Just found out Boros_fi has launched BNB, initially supporting two markets: Binance and Hyperliquid.

If you've been doing $BNB lending, hedging, or earning funding rates, make sure to keep an eye on this—another great place for your investments!

This update has several key details—

You can directly use BNB as collateral

No need to prepare ETH/Arbitrum for gas

You can open positions by directly transferring BNB from Binance

I've actually used it, and I can definitely feel it—Boros is definitely aligning with the usage habits of CEX users. If you're familiar with Binance's perpetual contracts, you can jump right in with Boros without learning any additional processes.

This step will directly affect the types of users Boros can reach later, not just DeFi natives, but those large capital pools already rolling funding fees frequently in CEX!

The most notable point is the launch of the special asset BNB. To put it simply, a conclusion—

BNB should currently be the market on Boros that is closest to 'rules giving away money'.

Why do I say this?

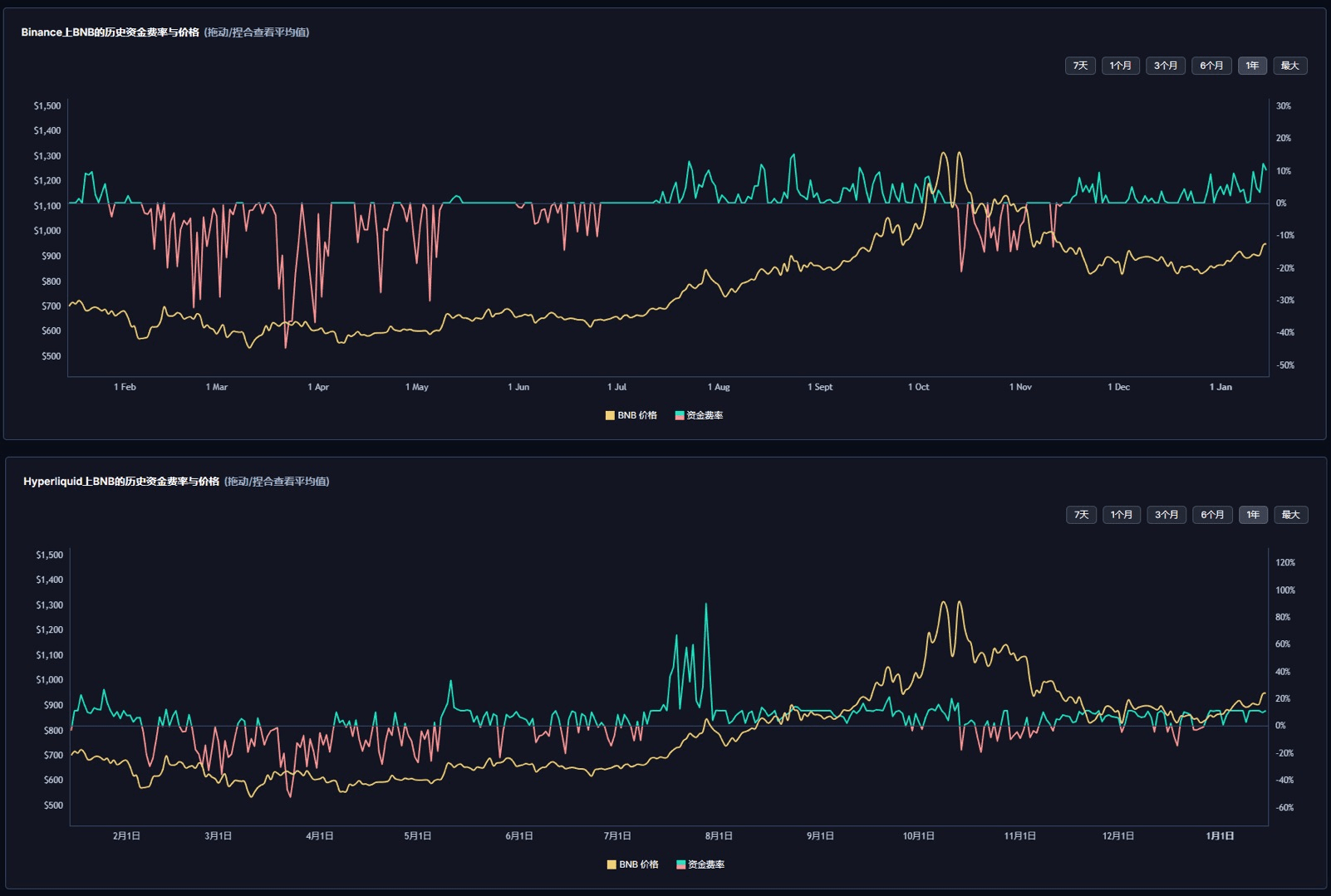

According to @0xanonnnn's observation, different exchanges have different pricing mechanisms for BNB funding rates;

At Binance, the benchmark funding fee rate for BNB has long-term fluctuated around 0%;

At Hyperliquid, using a standard model, the average fee rate for BNB will long-term revert to around 10%.

Simply translate it—

The funding cost expectations for BNB, being the same asset, inherently vary long-term across different exchanges.

In one place, BNB contracts have almost no rental fees long-term;

In another place, a considerable capital cost must be incurred long-term.

Damn, what does this mean in the world of arbitrage, those who understand, understand!

However, this type of operation is closer to cross-market, cross-pricing structure arbitrage, suitable for those who are familiar with margin and position management.

If viewed from a practical operational level, the BNB market on Boros is the easiest for ordinary newcomers to understand, actually revolving around 'hedging'—

For example, if you have BNB spot, while shorting BNB contracts on BN or HL to hedge price risk and also earn funding fees.

In this structure, price is not the core variable; what truly impacts the outcome is whether the funding rate remains positive.

Once the rate turns negative, the originally valid arbitrage logic will be eroded, potentially resulting in direct losses.

What Boros offers is a very specific tool: when you see a clear Implied APR in the corresponding market, you can choose to short YU on Boros, locking the funding fee level during this period near the current quote.

As a result, the funding fee expenditure in your hedging structure will not fluctuate chaotically, but will depend more on the interest rate spread at the time of position opening.

In the past few days' BNB new offerings, if you know how to use Boros, you can effectively control your hedging costs.

It is precisely because of this that I believe this update is crucial for Boros itself and could attract a large number of new CEX users.

I recalled a report I came across a couple of days ago, stating that by 2026, Boros's scale has achieved rapid growth—open interest is approximately $190 million;

In the entire $160–170B perp market, it accounts for about 0.1%.

Looking at it from another angle, Boros still has a large growth space:

If Boros is only considered a new toy by a few DeFi users, then the space is indeed limited;

But once it starts being used as a daily tool by users engaging in CEX hedging and funding fee arbitrage, the growth logic will be completely different.

perp market OI ~$160–170B, Boros only needs to achieve a 2% penetration rate, under the current fee structure, to potentially bring more than 15% incremental fees to @Pendle !

Therefore, the strategic significance of Boros is obvious, representing a completely independent growth curve for Pendle.