Author: @BlazingKevin_, the Researcher at Movemaker

SEC Chairman Paul Atkins pointed out that the entire U.S. financial market, including stocks, fixed income, government bonds, and real estate, may fully migrate to a blockchain technology architecture supporting cryptocurrencies within the next two years. This can be said to be the most significant structural change in the U.S. financial system since the advent of electronic trading in the 1970s.

1. Comprehensive on-chain cross-departmental collaboration framework and actual contributions

The 'Project Crypto' initiative promoted by Atkins is not a unilateral action by the SEC; it is based on systematic cooperation across legislation, regulation, and the private sector. The full on-chain integration of the U.S. financial market, valued at over $50 trillion (including stocks, bonds, government securities, private credit, real estate, etc.), requires multiple institutions to clarify their roles and contributions.

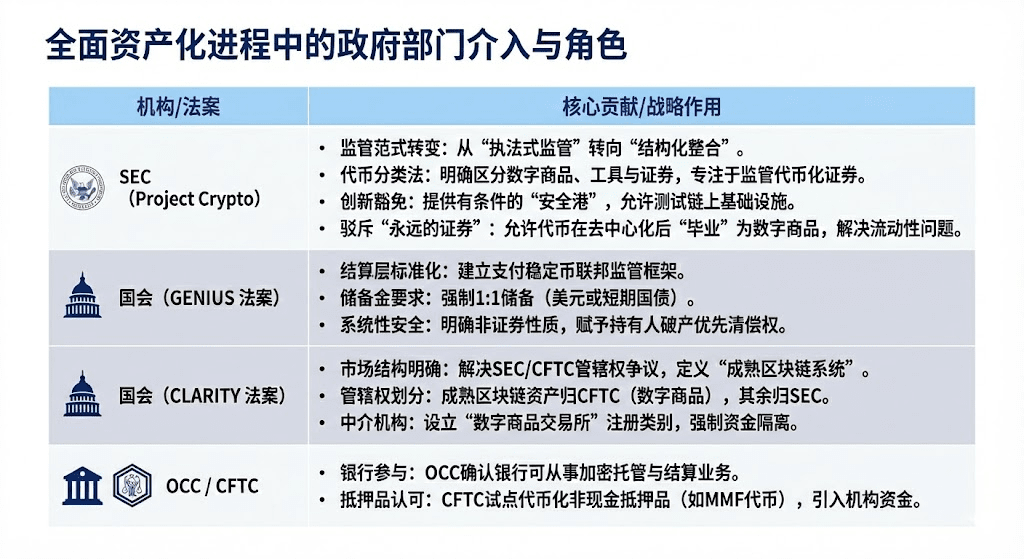

1.1 Government departments that will be involved in comprehensive assetization

It should be noted that the 'Project Crypto' and 'innovation exemption' mechanisms acknowledge the incompatibility of blockchain technology with existing financial regulations, providing a controlled experimental environment that allows traditional financial institutions (TradFi) to explore and implement tokenization infrastructure without violating core investor protection principles.

The GENIUS Act clarifies the regulatory authority transferred to banking regulators by creating compliant, fully reserved-backed stablecoins, addressing the Cash Leg issue necessary for institutions to conduct transactions and collateralization on-chain.

The CLARITY Act clarifies the jurisdiction between the SEC and CFTC, specifically targeting crypto-native platforms and creating a definition of 'mature' that enables institutions to clearly understand under which regulatory framework their digital assets (like Bitcoin) operate, while providing a pathway for crypto-native platforms to register as federal regulatory intermediaries ('brokers/dealers').

The OCC was established in 1973 to provide clearing and settlement services for options, futures, and securities lending transactions, promoting market stability and integrity. The CFTC is the main regulator of the futures market and futures traders.

This cross-sector collaboration is a prerequisite for the comprehensive on-chain implementation of the U.S. financial market and lays a solid foundation for the large-scale deployment by giants like BlackRock and JPMorgan, as well as the integration of core infrastructures like DTCC.

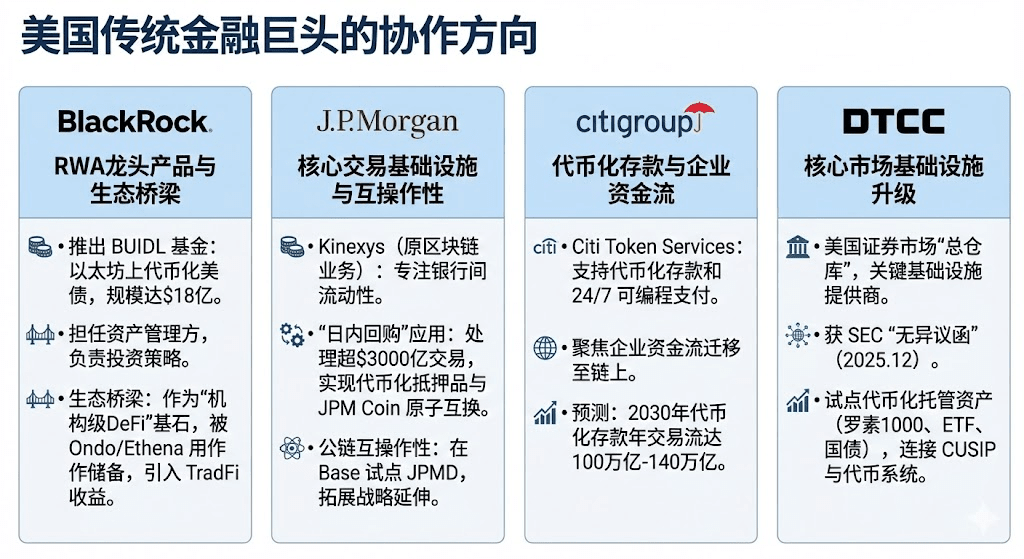

2.2 Collaboration of traditional financial giants

In the collaborative blueprint of traditional U.S. financial giants, the deepening layout of various institutions reflects more specific strategic focuses and technical details. BlackRock is the first to issue a tokenized U.S. Treasury fund on a public chain (Ethereum), establishing its foundational position as an asset manager introducing traditional financial returns into the public chain ecosystem.

After renaming its blockchain business to Kinexys, JPMorgan allows banks to complete atomic swaps of tokenized collateral and cash within hours rather than days, significantly optimizing liquidity management; at the same time, its pilot of JPMD on the Base chain is seen as a strategic step towards extending into a broader public blockchain ecosystem, aiming for stronger interoperability.

Finally, the specific breakthrough of the custody trust and clearing company (DTCC) is completed by its subsidiary, the custody trust company (DTC). As the world's most important trading infrastructure provider, its SEC no-action letter enables it to connect the traditional CUSIP system with the new token infrastructure, thereby officially launching pilot projects for mainstream asset tokenization, including Russell 1000 component stocks, in a controlled environment.

2. Analysis of the financial environment and impacts after comprehensive tokenization

The core goal of asset tokenization is to break the 'island effect' and 'time constraints' of traditional finance, creating a global, programmable, and around-the-clock financial system.

2.1 Significant enhancements in the financial environment: leaps in efficiency and performance

Tokenization will bring efficiency and performance advantages that traditional financial systems cannot match:

2.1.1 Leap in settlement speed (from T+1/T+2 to T+0/seconds):

Enhancement: Blockchain can achieve near real-time (T+0) or even second-level settlements and deliveries, contrasting sharply with the typical T+1 or T+2 settlement cycles required by traditional financial markets. The digital bonds issued by UBS on SDX showcase T+0 settlement capabilities, and the European Investment Bank's issuance of digital bonds has also shortened settlement times from five days to one day.

Pain points addressed: Greatly reduces the counterparty credit risk and operational risk caused by settlement delays. For time-sensitive transactions like repos and derivatives margins, the speed of settlement is crucial.

2.1.2 The revolution in capital efficiency and release of liquidity:

Enhancement: Achieves 'atomic delivery,' meaning assets and payments occur simultaneously in a single, indivisible transaction. At the same time, through tokenization, it can release 'sleeping capital' currently locked in settlement waiting periods or inefficient processes. For example, programmable collateral management can release over $100 billion of trapped capital annually.

Pain points addressed: Eliminates principal risk in traditional 'delivery versus payment' operations. Reduces the need for high-margin buffers at clearinghouses. At the same time, tokenized money market funds (TMMFs) can be directly transferred as collateral, retaining yields and avoiding liquidity friction and yield loss caused by the need to redeem cash for reinvestment in traditional systems.

2.1.3 Enhancement of transparency and auditability:

Enhancement: Distributed ledgers provide a single, immutable authoritative record of ownership, with all transaction histories being public and verifiable. Smart contracts can automatically execute compliance checks and corporate actions (such as dividends).

Pain points addressed: Completely resolves the inefficiencies of data silos, multiple accounting, and manual reconciliations in traditional finance. It provides regulators with an unprecedented 'God view' to conduct real-time, penetrating oversight and effectively monitor systemic risks.

2.1.4 24/7/365 global market access:

Enhancement: The market is no longer limited by traditional banks' working hours, time zones, or holidays. Tokenization makes cross-border transactions smoother, allowing assets to be transferred peer-to-peer on a global scale.

Pain points addressed: Overcomes the time lags and geographical constraints in traditional cross-border payments and liquidity management, especially benefiting cash management for multinational companies.

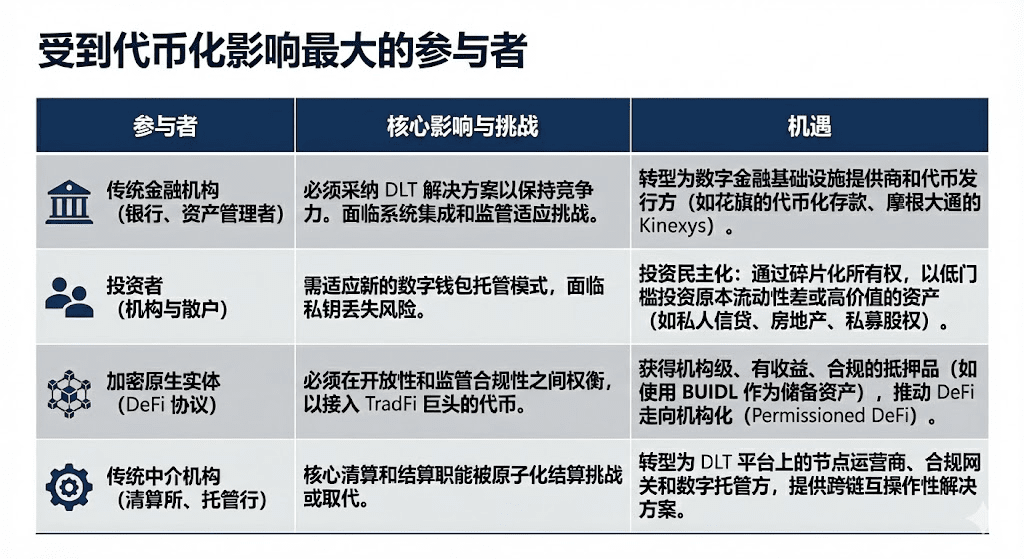

2.2 The participants most affected

The transformations brought by tokenization are disruptive and have the greatest impact on the following categories of market participants:

Main challenges and risks:

Trade-offs between liquidity and net settlement: DTCC currently reduces the actual amount of cash and securities that need to be transferred by 98% through net settlement of millions of transactions, achieving tremendous capital efficiency. Atomic settlement (T+0) is essentially real-time gross settlement (RTGS), which may lead to a loss of net settlement efficiency, requiring the market to find hybrid solutions between speed and capital efficiency, such as intraday repos.

Privacy paradox: Institutional finance relies on trade privacy, while public chains (like Ethereum) are transparent. Large institutions cannot execute block trades on public chains without being 'front-run.' The solution is to adopt privacy-preserving technologies like zero-knowledge proofs or operate on permissioned chains (like JPMorgan's Kinexys).

Amplification of systemic risk: 24/7 markets eliminate the 'calm period' of traditional markets. Algorithmic trading and automated margin calls (via smart contracts) may trigger large-scale chain liquidations under market pressure, thereby amplifying systemic risk, similar to the liquidity pressures seen in the 2022 UK LDI crisis.

2.3 The core value embodiment of tokenized funds (TMMF)

The tokenization of money market funds (MMFs) is the most representative case in the growth of RWA. TMMFs as collateral are particularly attractive:

Retention of yields: Unlike non-interest-bearing cash, TMMFs as collateral can continuously earn yields until actually used, reducing the opportunity cost of 'collateral drag.'

High liquidity and composability: TMMFs combine the regulatory familiarity and safety of traditional MMFs with the instant settlement and programmability brought by DLT. For example, BlackRock's BUIDL fund addresses the pain point of T+1 redemption required by traditional MMFs through Circle's USDC instant redemption channel, achieving 24/7 instant liquidity.

3. The role of DTCC/DTC in the tokenization process

DTCC and DTC are indispensable core systemic institutions in the U.S. financial infrastructure. The assets held by DTC are substantial, covering the vast majority of stock registrations, transfers, and custody in the U.S. capital markets. DTCC and DTC are seen as the 'total warehouse' and 'total ledger' of the U.S. stock market. The involvement of DTCC is crucial in fundamentally ensuring the compliance, security, and legal validity of the tokenization process.

3.1 The core role and responsibilities of DTC

Identity and scale: DTC is responsible for central securities custody, clearing, and asset services. As of 2025, the asset scale held by DTC reached $100.3 trillion, covering 1.44 million securities issues and dominating the registration, transfer, and confirmation of most stocks in the U.S. capital market.

Tokenization bridge and compliance guarantee: DTCC's involvement represents the official recognition of traditional financial infrastructure for digital assets. Its core responsibility is to act as a trust bridge between the traditional CUSIP system and the emerging tokenization infrastructure. DTCC commits that tokenized assets will maintain the same high levels of security, robustness, legal rights, and investor protection as their traditional forms.

Liquidity integration: DTCC's strategic goal is to achieve a single liquidity pool between the TradFi (traditional finance) and DeFi (decentralized finance) ecosystems through its ComposerX platform suite.

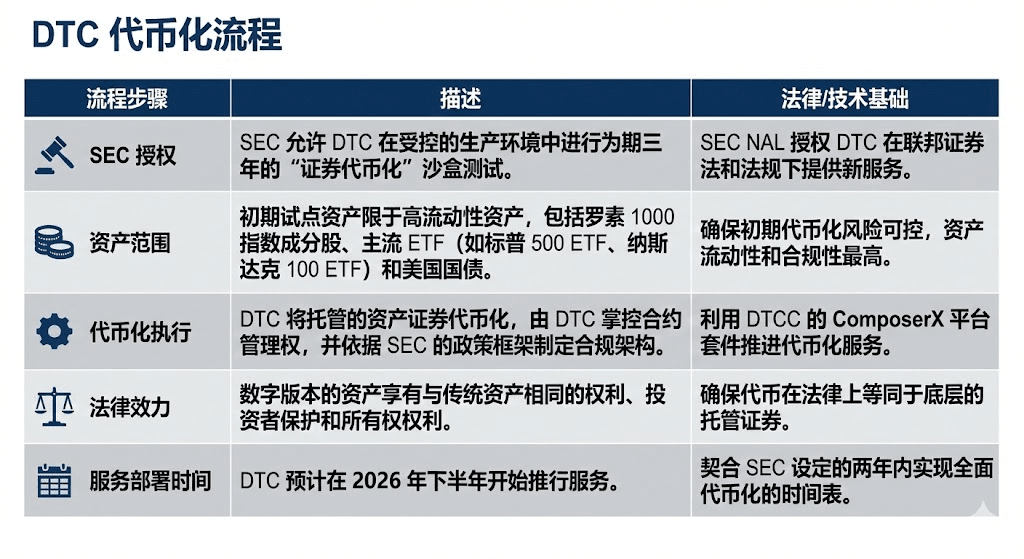

3.2 DTC tokenization process and SEC no-action letter

In December 2025, DTC, a subsidiary of DTCC, obtained a landmark no-action letter from the U.S. SEC, which serves as the legal foundation for its large-scale promotion of tokenization business.

3.3 The impact brought by DTC tokenization

The approval of DTC NAL is considered a milestone in tokenization, mainly impacting:

Certainty of official tokens: DTC's tokenization means that tokenized stocks officially backed by the U.S. are on the horizon. Future projects that tokenize U.S. stocks may directly access DTC's official asset tokens rather than building their own asset on-chain infrastructure.

Market structure integration: Tokenization will drive the U.S. stock market towards a model of 'CEX + DTC Custody Trust Company.' Exchanges like Nasdaq may directly take on the role of CEX, while DTC manages token contracts and allows withdrawals, fully unlocking liquidity.

Enhanced collateral liquidity: DTC's tokenization service will support enhanced collateral liquidity, achieving 24/7 access and asset programmability. DTCC has been exploring the use of DLT technology to optimize collateral management for nearly a decade.

Eliminating market fragmentation: Stock tokens are no longer a digital type isolated from traditional assets but are fully integrated into the general ledger of traditional capital markets.

About Movemaker:

Movemaker is the first official community organization authorized by the Aptos Foundation and jointly initiated by Ankaa and BlockBooster, focusing on promoting the construction and development of the Aptos ecosystem in the Chinese-speaking region. As the official representative of Aptos in this region, Movemaker is dedicated to building a diverse, open, and prosperous Aptos ecosystem by connecting developers, users, capital, and numerous ecosystem partners.

Disclaimer: This article/blog is for reference only, representing the author's personal views and does not represent the position of Movemaker. This article does not intend to provide: (i) investment advice or recommendations; (ii) offers or solicitations to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. Holding digital assets, including stablecoins and NFTs, carries high risks, significant price volatility, and may even become worthless. You should carefully consider whether trading or holding digital assets is suitable for you based on your financial situation. For specific issues, please consult your legal, tax, or investment advisor. The information provided in this article (including market data and statistics, if any) is for general reference only. Reasonable care has been taken in compiling these data and charts, but no responsibility is accepted for any factual errors or omissions expressed therein.