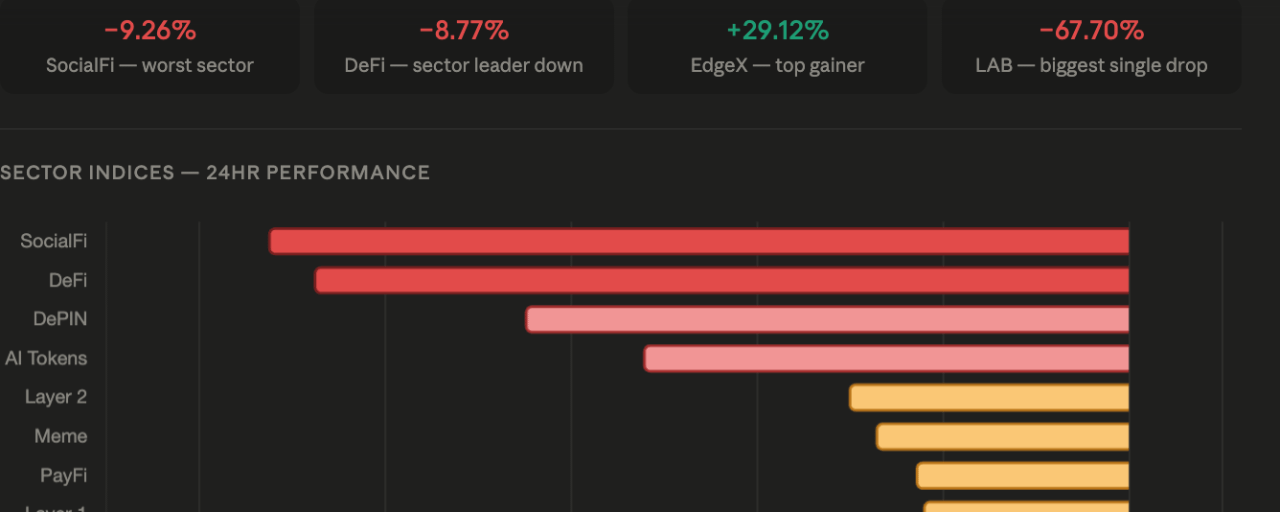

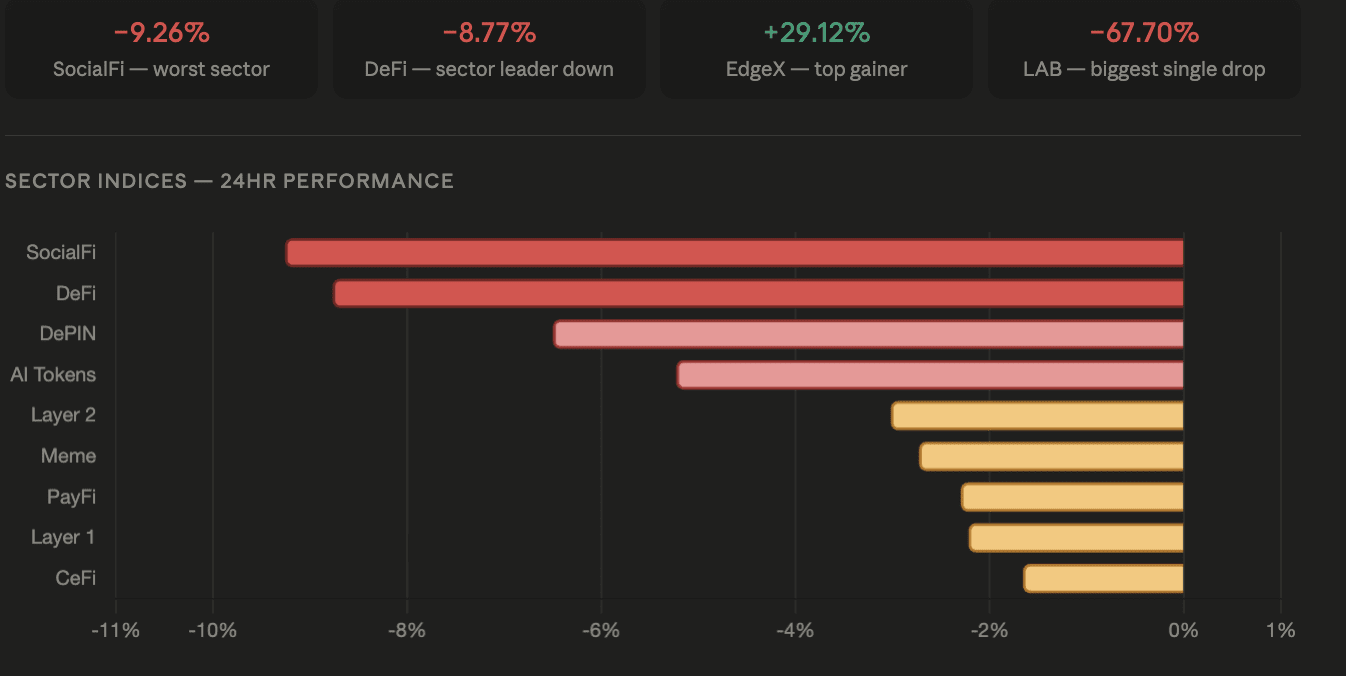

The cryptocurrency market declined across the board over the past 24 hours, with most sectors posting losses between 2% and 9%. The DeFi sector led declines at 8.77%, followed by SocialFi at 9.26%, DePIN at 6.50%, and AI tokens at 5.23% — three of the four worst-performing sector indices all tied to the infrastructure and application layers that had been the most hyped narratives of the current cycle.

Sector Breakdown

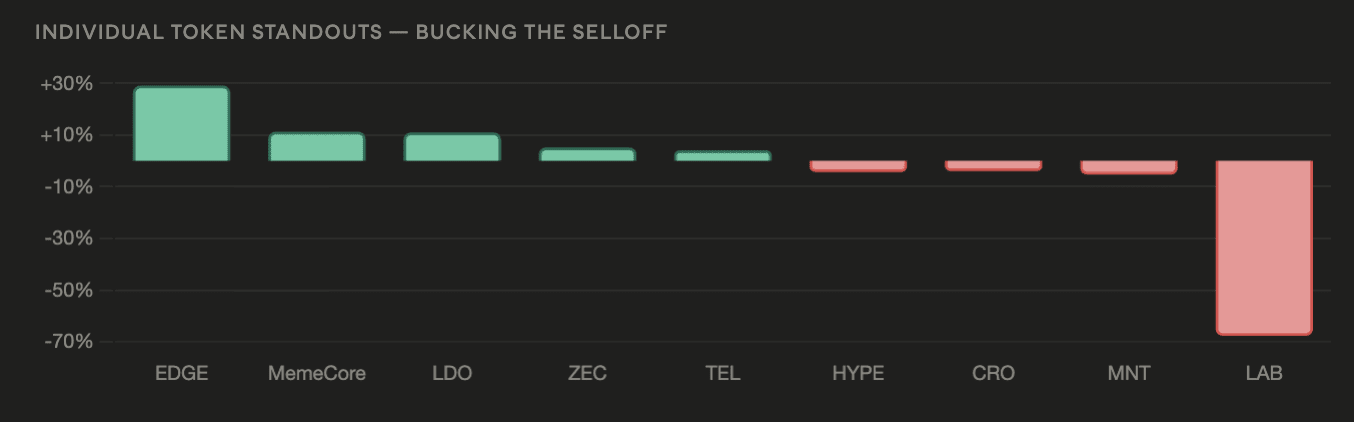

DeFi's 8.77% decline was the headline sector loss, with LAB falling 67.70% — the sharpest individual decline in the data — while HYPE dropped 4.30%. The countermovers were EdgeX gaining 29.12% and Lido DAO rising 11.01% — both on token-specific catalysts rather than sector sentiment.

The CeFi sector fell 1.66% with Cronos down 3.91% — a comparatively modest decline reflecting the relative stability of centralized exchange tokens versus more speculative DeFi protocols. Layer 1 declined 2.22%, with Zcash rising 5.17% as the privacy coin narrative continues its recent outperformance against the broader bear market. The PayFi sector dropped 2.30%, though Telcoin gained 4.11% — another token-specific catalyst bucking sector weakness. The Meme sector fell 2.73% while MemeCore added 11.30%. Layer 2 declined 3.02% with Mantle down 5.31%.

The Broader Context

Monday's broad sector decline fits within the macro pressure that has been building this week — the JGB yield surge to a 30-year high at 2.85% pushing US Treasury yields to test 4.5%, a fresh Hormuz missile strike reviving oil risk, and the KOSPI crashing 6.7% as Samsung fell 8.3%. The SocialFi, DePIN, and AI sector indices falling 9.26%, 6.50%, and 5.23% respectively reflect the same AI trade unwinding that has driven semiconductor stocks lower — assets most exposed to the AI infrastructure narrative are seeing the sharpest corrections as investors reassess whether the spending justifies the valuations.

The token-specific standouts — EdgeX at +29.12%, MemeCore at +11.30%, Lido DAO at +11.01%, Telcoin at +4.11%, Zcash at +5.17% — follow the pattern that has characterized the entire June-July correction: broad sector weakness with isolated fundamental catalysts producing outlier gains in individual tokens independent of macro direction.