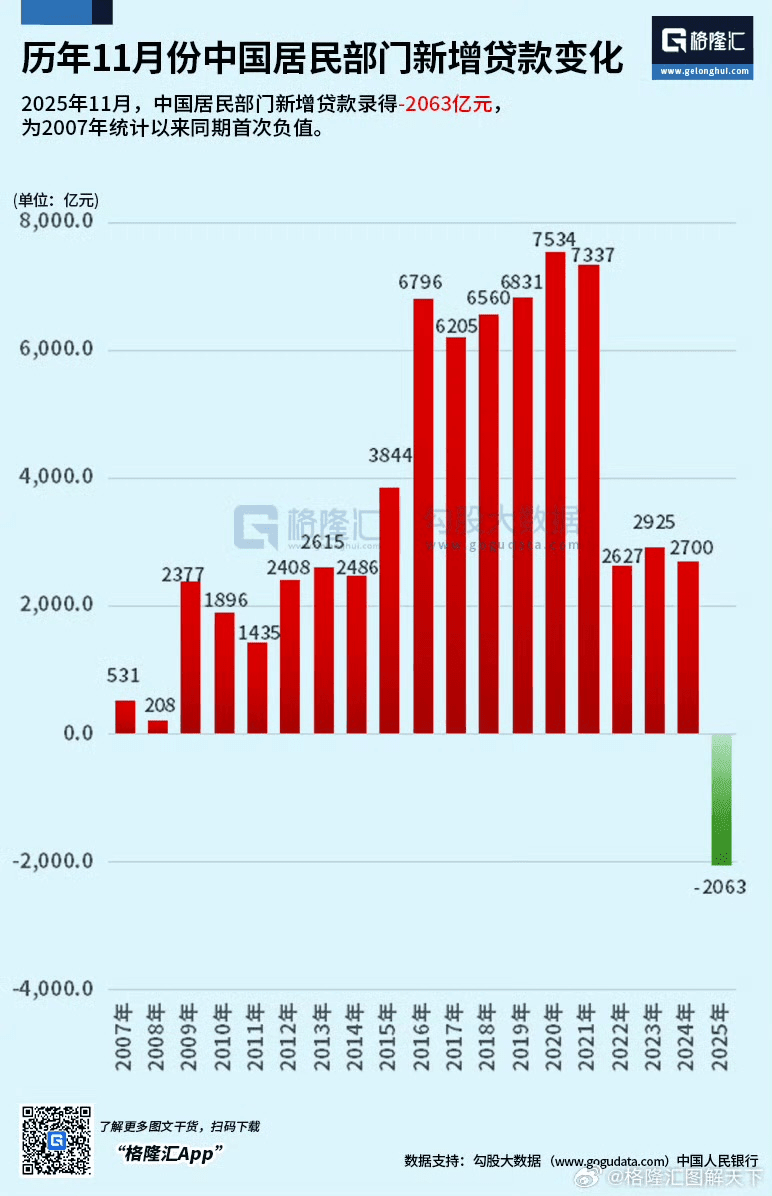

In November 2025, the new loans to the household sector in China recorded -2063 billion yuan, marking the first time since records began in 2007 that a negative value has occurred during the same period. Many people's first reaction is, 'Is it that banks are not lending?' or 'Is the data abnormal?' However, if we shift our perspective back to the behavior of households themselves, this number truly reveals a deeper and more serious change.

It signifies that households are systematically exiting the era of leveraging.

1. A negative value does not mean 'unable to borrow money,' but rather 'not wanting to borrow money.'

A negative new loan amount can only be explained in one logical way:

The total amount of loans repaid by residents this month is greater than the new borrowings.

This is not the result of tightening limits. On the contrary, over the past few years, mortgage interest rates have continued to decrease, down payment ratios have eased, and consumer and business loans have remained relaxed, but residents' reactions have been:

Prepaying the mortgage.

No longer replacing homes for improvement.

No longer using credit consumption.

Have cash to pay off debts rather than expand liabilities.

This is a proactive choice. The change in behavior is often more important than the data itself.

2. What has really changed is the judgment about the 'future.'

The premise of borrowing money has never been the interest rate, but the expectations.

As long as a family believes that future income will steadily grow and assets will appreciate over the long term, even if interest rates are slightly higher, they are willing to leverage. But now, more and more residents are beginning to form another consensus:

Income growth is unpredictable.

Employment stability is declining.

Real estate no longer has the 'bottom line' function.

Risks are almost entirely borne by individuals.

Under this judgment, the most rational behavior is not expansion but contraction.

Therefore, the new loans turning negative is essentially not about 'not having money to borrow,' but rather about 'not willing to stake the future.'

3. This is not the result of a recession, but rather a precursor to a recession.

Many people will ask: Is it already a decline in income and a surge in unemployment?

On the contrary, such credit data is usually a leading indicator. The real sequence is often:

Deteriorating expectations → Residents stop leveraging → Consumption and real estate decline → Corporate cash flow comes under pressure → Wage cuts and layoffs → Actual decline in resident income

In other words, residents' behaviors have already shifted to defense ahead of time, while the pain felt from macro data often gradually appears later.

This is why this signal is particularly important—it occurs at a stage where 'people haven't fully felt the pain yet.'

4. The financial logic of real estate is failing completely.

For the past twenty years, there has been a very clear chain in the Chinese economy:

Residents leverage to buy houses → Housing prices rise → Local finances expand → Investment and employment → Leverage again.

And now, this chain has broken at the very front.

When residents are no longer willing to take on long-term debt, real estate ceases to be an expansionary force and turns into a source of contraction. Even if policies continue to ease, the effect will clearly diminish because the issue is no longer about 'conditions' but rather about 'beliefs.'

5. Will this create a vicious cycle?

The answer is: We have already entered a negative feedback zone, but it is not a sudden collapse; rather, it is a chronic contraction.

Residents deleverage → Insufficient consumption and investment → Corporations cut costs → Employment and income come under pressure → Expectations further weaken → Even less willing to leverage.

This process will not fall off a cliff like a financial crisis, but more like 'long-term blood loss.' The system is still operating, but growth momentum has clearly declined, and the overall risk appetite of society continues to decrease.

6. The real watershed is not in the data, but in people's hearts.

The first negative new loans are significant not so much for their scale, but because they mark a transition of an era:

Shifting from 'exchanging the future for the present' to 'preserving the present to guard against the future.'

This is not an emotional panic but a form of collective rational self-protection.

In such an environment, any methods that purely rely on stimulus will become increasingly ineffective. The only two things that can truly change the trend are stable and predictable income growth and a credible risk-sharing mechanism for the future.

Before this, residents choosing to contract was not a mistake, but a calm response to reality.

SO:

The negative turn in new loans for residents is not a signal that the economy has bottomed out, but rather a sign that society as a whole is entering a defensive state. The real challenge has just begun.