The recent surge in gold prices in January 2026 is hard to summarize with old phrases like 'another major bull market.' On January 13, London spot gold reached approximately $4,636 per ounce, setting a new historical high. This isn't due to a sudden boom in a mining stock, nor a short-term bubble caused by a hot ETF—it's more like a global monetary system health check-up: fiat currencies are systematically losing value, while gold is being forced back to its original, never-escaped role as the ultimate currency.

4,500 USD is more of a coordinate than a target price. It reflects a prolonged trajectory of fiat currency depreciation, and represents a concentrated pricing of a series of changes, including sovereign debt, the weaponization of sanctions, realignment of reserve assets, and the rise of on-chain finance. Gold hasn't become a 'higher-grade asset'; rather, the entire credit-based monetary system is losing credibility.

This article does not intend to provide a "future target price" or discuss short-term trading techniques. Instead, it offers a different perspective: in a world where gold has once again been used as currency, where do investors, institutions, and sovereign nations stand, and what kind of restructuring is underway?

$4,500 is not a "high point," but rather a benchmark for currency devaluation.

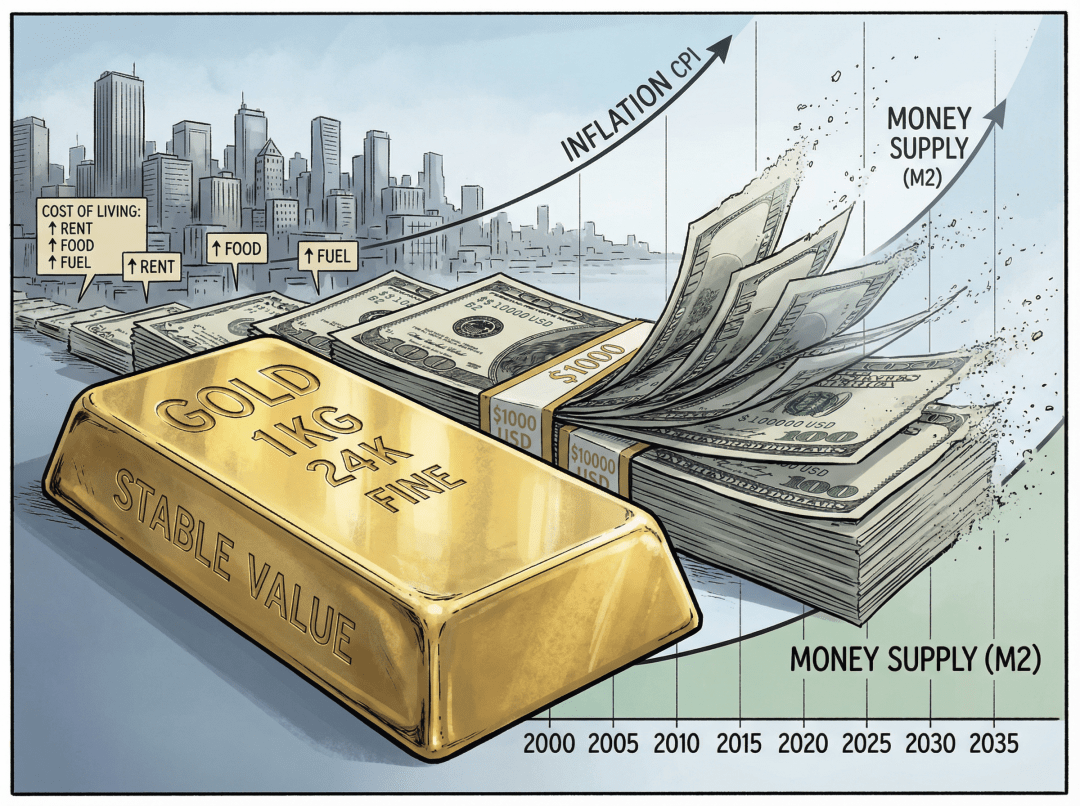

For decades, gold has been portrayed as an "inflation hedge," a "safe-haven asset," and an "inverse interest rate asset." While these labels still hold true, they are no longer sufficient. Since Nixon announced the decoupling of the dollar from gold in 1971, the dollar's purchasing power against gold has evaporated by nearly 98%. The so-called "new high of $4,500" is more like a belated accounting for the credit expansion of the past 50 years.

A simple comparison between global money supply, the rate of expansion of central bank balance sheets, and gold reserves reveals another, even more glaring fact. If gold is used to cover global monetary base (similar to M0), some institutions estimate the implied gold price to be between $40,000 and $50,000 per ounce. If we try to cover a broader monetary scope (closer to M2), the corresponding theoretical gold price jumps to hundreds of thousands or even higher.

A major asset management firm estimates that if gold were fully backed by the current global monetary base, the implied gold price would be between $30,000 and $40,000 per ounce. If a broader monetary scope were to be covered, the figure would skyrocket. In comparison, $4,500 seems more like a midway point in the "early stages of repricing," rather than the end. Simply put, with fiat currency expansion reaching its current scale, the price of gold reflects more the cost of the "fiat currency insurance premium" than the intrinsic value of gold itself.

From a pricing driver perspective, the traditional "real interest rate + exchange rate" framework is seeing its weight diminished by several factors. Persistently high fiscal deficits and debt rollover make it difficult to restore confidence in sovereign credit, no matter how high the interest rates are. Central banks' continued net gold purchases are transforming gold from a "small allocation in an investment portfolio" into a fundamental anchor on the balance sheet. Geopolitical conflicts and sanctions are turning "reserves held by others" into a privilege that can be frozen, naturally boosting the value of gold, an asset independent of the credit of its counterparties.

The old monetary pricing model has become ineffective, but the new model has not yet been fully established, and prices are testing this ambiguous boundary.

The chain of transmission through which fiat currency loses its status as a "safe asset"

To understand gold's return to its monetary function, we cannot focus solely on the price of gold itself; we must also examine the path of fiat currency's decline. For decades, US Treasury bonds have been marketed as the anchor of the "global risk-free interest rate"—holding US Treasury bonds was equivalent to owning the safest asset. However, as the debt-to-GDP ratio crossed one psychological threshold after another (the US federal debt/GDP ratio has stabilized above 120%) and new fiscal bills continued to increase deficits, this argument began to crumble.

Fiat currency typically loses its "safe asset" status through three steps:

The first step is that monetary policy has been hijacked by fiscal policy. Interest rate decisions are no longer aimed at controlling inflation, but at maintaining the sustainability of massive debt. The so-called real yield is largely eaten up by inflation and financial repression. Holders of sovereign debt are beginning to question whether they are receiving "interest" or a debt certificate slowly eroded by inflation. Simply put, raising interest rates is increasingly becoming a way to "buy time" rather than "solve the problem."

The second step is the weaponization of assets. The freezing of part of Russia's foreign exchange reserves in 2022 was a watershed moment. More and more countries realized that reserve assets held by others could be "paused" overnight by their adversaries. At this point, a fundamental characteristic of gold was recalled: it is not anyone's liability, it does not rely on any settlement system, and keeping it in one's own vault means real control.

The third step is a shift towards physical assets. When the risks of default and devaluation of credit assets rise simultaneously, central banks and sovereign wealth funds must find another anchor. Gold naturally meets several conditions: global consensus, cross-regime, long historical cycle, and no need for a counterparty. Thus, the old logic of "allocating a small portion to gold to diversify risk" has gradually transformed into the new logic of "reconstructing the entire balance sheet with gold."

As this transmission chain lengthens, an interesting phenomenon emerges. When the safety of sovereign debt is questioned, no matter how interest rates are adjusted, the downward pressure on gold decreases. In some stages, even "high interest rates + high gold prices" can occur simultaneously—because interest rates are interpreted as a signal that the debt system is on the verge of spiraling out of control, rather than a reliable return opportunity.

Weak fiat currency, Bitcoin, strong gold anchor: the prototype of a multi-tiered monetary system

While many are still debating whether Bitcoin will replace gold, the changing order in the real world has already provided another answer:

It's not about replacement, but about division of labor.

In the world beyond $4,500, a three-tiered structure is taking shape.

At the very bottom is the strong gold anchor, a final settlement tool that transcends sovereign and systemic boundaries. Central bank physical gold reserves are no longer simply "adding another asset class," but are gradually climbing in weight relative to US and European Treasury bonds. The repatriation of physical gold to domestic vaults has also transformed from a symbolic operation into a substantial hedge against the risks of overseas custody. The fact that European countries such as Germany, the Netherlands, and Hungary have been repatriating their gold reserves held at the Federal Reserve Bank of New York and the Bank of England since 2022 is the most direct signal of this.

The middle layer consists of digital hard assets such as Bitcoin. It addresses the shortcomings of gold in terms of "cross-border, instant, and small-value" transactions. Bitcoin has gradually moved from being a fringe speculative asset to being included in reserve discussions by some countries and institutions, playing the role of a "quasi-reserve that can be quickly transferred across borders" in scenarios with strict capital controls and significant sanctions. El Salvador's recognition of Bitcoin as legal tender and the United States' consideration of establishing a national Bitcoin reserve all point to one thing: digital hard assets are being incorporated into sovereign balance sheets.

At the top are national fiat currencies. While fiat currencies remain irreplaceable in local income settlements, tax payments, and wage distributions, their function as a store of value is weakening. They are more like a unit of account mandated by the state than the ultimate destination of wealth. True reserves are slowly sinking into gold and certain digital assets.

These three layers combined form a hybrid monetary system of "weak fiat currency + Bitcoin + strong gold anchor". Fiat currency is more of a surface interface, gold is the underlying capital support, and Bitcoin is a digital conduit for global liquidity.

Central Banks' "Action Voting": Rewriting the Monetary Order with Balance Sheets

Judging solely from media pronouncements, terms like "de-dollarization" and "increasing gold reserves" have been used for years and seem somewhat tiresome. However, the actual actions of central banks demonstrate that this shift is substantial: since 2022, official gold purchases have exceeded 1,000 tons for three consecutive years, and data from the World Gold Council has broken records almost every year.

The fact that official gold purchases have exceeded 1,000 tons for several consecutive years speaks volumes. The higher the price, the more rigid the purchases, indicating that this is not a short-term game but a structural reallocation. The proportion of gold holdings in the balance sheets of many central banks has caught up with or even surpassed that of US Treasury bonds. More importantly, some countries are beginning to pay more attention to "where their gold bars are"—the return of gold from overseas vaults to their own countries is a direct response to the risks of financial sanctions.

The changes in central bank asset allocation can be broadly summarized into three lines. First, a shift from market timing to structural accumulation: the focus is no longer on whether to buy at 3,800 or 4,200, but rather on raising the gold ratio to a new normal over the next few years. Second, a shift from paper debt to hard assets: while the term premium of US Treasury bonds has increased, their credit attractiveness has declined, and gold, some commodities, and strategic resource equities are gradually being seen as the "physical foundation of monetary sovereignty." Third, a shift from "indiscriminate foreign exchange reserves" to "foreign exchange reserves filtered for hostile risks": assets that could potentially become tools of sanctions in the future will be downgraded.

Behind this lies a quiet but profound reshuffling of power. As the main component of official reserves shifts from "foreign debt" to "real assets under one's own control," traditional monetary hegemony is gradually losing its grip. The decline in the US dollar's share of global foreign exchange reserves from around 65% in 2000 to approximately 40% today is the most direct reflection of this reshuffling.

High price does not equal high supply: the physical basis of the gold monetization premium

Many people, upon seeing $4,500, will instinctively think of one question: "At such a high price, won't miners ramp up production?" The reality is quite the opposite. The characteristics of the gold supply side are: long supply chain, high rigidity, and extremely cautious capital decisions.

From the discovery of a deposit to the actual start of gold production, it often takes 6–10 years. Exploration, licensing, infrastructure construction, and environmental reviews—each step can slow things down. The World Gold Council's analysis repeatedly emphasizes that global capital expenditure on gold exploration has been relatively low over the past decade, and the current high prices are, to some extent, a make-up for that period of "insufficient investment."

Even in a high-price environment, mining companies may not be willing to aggressively expand production. The overall cost curve for mining is shifting upwards, with energy, environmental, and labor requirements pushing up AISC (Total Sustainability Costs, including all operating costs such as mining, processing, and management). Easily accessible high-grade ore is becoming increasingly scarce, and new projects are often buried in deeper or more remote locations. Boards are more willing to reward shareholders with dividends and share buybacks rather than betting on a decade-long cycle. In 2025, Lundin Gold's AISC guidance under the assumption of a $4,000 gold price already reaches $1,110-$1,170, highlighting the significant cost pressures.

The rigidity of the supply side provides a solid physical foundation for the "gold monetization premium." Prices can fluctuate wildly in the short term due to financial leverage, but it is difficult for the actual mineral supply to expand rapidly enough to dilute this premium.

Meanwhile, the demand structure is quietly shifting. The market, traditionally dominated by gold jewelry and consumer demand, is being squeezed out by official and investment demand. The volume of gold jewelry has been declining for several quarters, with high prices keeping many ordinary consumers out. Official gold bars and small-denomination gold coins, on the other hand, continue to see increased supply, with retail investors willing to buy a few grams less to secure a substantial piece of future "insurance." Industrial demand is growing steadily, driven by industries such as AI and electronics, but its share of total value remains limited. The secondary recycling market has not seen the anticipated "frenzied selling," with many holders choosing to remain on the sidelines due to price support and expectations of further increases.

Gold is increasingly resembling less of a consumer good and more of a monetary instrument that only a few individuals, institutions, and sovereign capital can afford to play with.

Gold as a “sanctions firewall”: Energy, shipping routes, and the precursors of a regional gold standard

In recent years of frequent geopolitical conflicts, another ancient function of gold has been reactivated: a firewall against sanctions. When a country suddenly discovers that its foreign exchange reserves held in the overseas banking system can be frozen with a single executive order, the allure of gold is almost instinctive—it has no SWIFT account, does not require dollar clearing, and does not carry a "liability" label on anyone's balance sheet.

Several key trends are driving gold back into the international settlement tier. The partial physicalization of energy trade is leading some oil-producing countries to experiment with using gold to settle some oil exports, or to bypass the dollar as an intermediary through bilateral "gold-for-oil" arrangements. Russia and Iran implemented gold pricing and settlement for some oil trade in 2025, and African countries like Ghana have also bypassed the rigid demand for dollar reserves through "gold-for-oil" programs. In regional currency experiments, gold is being embedded in currency baskets. For example, in the BRICS-related mechanisms, the "Unit" pilot project, launched in October 2025, has a gold content set at 40%, aiming to add a globally recognized value anchor to this new currency design. Shipping lane conflicts and the threat of sanctions have led to increased discussions about "gold as the final settlement method" in more bilateral negotiations, even if the scale is currently small, the direction has been determined.

Even more subtle are the changes in gold production and the distribution of reserves.

When more than half of the new production and nearly half of the underground reserves are concentrated within a few political alliances or cooperation frameworks, this "control over the physical supply of gold" itself becomes a financial weapon. It can be used to build the underlying support for non-dollar settlement networks, or in extreme cases, as a countermeasure against the freezing of foreign exchange reserves.

The relationship between interest rates and gold is being rewritten.

Traditional textbooks present a clear inverse relationship between gold prices and real interest rates: rising interest rates increase the opportunity cost of holding gold, thus causing gold prices to fall; conversely, falling interest rates decrease the price of gold. However, in recent years, the market has repeatedly witnessed a discrepancy: rising real interest rates have led to gold prices rising instead of falling; and at the end of interest rate hike cycles, gold prices have accelerated their upward trend.

The reason is actually not complicated. When the total debt has become so large that it can no longer be absorbed naturally through growth, every interest rate hike may be interpreted by the market as a prelude to "inevitable inflation or default at some point in the future." In other words, if high interest rates fail to increase confidence in sovereign debt, they will only reinforce the expectation that the government will ultimately have to devalue its currency to reduce debt.

In this environment, the role of interest rates in gold pricing is overshadowed by factors such as credit premiums, geopolitical conflicts, and unsustainable fiscal policies.

In the short term, there will certainly be passive moments of "liquidity tightening → gold sell-off," such as margin tightening, leveraged runs, and large-scale ETF redemptions. However, these are more like noise in a structural upward process than a fundamental reversal.

Another easily overlooked change is the volatility of gold itself.

As financialization deepens and on-chain gold and derivatives become more abundant, gold price fluctuations are no longer slow and unidirectional, but rather highly elastic and "step-like." This changes the requirement for investors from "just hold on" to "maintaining positions during periods of high volatility and avoiding being shaken out by short-term panic."

On-chain gold: Connecting "dormant gold bars" to a 24/7 settlement network

A fatal flaw of traditional gold is its lack of liquidity and programmability. Physical gold is suitable for long-term storage but not for frequent transfers and splits. ETFs and paper gold, in some cases, revert to the old approach of "requiring trust in intermediaries."

Tokenized gold (PAXG, XAUT, etc.) emerged precisely from this gap. Their ambition is not to replace physical gold, but to add a shell of "real-time settlement + financial programming" to gold.

This new framework has changed several things. While the physical gold remains in traditional vaults, ownership can be transferred on-chain in seconds. The smallest unit can be broken down into very small amounts, starting with a tiny handful of gold equivalent to just a few dollars. Gold has transformed from being "only suitable for large-scale reserves" to being used for some retail payments and wealth management. Through DeFi protocols, tokenized gold can be used for staking, lending, and market making, giving gold a yield curve instead of simply sitting in a vault. By the end of 2025, the market capitalization of tokenized gold had reached nearly $4 billion, a threefold increase from 2024.

What's even more interesting is that on-chain gold often forms a "dual-anchor combination" with USD stablecoins. Gold serves as the underlying collateral and final settlement, while stablecoins handle pricing and payments in daily transactions. The entire system operates on a settlement network that is parallel to or even independent of the traditional banking system.

Of course, this path is not without risks: compliance, centralized custody, and issuance transparency—any failure in any of these areas can backfire and damage the entire sector. However, judging from the trend, gold is no longer just a "dormant asset in a safe," but has been integrated into a global real-time financial network.

Gold and Bitcoin: From the debate over "which is more like currency" to a "dual-currency combination"

Gold has a 6,000-year history as currency, while Bitcoin is only a teenager. But in the past few years, their relationship has changed from "opponents" to "partners".

In extreme situations, holding gold and holding Bitcoin represent two completely different defenses for capital. Gold is physically independent, not reliant on a network, making it suitable as an ultimate reserve. Bitcoin's cross-border transfers are virtually frictionless, making it suitable as an emergency liquidity outlet in capital-controlled environments. Gold is best stored in vaults for large-scale liquidations and long-term hedging. Bitcoin is well-suited for frequent movement at the network layer, connecting to exchanges, DeFi, and cross-border payments.

For some sovereign states, these two can even be structured as an internal cycle. Gold is used to settle accounts with some trading partners, reinforcing "physical credit." Bitcoin is used to access a broader ecosystem of digital assets and stablecoins, obtaining a liquidity pool not entirely controlled by the Western financial system. In some sanctioned regions, Bitcoin has become a trade settlement tool directly linked to gold.

For large institutional investors, the "gold + Bitcoin" portfolio is evolving from a speculative combination into a new module within their asset allocation framework. Gold offers long-term protection against inflation and institutional risks, while Bitcoin provides highly resilient liquidity hedging and potential returns. Together, they form a comprehensive defense against fiat currency devaluation, financial repression, and sanctions.

The next few years: not a "bull market or a bear market," but the speed of repricing under different paths.

Discussing "how much higher can it go" now is pointless. The more practical question is: how quickly will gold be repriced under different macroeconomic trends, and will we have time to react gradually?

We can use three scenarios to roughly think about this—not precise predictions, but risk maps.

If the world maintains a state of "slow bleeding," with inflation not so high as to get out of control, but always hovering above the target; and fiscal deficits not exploding, but with no political space to reduce them, then gold is more like slowly climbing a staircase. Central bank gold purchases are stable, demand structure continues to be monetized, with occasional pullbacks, but it's difficult for it to fall in the long run.

If a sovereign credit or financial system crisis erupts, and the debt problems of a major economy are suddenly exposed, leading to a chain reaction of bank runs, escalating sanctions, and tightening capital controls, gold and Bitcoin may experience a non-linear price surge, with prices resembling a curve suddenly straightened out, completing the concentrated pricing of years of accumulated risks in a short period.

If we witness a "productivity miracle," where technologies like AI and large-scale automation not only boost valuations but genuinely reduce societal operating costs, improve fiscal conditions, alleviate debt pressures, and bring inflation back to a manageable range, then gold is likely to slowly decline from its current highs. Some investment demand may recede, but the rigidity on the supply side will provide new support at lower prices. The role of a long-term monetary anchor will remain, only the premiums will temporarily become cheaper.

In any scenario, several risks need to be considered in the long term. Aggressive fiscal austerity coupled with violent interest rate hikes, if politically unexpectedly implemented, would forcefully compress the short-term premium for gold. Forced sales of physical reserves by some countries during their own debt crises could trigger a short-term liquidity crunch. A sudden tightening of financial regulations, imposing severe restrictions on the cross-border flow of on-chain gold, stablecoins, and Bitcoin, would temporarily cut off gold's access to real-time settlement layers. In times of extreme liquidity tightening, both gold and Bitcoin could be treated as "liquid assets" and sold off together, resulting in a short-term positively correlated decline—something the market already experienced in 2020.

When gold has become a form of currency, discussing its "price" becomes less meaningful.

Gold's breakthrough of $4,500 was a high-profile price event, but also a low-key reshuffling of the monetary order. As more and more central banks, institutions, and individuals cease to view gold as a "commodity" and instead regard it as a "borderless ultimate collateral," our focus should shift away from questions like "how much higher can it go?" and "where is the top?"

A more practical question is: in an environment of continuous fiat currency depreciation, how can we rationally allocate physical gold, on-chain gold, and digital hard assets to position our balance sheet as a "beneficiary" rather than a "dilutive" side of the repricing process? In this new phase of significantly increased volatility, how can we view short-term pullbacks, regulatory disturbances, and leveraged runs as "noise" within structural trends, rather than reasons to hastily exit the market? As a multi-tiered monetary system gradually takes shape, how can we understand the functional division between gold, Bitcoin, and fiat currency, moving beyond a single-asset perspective to comprehend the fragmented global monetary world?

When you acknowledge that gold has once again taken center stage as currency, the "price" itself becomes secondary. What truly matters is how much real purchasing power your gold holdings—whether in vaults, on-chain, or a digital representation—will retain for you, and how many new avenues will they open for you in the next round of monetary order readjustment.