Virtual asset OTC operators will now need formal licensing to operate!

Not just a trading platform, the entire virtual asset business chain—from over-the-counter (OTC) exchanges, investment advice, to asset management—will now be subject to unified regulation.

Is this paving the way for large-scale capital entry?

Recently, the Hong Kong Securities and Futures Commission (SFC) and the Financial Services and the Treasury Bureau (FSTB) jointly released new regulations on virtual asset supervision, sparking widespread attention in the industry.

The core change is this: the previous focus on regulating trading platforms is now expanding to cover the entire business chain—from OTC trading and investment advice to asset management—under a unified licensing system.

To this, many people's first reaction is 'another layer of approval needed,' but upon closer reading, it becomes clear that the regulators' intent is not to create barriers, but to establish a clear, stable, and predictable regulatory framework.

This system not only improves upon the previous VATP regime but also sends a clear signal of certainty to institutional and long-term capital.

In other words, Hong Kong is not retreating, but laying the groundwork for larger-scale compliant capital to enter. For institutions genuinely committed to long-term development here, the question is no longer 'whether to get a license,' but how to best leverage this regulatory framework.

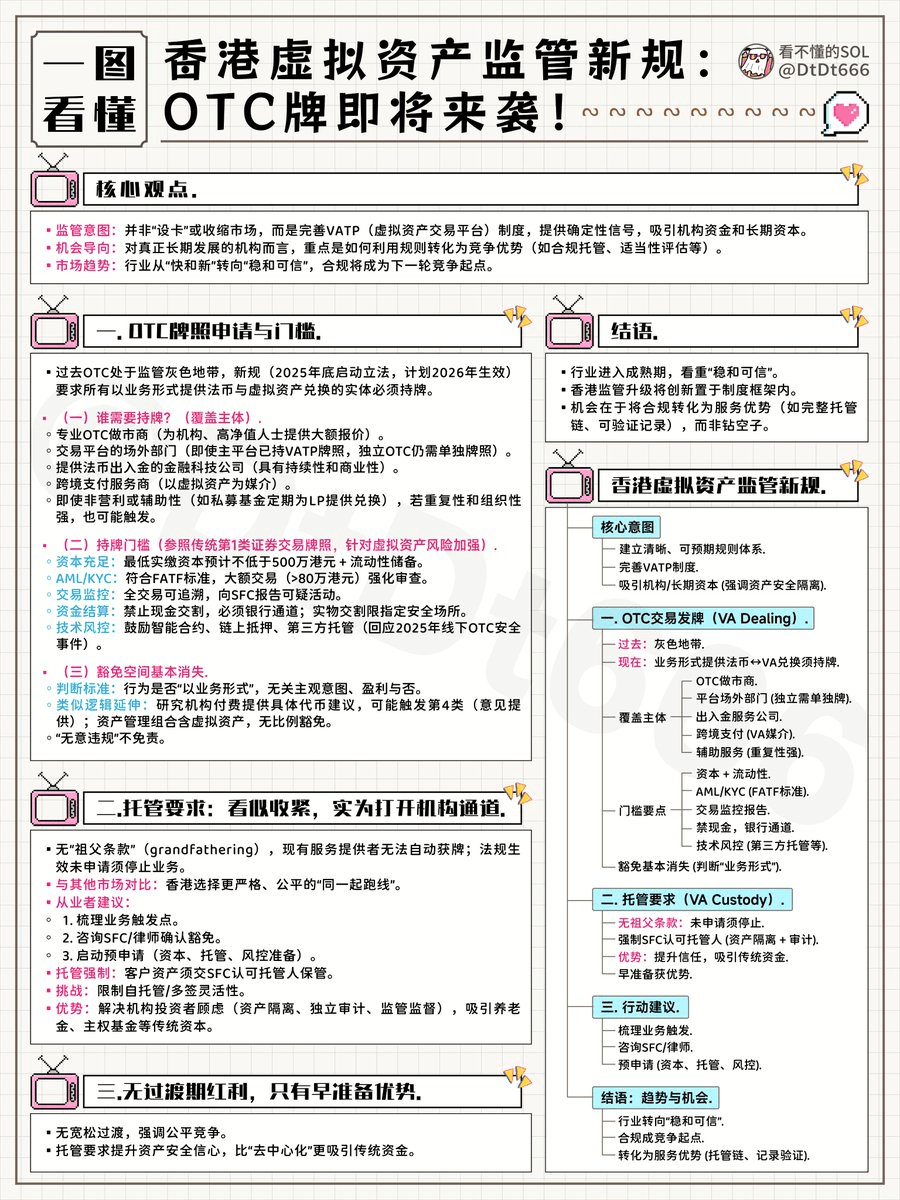

I. How to Obtain an OTC License? What is the Entry Barrier?

In the past, over-the-counter (OTC) trading of virtual assets long existed in a regulatory gray zone. Many institutions believed that as long as they did not directly operate an exchange面向 the public, they did not need to apply for a license.

However, this perception was completely shattered by the end of 2025 — the Securities and Futures Commission (SFC) and the Financial Services and the Treasury Bureau jointly announced the launch of legislative procedures for a licensing regime targeting virtual asset OTC dealers.

The new rules clearly state: any entity that provides large-scale fiat-to-virtual asset exchange services to clients in a business-like manner, regardless of profitability, self-description as a 'technology platform' or 'matching intermediary,' constitutes a regulated activity and must apply for a license.

This means OTC business has officially moved from 'self-regulated exploration' into the 'legally licensed' era.

(I) Who Needs a License? Which Entities Are Covered by Regulation?

The core regulatory criterion is not subjective intent or revenue model, but whether the activity is conducted in a 'business-like manner.' Accordingly, the following types of entities will fall under the licensing requirement:

1. Professional OTC Market Makers: Provide buy/sell quotes for large volumes of mainstream assets like Bitcoin and Ethereum to institutional clients, family offices, or high-net-worth individuals;

2. OTC departments of trading platforms: Even if the main platform already holds a Virtual Asset Trading Platform (VATP) license, if its large-scale trading or fiat channels operate as independent business lines, a separate OTC license is still required;

3. Fintech companies providing fiat on/off-ramp services: If they essentially provide two-way exchange services between virtual assets and fiat currencies, and possess continuity and commercial characteristics;

4. Cross-border payment or remittance service providers: If virtual assets are used as an intermediary to facilitate cross-border fund transfers, this may trigger licensing requirements. Notably, even non-profit or auxiliary services, if repetitive and organized, may be deemed regulated activities. For example, a private equity fund providing BTC/USD exchange services to its limited partners (LPs) as an added value, even without separate charges, may still be considered engaged in OTC business.

(II) Licensing Threshold: Not Just 'Submitting Documents,' but Systematic Compliance Capability Building

The proposed OTC license will be modeled after the traditional Securities Class 1 (Securities Trading) license framework, but with higher and more specific compliance requirements tailored to the unique risks of virtual assets:

1. Capital Adequacy: Applicants must maintain a minimum paid-in capital (expected to be no less than HK$5 million) and possess liquidity reserves capable of withstanding market volatility and counterparty defaults;

2. Anti-Money Laundering and KYC System: Must establish customer due diligence processes compliant with FATF international standards, and conduct enhanced scrutiny on large transactions (e.g., single transactions exceeding HK$800,000);

3. Transaction Monitoring and Reporting Mechanism: All transactions must be traceable and auditable, and reported to the SFC as required in cases of suspicious activities;

4. Fund Settlement Security: Cash settlement is strictly prohibited. Licensed OTC dealers must complete fiat settlements through regulated banking channels; if physical delivery is necessary, it must occur in designated vaults or approved secure locations;

5. Technology Risk Management Capability: Encourages the use of smart contracts, on-chain collateralization, or third-party custody mechanisms to reduce human operational risks — a direct response to the offline OTC security vulnerabilities exposed by the HK$100 million cash heist incident in December 2025.

(3) 'Unintentional violation' is not a免责 reason: the room for exemption has virtually disappeared

A key detail in the new regulations is that whether an activity constitutes a regulated one depends on whether the behavior itself is conducted in a 'business-like manner,' not on whether the entity intended to engage in financial services or whether it profited from it.

The same logic applies to other virtual asset businesses.

For example, if a research institution regularly sends weekly market reports containing specific token purchase recommendations to paying subscribers, even without charging a separate 'investment advisory fee,' as long as this service is part of its regular business operations, it may be deemed to be engaged in Category 4 regulated activity (providing advice on virtual assets).

Similarly, even if a family office's investment portfolio includes only 3% Bitcoin, it can no longer rely on the previously ambiguous loophole of 'small holdings exempt.'

The new rules explicitly eliminate such proportional exemptions, sending a clear signal: risks do not disappear due to small scale, and responsibilities cannot be waived on the grounds of 'unintentional violation.' No platform or institution can avoid compliance obligations by claiming 'we never intended to do financial business.'

II. Custody Requirements Appear Tightened, But Actually Open the Door for Institutional Capital

Notably, the new regulations explicitly state that no 'deemed licensed' arrangement will be provided for existing service providers.

This means that regardless of whether you currently have users or have been operating for years, if you have not completed formal application when the regulation takes effect, you must cease such activities immediately.

This stands in sharp contrast to certain markets' 'grandfathering' approach. Hong Kong has chosen a stricter but fairer path: all participants start on equal footing, applying under the same set of standards.

For institutions, this means they can no longer wait for 'policy clarity' before taking action.

III. No 'transition period红利', only 'early preparation advantage'

Another controversial point is that client assets must be held by an SFC-recognized custodian.

Some practitioners worry this may limit operational flexibility, especially for teams accustomed to self-custody or multi-signature solutions. But viewed from another angle, this requirement directly addresses the biggest concern of institutional investors — asset security.

One of the core obstacles preventing pension funds, sovereign funds, and large asset management firms from entering the virtual asset space on a large scale has been the lack of custodial solutions meeting regulatory standards.

Hong Kong's mandatory use of compliant custodians for licensed platforms sends a clear signal to global capital: client assets are strictly segregated from platform-owned assets, with independent audits, regulatory oversight, and accountability mechanisms in place.

This institutional arrangement is more reassuring to traditional capital than technological 'decentralization.'

Hong Kong's regulatory upgrade aligns with this trend. It does not reject innovation, but rather embeds innovation within a structured framework. For practitioners, the real opportunity lies not in loopholes or gray areas, but in who can first turn compliance into a service advantage — such as demonstrating a complete custody chain, clear suitability assessment processes, and verifiable transaction records. These details will become the core criteria for institutions when choosing partners in the future.

Compliance is not the end, but the starting point for participating in the next round of competition. — Xiao Sa