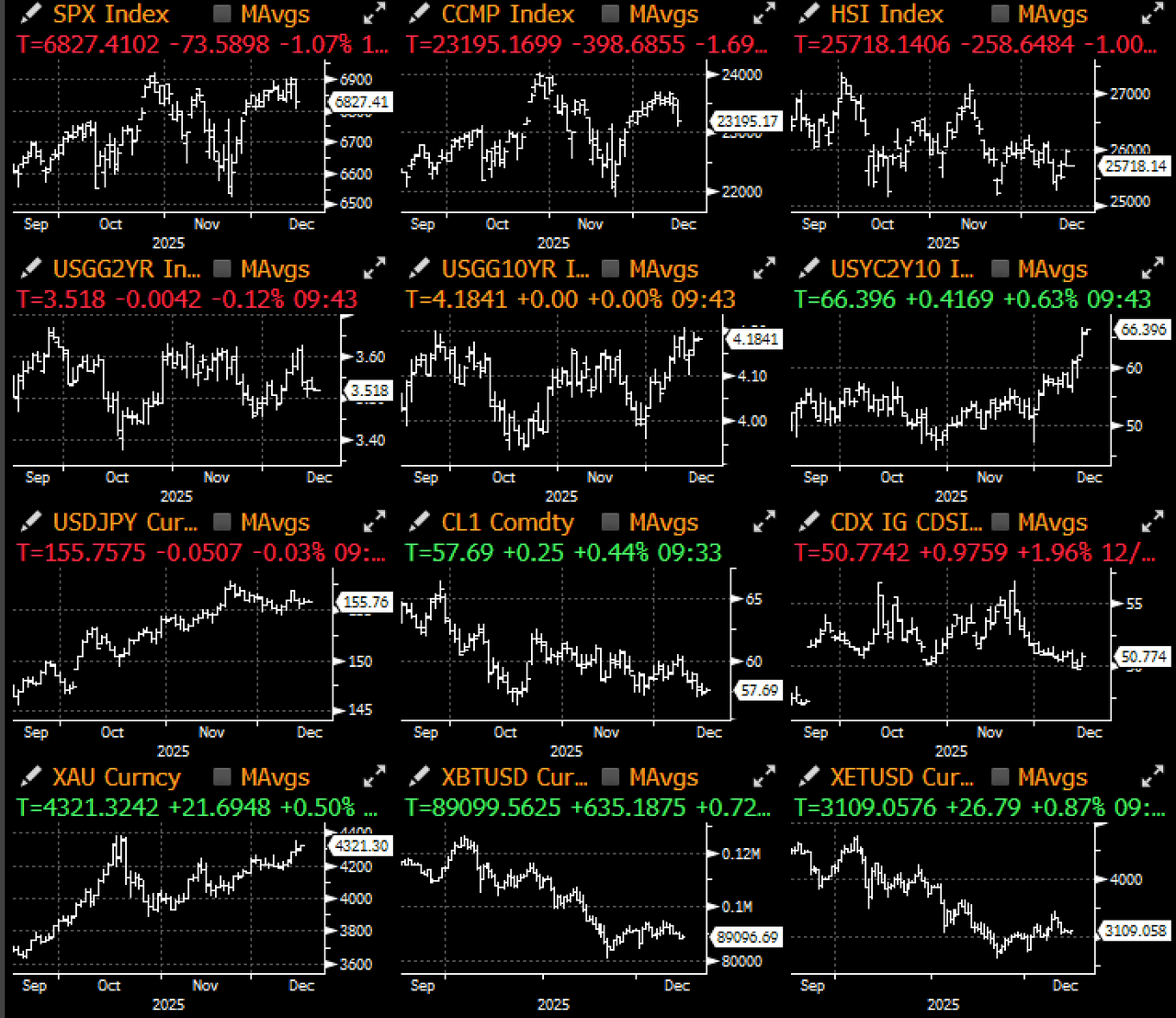

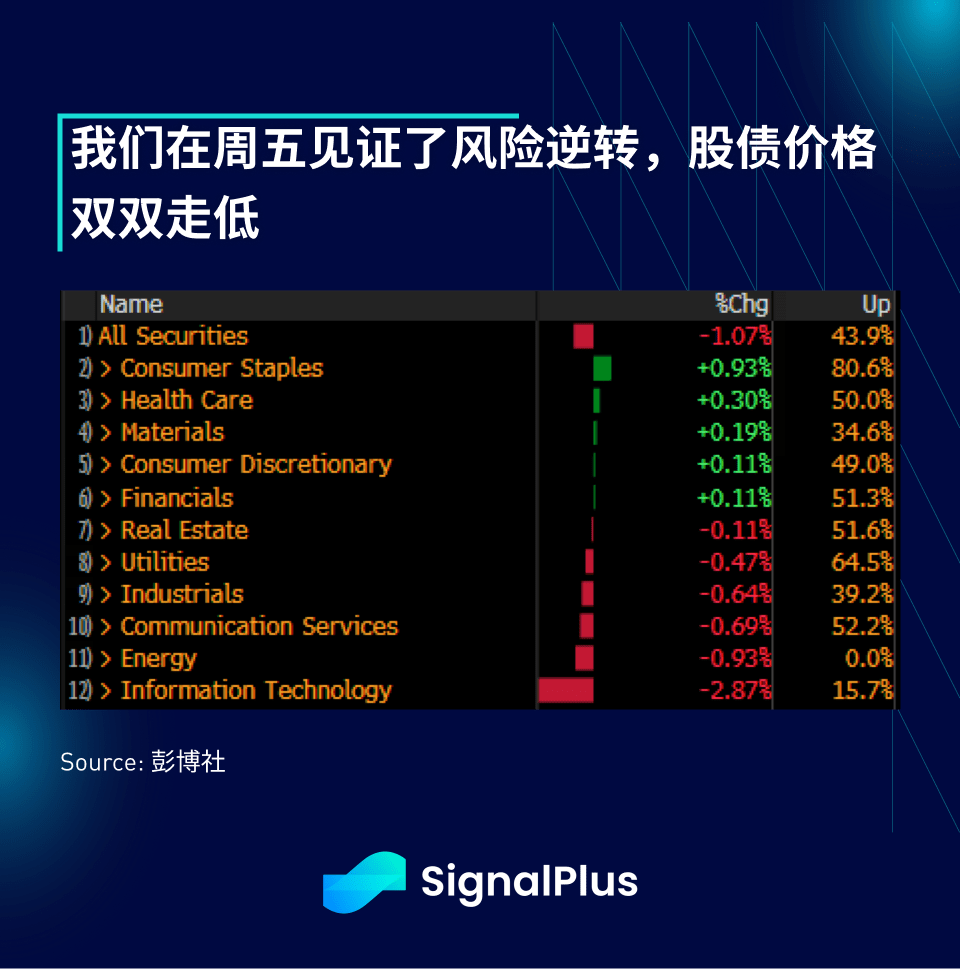

Last Friday, market risk sentiment reversed 180 degrees, with macro assets sold off across the board, and tech stocks leading the decline, resulting in a bear market steepening of the yield curve. Concerns about Oracle and Broadcom's earnings reports weighed on overall risk assets, while year-end profit-taking and sector rotation temporarily caused the Nasdaq index to drop by -2% intraday.

In addition, the Supreme Court will rule on President Trump's tariff authority as early as this week, and an unfavorable ruling could mean that the U.S. government will need to refund about $200 billion in tariffs to importers over the next year. This portion of funding will need to be raised through further bond issuance, significantly impacting future government budgets, as tariffs were originally designated as a primary source of revenue. As a result, the 10-year U.S. Treasury yield is testing and may break above approximately 4.20%, a multi-month high, and in just the past two weeks, the 2/10-year yield curve has steepened by about 15 basis points.

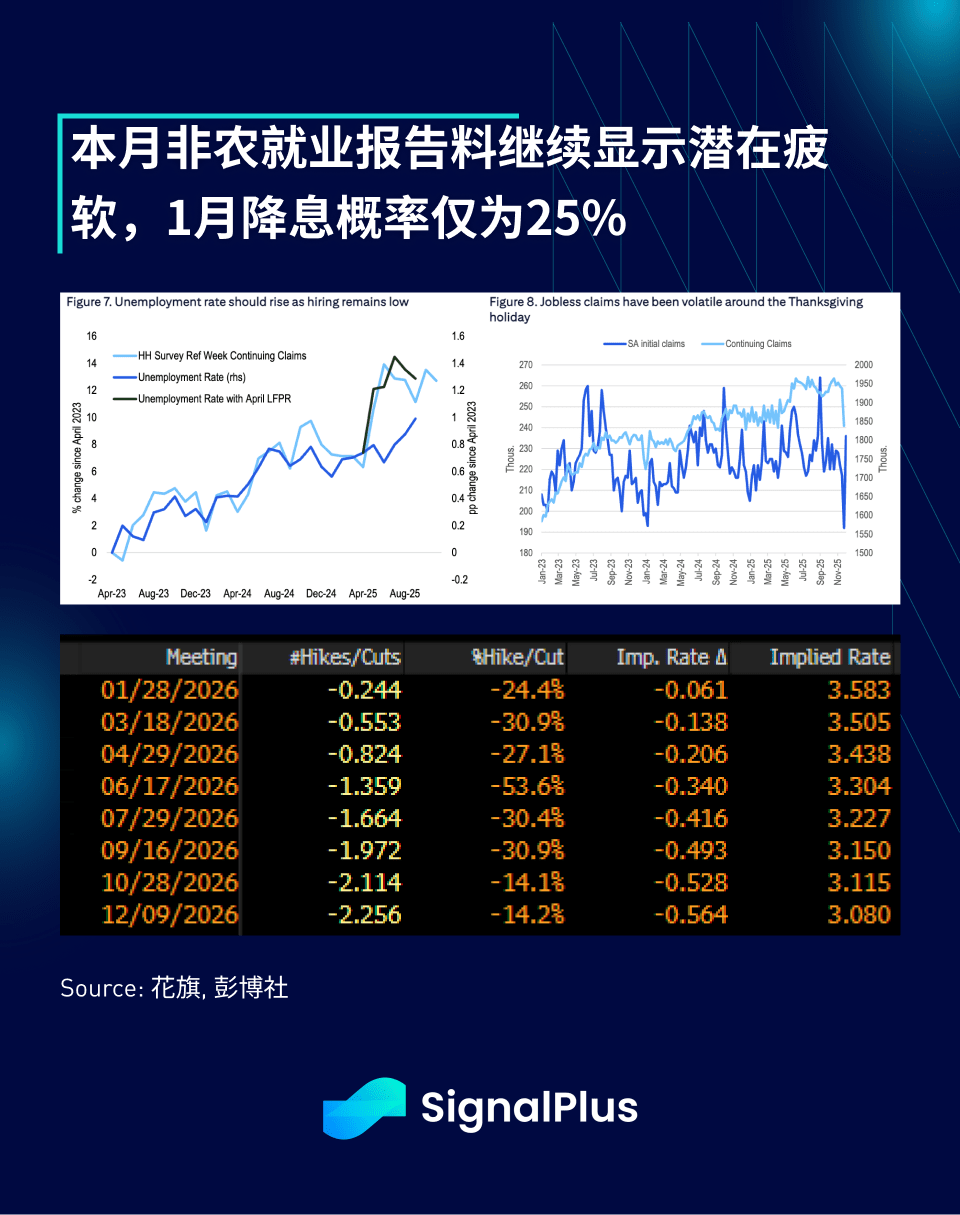

Additionally, long-term yields are facing upward pressure, as Harsit may be nominated as the Fed chair, whose inclination towards loose policies offsets the recent dovish impact of the Fed emphasizing the downside risks to employment. Although this week's non-farm employment report may show an increase in unemployment rate, the market is currently pricing in only about a 25% chance of a rate cut in January, and expectations for rate cuts throughout 2026 remain just slightly above 2.

Cryptocurrencies continue their recent weakness, with prices persisting in decline on Friday and Monday under extremely low liquidity conditions. Rumors of large market makers dumping inventory have compounded the situation, with the effects of the October 10 incident continuing to manifest. Liquidity and trading volume have noticeably shrunk in recent weeks, especially in the over-the-counter market, as BTC/ETH will increasingly be used as hedging alternatives since they are the only major tokens with institutional-scale liquidity.

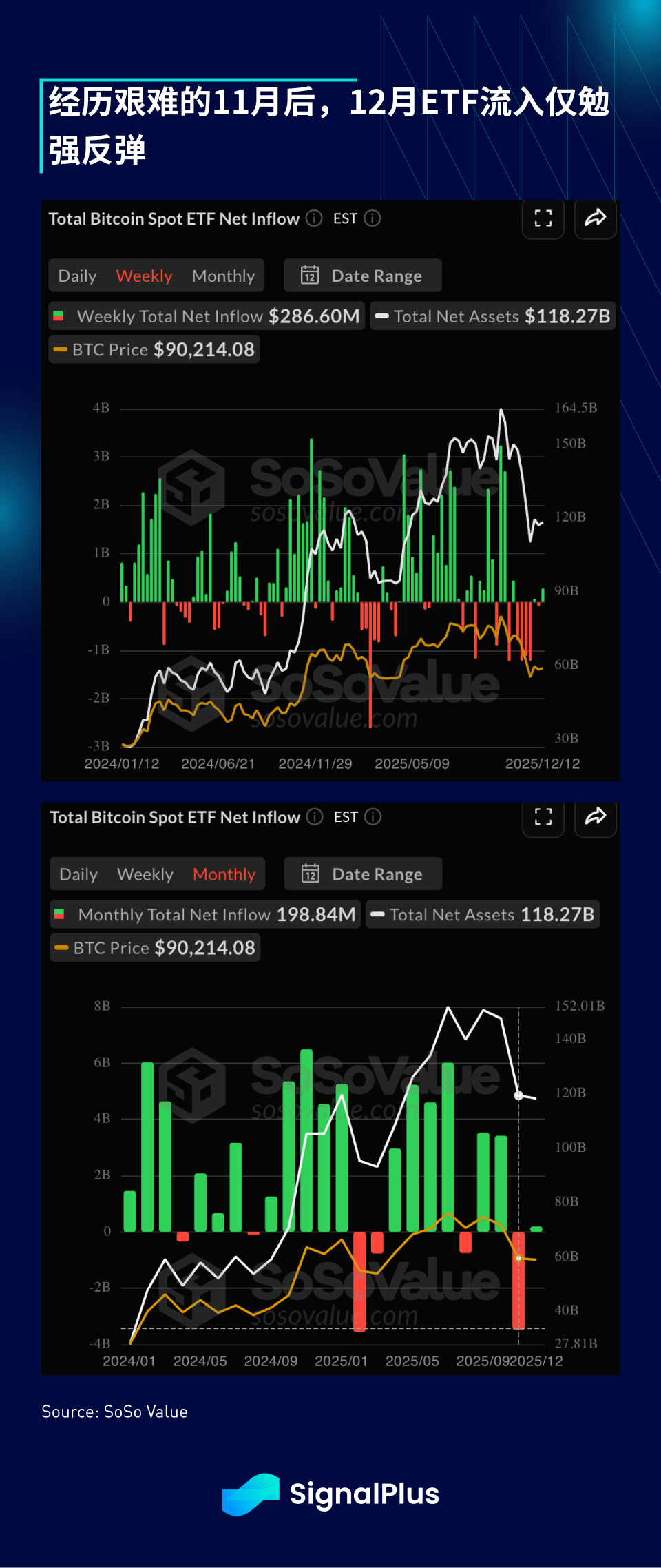

As the global market is about to enter holiday mode, the 24/7 trading characteristic of cryptocurrencies may become a disadvantage before the end of the year, with price fluctuations possibly intensifying, especially in further risk aversion and de-risking actions. After several weeks of capital outflows, ETF inflows rebounded slightly last week, with +0.2B inflows since December, compared to -3.5B last month.

From a technical perspective, the price trend remains perilous; if it breaks below the current channel, it may revisit the price level of about $70,000. We maintain a bearish outlook and recommend extreme caution ahead of this week's CPI/non-farm employment data release, especially in a light holiday trading environment.

Wishing you successful trades and good luck!