Every time the market fluctuates, I always hear 'It has fallen again, this time it will go to 60,000' and 'It has risen again, this time it will break new highs.' When it rises, the bulls come; when it falls, the bears come. In too many stories of people shouting that the wolf is coming, we have all, without exception, successfully chased after gains and cut losses. The conclusion is that blindly fidgeting is worse than doing nothing at all.

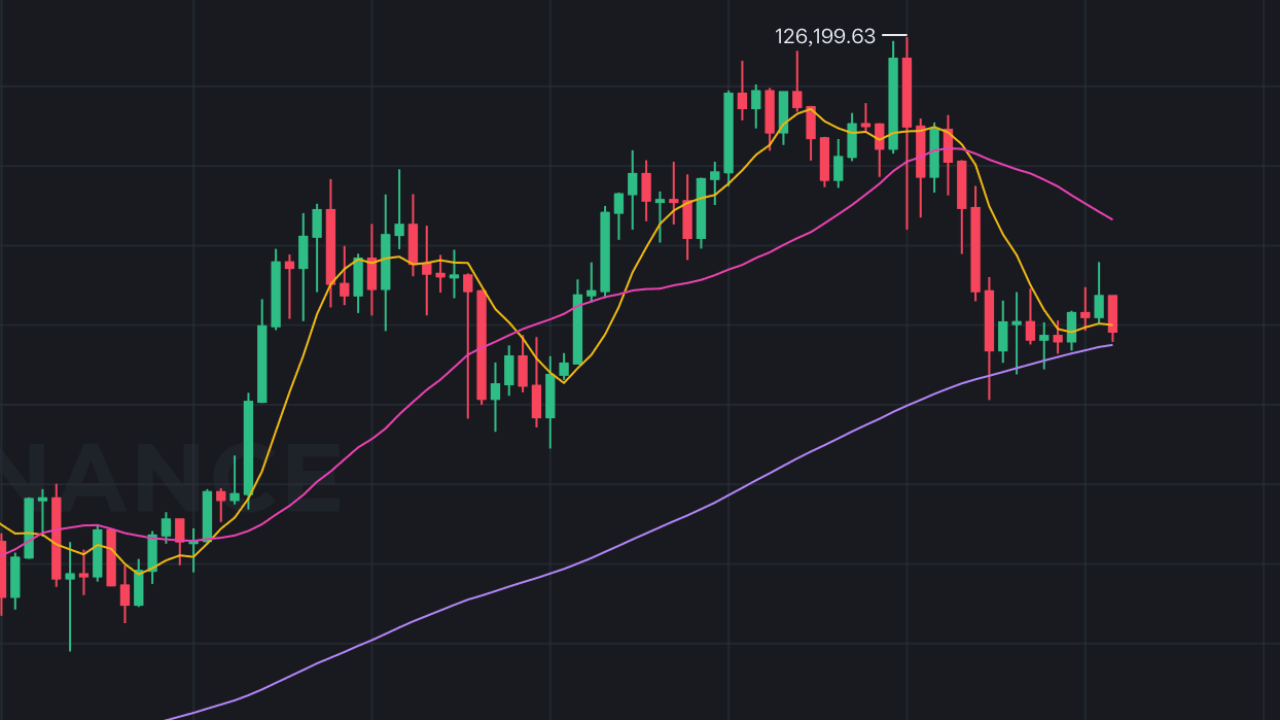

Since October of last year, I believe many people, like me, are in a vague state of anxiety, as if we have missed one of the few historic opportunities in the Crypto industry during our lives. In just over three short months, we have witnessed the new high of BTC, the rise of Chinese Memes, and also witnessed the 'spectacle' of over 19.1 billion USD and 1.62 million people liquidated in a single day.

I have always believed in decentralized blockchain, love cryptocurrency, but why does my wallet keep paying for my beliefs? I saw an interesting sharing from an analyst: 'As long as you don't invest in Crypto, you can earn in other markets. The disappointment is spreading among crypto investors, and when asked about making money in other markets without investing in Crypto, they even share the 'secret' of 'ABC' – Anything But Crypto, as long as you don't invest in Crypto, you can earn in other markets.'

It’s worth thinking, just a few days ago, we were still immersed in the joy of approaching 100,000, but now it has broken 90,000. The emotional switch is faster than the K-line. Is Crypto really unbearable? No, we need to give ourselves some motivation and recharge our beliefs. Perhaps in the current multidimensional complex, even somewhat torn macro environment, Crypto is the clearest asset target and guiding light.

Since 2025, precious metals, US stocks, A-shares and other markets have risen repeatedly, forming a sharp contrast with the silence in the crypto space. However, these increases do not entirely stem from macro and liquidity improvements, but are more driven by sovereign will and industrial policies against the backdrop of great power competition. The rise of these assets further absorbs the already limited liquidity (the rise of crypto relies on liquidity logic), weakening expectations for crypto price increases and exacerbating downward performance.

In the past two days, macro risks have resonated. The gold breakthrough at 4900 indicates clear inflows of risk-averse funds, while US stocks have collectively fallen, signaling synchronization of risk asset deleveraging. This indicates that global capital is doing one thing: reducing risk exposure and enhancing defensive attributes. In such an environment, the most clear asset target, BTC, still remains above $80,000. It may drop below $80,000, but undoubtedly, it is no longer the BTC that was once cherished only by faith. Today, it is included in the reserves of some sovereign nations, public institutions, and quasi-government entities; becoming a strategic asset on institutional and corporate balance sheets; entering traditional capital markets through various forms such as ETFs and structured products; with real, verifiable, and continuously evolving demand behind it. Its value is shifting from 'market dream rate' to 'market reality rate', migrating from narrative asset to institutional asset.

Therefore, regardless of how the outside world changes, recognize the essence, return to first principles, see the true stage of industry development, not be carried away by emotions, and not let external noise change one's most authentic judgment logic of asset value, and seek the value average of assets. I believe that as the Crypto industry matures, even if prices fluctuate dramatically under macro and emotional influences, in the medium to long term, it will continuously converge towards the value average after each fluctuation.

Thanks to this understanding, I suddenly feel like the fog has lifted, and I try to jump out of the pure trading perspective, curiously using the professional perspective of technology listed company valuation, combined with AI (AI really makes knowledge equitable) to systematically break down the valuation of ETH, BNB, and SOL three Layer1s, including: business model breakdown, core 'income/cash flow' equivalents, valuation methods and implicit multiples, judgment of current prices, market values, FDV's rationality, medium to long-term valuation range deduction, and the marginal impact mechanism of institutional and corporate strategic reserves on these assets. Because they are no longer 'pure tokens', but blockchain infrastructure companies with a complete business closed loop.

One, ETH (Ethereum) – similar to 'global decentralized cloud computing platform'

1. The essence of the business model

From the perspective of listed companies, Ethereum is a:

Global distributed computing and settlement infrastructure providers

Income sources = on-chain transaction fees + MEV + L2 settlement demand + security premium of the staking system

Equivalent analogy:

AWS / Google Cloud + settlement system + decentralized operating system

The uniqueness of ETH lies in:

It is one of the few public chains with sustainable 'native cash flow'

And form a closed loop of 'income → buyback → burn' through EIP-1559

This corresponds in traditional companies to:

High gross profit SaaS + continuous buyback + supply-side tightening

2. 'Income equivalents' and cash flow capabilities

The core 'operational indicators' of ETH:

Annual on-chain transaction fee income (bull market peak): $15B–$25B

Normal cycle: $6B–$10B

Of which 30–70% is directly burned (equivalent to net buyback)

This means:

In the bull market cycle, the implicit free cash flow rate of ETH is very high

And the supply is deflationary or quasi-deflationary

3. The 'multiplicative disassembly' of current valuation

Using current data (approximate):

Market value: ~$360B

Normalized annual income capability: ~$8B–$10B

Implicit P/S = 36–45 times

In traditional technology:

Mature cloud service company: 8–15x P/S

High growth infrastructure platform: 20–30x P/S

Infrastructure with network effects + high moats: acceptable 30–40x

Conclusion:

The current valuation of ETH is not low, but under the premise of the scarcity of 'the world's only decentralized settlement layer', it is still in the 'explainable range'.

4. Qualitative judgment of FDV and supply structure

The key advantage of ETH:

No fixed maximum supply

But through the burn mechanism, the long-term actual supply approaches 'soft deflation'

This is equivalent to:

A company that can dynamically reduce its share capital scale

This is extremely rare in traditional markets and is one of the valuation moats of ETH.

5. Medium-term reasonable valuation range (based on technology valuation method)

Using a cycle of 12–18 months, adopting:

Normalized annual income: $8B – $12B

Giving a 20–30x infrastructure multiple

Achieve medium-term reasonable market value:

$200B – $360B (central range)

Extreme bull market scenario: $450B – $550B

Corresponding price range (based on current supply):

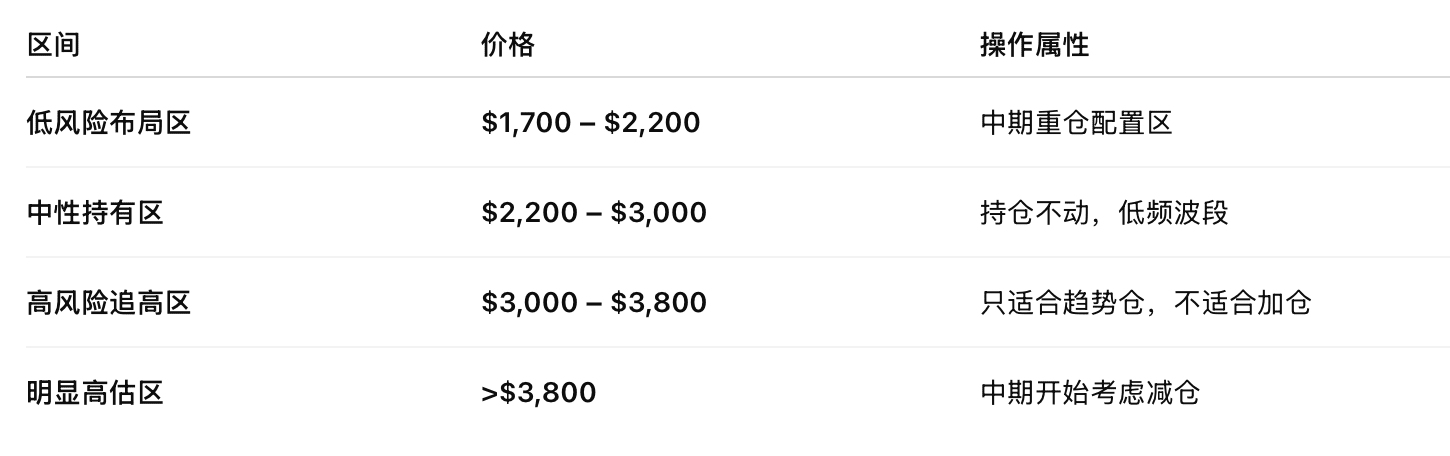

Rational central price:

$2,000 – $3,000

Bull market premium area:

$3,000 – $4,200

Once any of the following occurs, the valuation logic of ETH needs to be revised downwards:

On-chain income has significantly declined for 2–3 consecutive quarters

L2 completely engulfs mainnet settlement value, mainnet fee structure fails

The staking system is strongly restricted by regulation (affecting security premium)

As long as these three points do not hold:

ETH is the asset with the lowest medium-term risk.

6. The impact of strategic reserves of institutions and listed companies on ETH

For ETH, the meaning of listed company holdings is:

Strengthen its positioning of 'digital national debt / digital reserve assets'

Enhance its institutional allocatable premium

But the core driver for valuation increase remains:

On-chain income and burn scale, rather than simply holding behavior

Conclusion:

For ETH, institutional and listed company strategic reserves are the stabilizers of valuation, not the main drivers.

Two, BNB – similar to 'platform super company equity + endogenous tokens in the ecology'

1. The essence of the business model

BNB is essentially not a 'pure infrastructure chain', but:

Binance, this 'super financial platform', is an equity-mapped asset + endogenous tokens in the ecology

Its value is highly dependent on:

Binance exchange profits

Binance ecological traffic

Buyback and burn mechanism (quarterly burn)

Equivalent traditional company model:

Similar to:

Alibaba equity + internal points system

Combining the attributes of 'platform stock + functional token'

2. 'Income equivalents' and buyback mechanism

The source of BNB's value is very clear:

Binance's annual profit: historical peak $10B–$20B

Buy back and burn BNB at a fixed ratio

Equivalent to:

A high-profit platform company + forced buyback plan

This is a highly popular structure in the traditional market.

3. The 'implicit equity logic' of current valuation

Current data:

Market value: ~$120B

Assuming Binance's annual net profit: $8B–$12B

Implicit valuation multiple:

P/E ≈ 10–15 times

This is a very low level of multiples.

But the problem is:

BNB is not legally considered equity

Investors bear the discount of regulatory uncertainty

Therefore, the market's valuation logic for BNB is:

High profitability × high regulatory risk discount

4. FDV and supply structure judgment

The key advantage of BNB:

Fixed maximum supply of 200 million

Continuous destruction, ultimately reduced to around 100 million

Highly controllable supply side

This is equivalent to:

A company that continuously repurchases and reduces its share capital

This is extremely favorable for long-term valuation.

5. Medium-term reasonable valuation range (similar to platform stocks)

Assuming 12–24 months:

Binance's annual net profit: $8B – $12B

Giving a 10–15x risk discount multiple

Achieve a reasonable 'equity equivalent market value':

$80B – $150B (central range)

Extreme optimistic scenario: $180B – $220B

Corresponding price range:

Rational central price:

$650 – $1,000

Bull market premium area:

$1,000 – $1,300

The risk of BNB is not technical, but institutional risk:

Binance forced to split / severe fines / core business restrictions

Buyback and burn mechanism interrupted or weakened

Exchange profits showing structural decline

As long as:

Buyback continues

Exchange cash flow stable

Then:

BNB is a typical 'low valuation + strong bottom support' mid-term asset.

6. The impact of strategic reserves of listed companies on BNB

For BNB:

The marginal significance of strategic reserves is weak.

Because its core value is:

Binance's profitability, rather than 'public chain scarcity'

Conclusion:

The valuation uplift from listed company holdings for BNB is significantly weaker than that for ETH / SOL, more like holding a 'shadow equity' of a non-listed company.

Three, SOL (Solana) – similar to 'high-growth infrastructure startups'

1. The essence of the business model

The essence of Solana is:

Early-stage companies of high-performance, low-cost blockchain operating systems

Its core goal is:

Extreme TPS

Extremely low transaction costs

Support high-frequency applications (payments, social, gaming)

Equivalent traditional company stage:

Similar to:

Early AWS

Early Android

Infrastructure companies with high growth but not yet formed stable profit models

2. Current 'income equivalents' are severely low

The current issue with Solana is:

Transaction volume is extremely high

But the per-transaction fee is extremely low

Annual network income is only in the hundreds of millions range

This means:

The current valuation of SOL is almost entirely based on future growth expectations, rather than current cash flow.

This corresponds in traditional markets to:

Typical valuation method for 'high growth loss-making technology companies':

Pricing based on user numbers, activity levels, and ecological expansion speed.

3. The implicit assumptions of current valuation

Currently:

Market value: ~$70B

Annual income capability: <$1B

Implicit P/S:

70x – 100x

This is a very high multiple.

The market's implicit assumption is:

Solana will grow into:

The second largest or even the largest high-frequency settlement network

And significantly improve fee structure, MEV, and ecological income

4. FDV and supply risks

The core risk point of Solana lies in:

There is still a large amount of token unlocking history

Inflation rate higher than ETH / BNB

Supply side puts long-term pressure on price formation

This corresponds in traditional companies to:

A growth company that continuously issues shares for financing

5. Medium-term reasonable valuation range (growth model)

Assuming 12–24 months:

Annual income increased to: $1.5B – $3B

Giving a 20–30x growth multiple

Reasonable market value range:

$40B – $90B (central range)

Extreme success scenario: $120B – $150B

Corresponding price range:

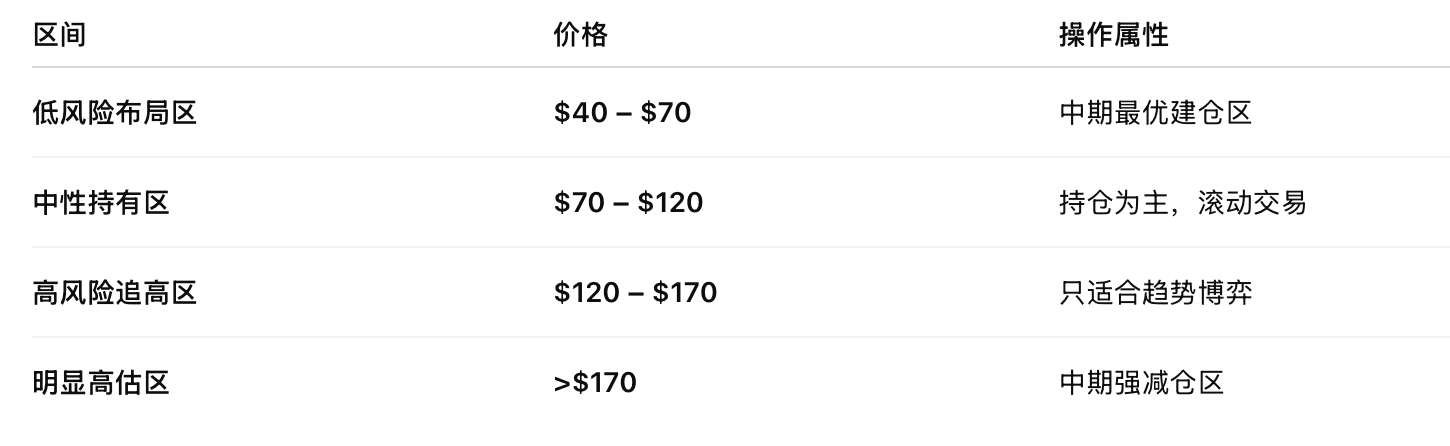

Rational central price:

$70 – $130

Bull market premium area:

$130 – $200

The medium-term risk of SOL mainly comes from three points:

Income has not improved for a long time (high activity, low monetization long-term unchanged)

Network stability has again encountered systemic incidents

Large-scale unlocking periods suppress prices

If:

High transaction volume

But income structure does not improve

So:

The valuation of SOL will rapidly collapse from 'growth premium' to 'pure speculative premium'.

6. The impact of strategic reserves of listed companies on SOL

For SOL, this is the biggest beneficiary among the three:

Reason:

The current valuation of SOL is highly dependent on 'future stories'

Listed company holdings = strong endorsement of its 'future mainstream infrastructure'

Will significantly elevate its growth premium

Conclusion:

For SOL, the strategic reserves of listed companies are amplifiers of valuation, with effects far exceeding those of ETH and BNB.

The above content is for reference only, no need to argue.