Aave's price has dropped, but the story is far from over.

The recent market performance of Aave (#AAVE ) does not appear to be friendly. The price fell more than 10% in a short time, while trading volume suddenly surged, skyrocketing 226% within 24 hours to reach 577 million dollars. On the surface, it looks like a typical panic sell-off, but if you zoom out, you'll find that things are not so simple.

The direct trigger of market volatility was a 'whale' selling approximately 17 million dollars worth of AAVE-related assets. This action quickly amplified the negative sentiment in the market, particularly impacting long positions in perpetual contracts. As prices declined, longs were forced to liquidate, ultimately leading to 1.59 million dollars in long positions being liquidated, significantly increasing short-term selling pressure.

However, a price decline does not necessarily mean a weakening of the fundamentals; Aave's on-chain data tells a different story.

In panic, funds continue to flow in.

Against the backdrop of a generally panic sentiment in the crypto market, Aave's capital flows appear particularly eye-catching. According to DeFiLlama's data, from December 18 to date, Aave's total locked value (TVL) has increased by approximately $1.42 billion.

The significance of this number is not low. Because when market sentiment cools, a large amount of capital chooses to enter DeFi protocols and actively lock up, it often means that investors are not betting on short-term rebounds but are wagering on longer-term value returns. This return includes both the yield provided by the protocol itself and expectations of future price recovery.

The choice of funds to enter Aave, rather than remaining in stablecoin pools or exiting to observe, indicates that market participants still have high confidence in Aave's core value and long-term positioning.

Fees and income are still very strong.

From an operational perspective, Aave's performance remains robust. In just the past 24 hours, the protocol generated approximately $1.88 million in fee income, while the total fees over the past seven days reached $11.58 million. This continuous ability to generate fees indicates that the real borrowing demand from users still exists, and the protocol has not been 'neglected' due to price declines.

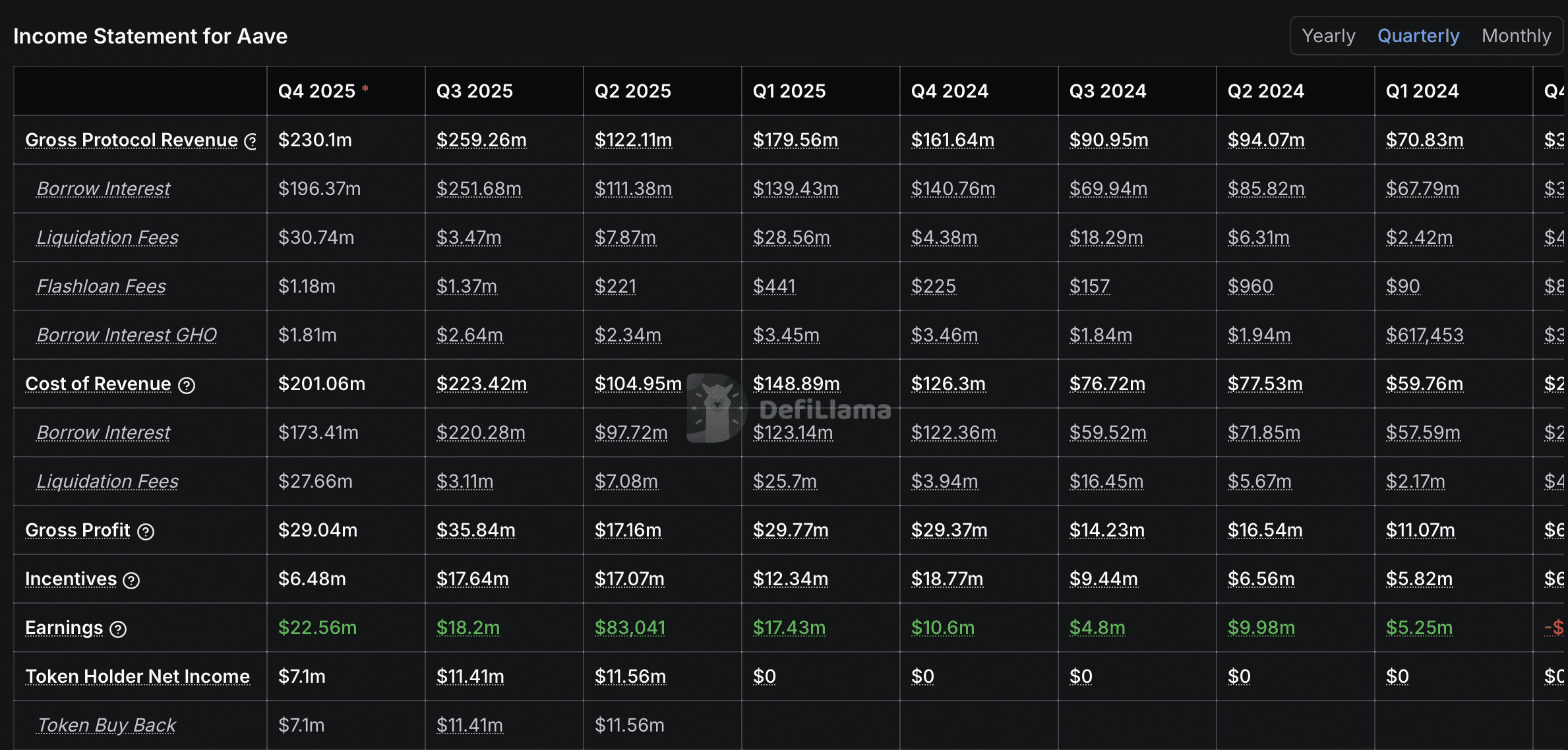

More notably, profitability. Aave achieved a profit of $22.56 million in Q4 2025, which is the net income after deducting incentive expenditures, setting a quarterly record in the protocol's history. This data implies that Aave is no longer just 'usable' but has truly entered a stage of efficient profitability.

The improvement in profitability often brings about a chain reaction. More and more investors tend to hold or accumulate AAVE instead of frequently selling during short-term fluctuations, gradually reducing the market's circulating supply, which usually supports prices in the medium to long term.

Holders are still making money.

From the perspective of token holders, the situation is also not pessimistic. Data shows that net income for AAVE holders this quarter to date is approximately $7.11 million. Although this number has declined compared to the previous two quarters, it remains positive, indicating that holding AAVE is not merely 'pure faith' but still offers realistic returns.

Such data often reinforces the willingness of long-term investors to hold positions and further explains why, despite price pressures, there is still a large amount of capital choosing to flow into the protocol.

A cooling of on-chain activity may not be a bad thing.

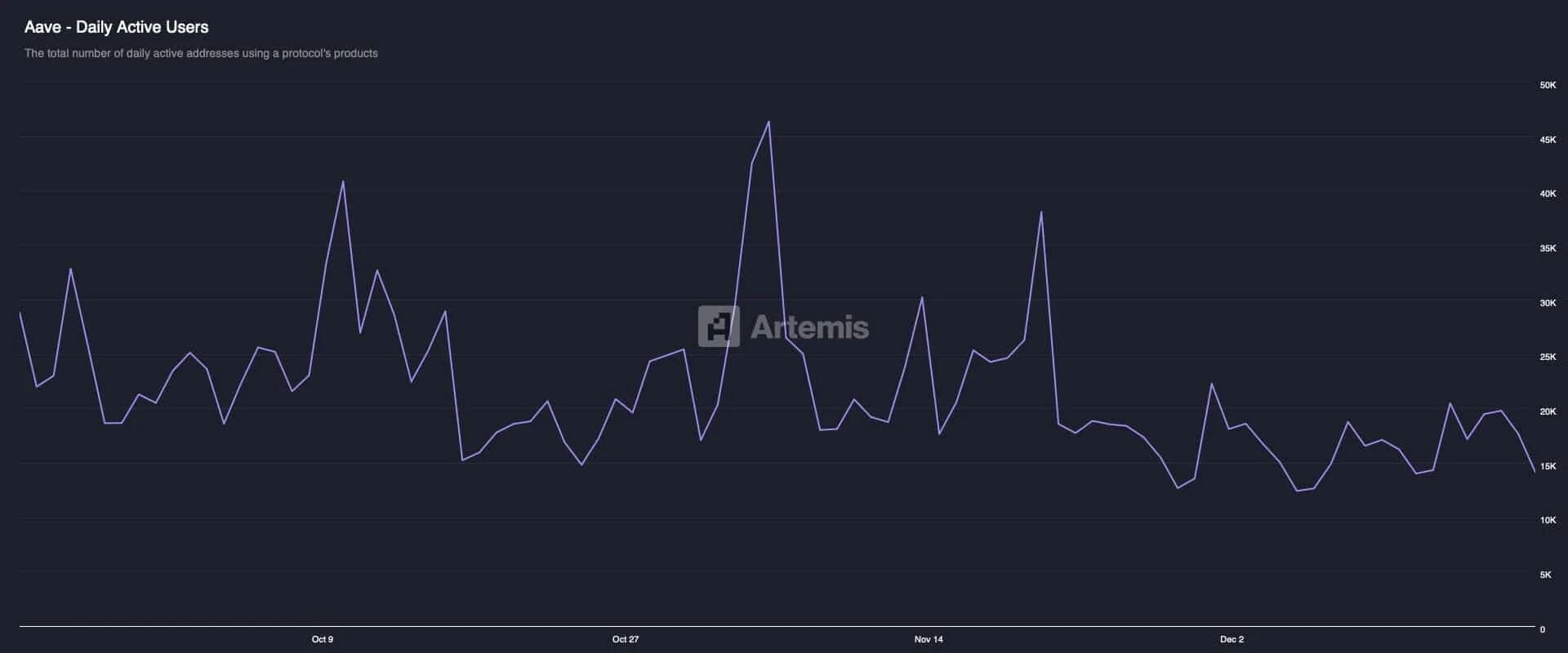

Of course, not all indicators are strengthening synchronously. Artemis's data shows that Aave's daily transaction volume and active user count have both recently declined, with on-chain participation slightly slowing compared to earlier.

However, it is important to note that this decline in activity coincides with a significant increase in TVL. This combination is not necessarily bearish; it may indicate that short-term traders are exiting, leaving behind funds that are willing to lock up long-term and have more confidence in the protocol.

If the overall market sentiment improves subsequently, those temporarily observing users may return, which could bring a new round of activity and capital to Aave.

Short-term price vs long-term fundamentals.

Overall, Aave currently presents a typical 'price and fundamentals divergence' state. In the short term, whale sell-offs and derivative liquidations have indeed pressured prices, but in terms of on-chain capital inflow, fee income, and profitability, Aave's performance is closer to that of a mature institution-level protocol.

To summarize a few key points: Aave recorded approximately $1.4 billion in capital inflow during the market panic phase, quarterly profits reached an all-time high, and fee income remains stable. These data remind the market that under short-term fluctuations, Aave's fundamentals have not collapsed but have quietly strengthened.