As the green stock price on Nasdaq covers the stench of dirty money, and the shiny exterior of the AI engine becomes a tool for money laundering — the astonishing scam of $APP, spanning Southeast Asia's black market and Wall Street capital, is being unraveled layer by layer!

On the Nasdaq screen, the green stock price of $APP (AppLovin) once attracted countless investors, touted as 'the AI-driven future of mobile internet.' But a 36-page forensic investigation report tore apart its grim facade — it is not a tech unicorn but a 'money laundering machine' for Southeast Asian criminal groups.

On January 21, 2026, in the face of money laundering allegations from CapitalWatch, AppLovin urgently responded with Yahoo Finance, dismissing the accusations as 'false and economically unfeasible.' However, this pale defense not only failed to clear its suspicions but also exposed its compliance failures and securities fraud in the face of irrefutable evidence. More significantly, CapitalWatch has explicitly warned: three more solid reports are set to be released, and this storm surrounding $APP is just beginning.

I. Ironclad Evidence of Money Laundering: The "Perfect Gateway" for Southeast Asian Criminal Groups

AppLovin's response boiled down to two points: "inability to control shareholders" and "money laundering is not worthwhile." However, these two arguments crumbled in the face of a complete chain of evidence.

1. Core shareholder is a wanted criminal: a multi-billion dollar black market behind 28.1% of the shares.

AppLovin claims it has "no control over who buys the stock," attempting to portray Hao Tang, the core shareholder holding 28.1% of the shares, as an ordinary retail investor. However, SEC filings and in-depth investigations reveal that Tang, through three shell companies including Discovery Key Investments, has long been one of the company's actual controllers.

In mature capital markets, holding more than 5% of shares triggers the disclosure threshold, and exceeding 10% requires strict KYC (Know Your Customer) and AML (Anti-Money Laundering) obligations. The "ordinary retail investors" mentioned by AppLovin are actually fugitives wanted by law enforcement for major economic crimes. Their funds directly originated from $957 million in illegally raised funds transferred before the collapse of Tuandai.com, as well as proceeds from 10 years of illegal gambling and usury operations.

Even more alarming is that Tang Hao belongs to the same criminal organization as Chen Zhi, the founder of Prince Group, who was recently arrested and deported by the government. Chen Zhi, as the head of Asia's largest transnational criminal organization, is suspected of wire fraud, human trafficking, and forced labor. His 127,000 bitcoins (worth $15 billion) have been seized by the U.S. Department of Justice, setting a record for the world's largest asset seizure. The capital entanglement of these two wanted criminals has turned AppLovin's equity structure into a complete shield for illicit activities.

2. 30%-40% "laundering fee": The core of money laundering is never making money.

The argument that "money laundering through advertising is not worthwhile" exposes AppLovin's ignorance of underground finance. The essence of money laundering is never profit maximization, but rather giving illicit money a "legitimate identity"—criminal groups are usually willing to pay 30%-40% or even higher "laundering fees," and AppLovin's platform fees and advertising revenue sharing have become the perfect vehicle for this fee.

Prince Group had already established a closed-loop money laundering network through its subsidiary, Jin Bei Group: acting as an advertiser, it aggressively purchased user traffic through apps like WOWNOW; acting as a publisher, it sold traffic through a massive number of spam apps. Even after AppLovin took its cut, the remaining funds were successfully converted from illicit funds obtained through "pig butchering scams" and "online gambling" into legitimate settlement funds for a Nasdaq-listed company. The U.S. Treasury Department has confirmed that Jin Bei Group is linked to extortion, fraud, and murder, and in 2022 it defrauded 259 Americans of a total of $18 million.

3. Advertising + Games: A Natural "Digital Money Laundering Maze"

Why did criminal groups choose AppLovin? Its "ad monetization + game ecosystem" business model inherently possesses advantages for money laundering: the fragmented and cross-regional nature of advertising, combined with the flexibility of mobile games to "launch anytime, reskin, and buy users," creates a labyrinth of fund flows that is difficult to trace.

The three-step process of money laundering is clearly visible:

Step 1: Leaving the illicit funds abroad. Tang Hao's gang converted their illegal proceeds into USDT through underground banks and then transferred them to offshore shell companies in the Cayman Islands and other locations, taking advantage of the anonymity of crypto assets.

Step Two: Creating Revenue. The shell company, posing as an "advertiser," places ads on AppLovin to promote fake, reskinned games, converting illicit funds into the platform's "legitimate revenue."

Step 3: Capital Harvesting. Tang Hao built up his position at a low price before the IPO, and then cashed out and left after the fake transaction volume drove up the stock price, completing a double harvest of "money laundering + harvesting retail investors".

Ironically, AppLovin's claim of "strict KYC" has long been exposed by technical evidence: Cambodian local life app WOWNOW generates huge advertising expenditures that are disproportionate to its size, and its Array product was used by the Jinbei Group to "silently install" illegal gambling apps. These illegal apps, which are rejected even by Google Play, were able to enter users' phones through AppLovin's backdoor.

II. A Shocking Lie: The "Ghost Business" Personally Endorsed by the CEO

If money laundering charges can still be explained by the excuse of "lack of knowledge," then business fraud is blatant securities fraud.

1. A "non-existent" company where the CEO is the legal representative.

During the earnings call on May 7, 2025, AppLovin CEO Adam Foroughi stated unequivocally that "AppLovin does not operate in China." However, business registration information shows that "AppLovin (Beijing) Technology Development Co., Ltd.", for which he personally serves as the legal representative, has been in a "continuous existence" status since its establishment in 2018, with a registered capital of US$500,000 and an office address located in Parkview Green Fangcaodi, Beijing. In 2022, it also added a branch office in Hangzhou.

A subsidiary directly managed by its CEO and with physical offices in Beijing and Hangzhou was publicly denied its existence. This blatant cognitive dissonance suggests either extreme incompetence on the part of the management or deliberate deception of regulators and investors.

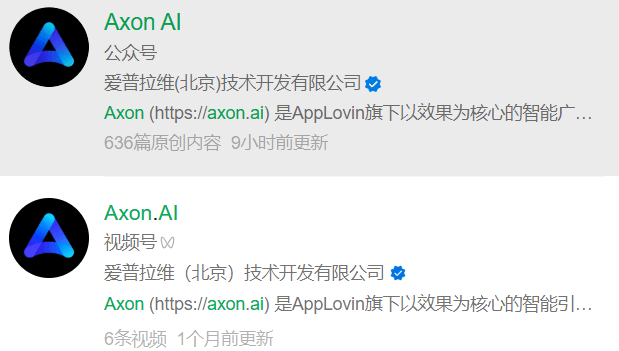

2. Core Engine Axon: The team is currently developing it.

AppLovin attempted to bluff its way out by claiming it was a "non-core business," but its recruitment information and employee updates completely exposed the deception. According to BOSS Zhipin, AppLovin's Beijing team officially established the Axon China R&D team in 2024. With fewer than 60 core members, the team focuses on top-tier global advertising products and e-commerce advertising, and also explores the application of large language models in the advertising field.

High-paying job postings on platforms like Maimai and Xiaohongshu explicitly state "Join the Beijing Axon team," and the WeChat official account "Axon AI" is certified to be Axon (Beijing) Co., Ltd. Employees' social media posts about office activities also bear the tag "Axon China Team." It's important to understand that Axon is the commercial heart of AppLovin, driving its AI recommendation engine, which is valued at hundreds of billions—deploying core technology R&D at Zhongda University is by no means a "non-operational" move, but rather a deep and substantial business strategic move.

3. Crossing the SEC's red line: Facing executive bans and hefty fines

According to U.S. securities regulations, AppLovin's actions constitute multiple serious violations:

False statements and securities fraud: The CEO's public statements were completely contrary to the facts and violated the SEC's anti-misleading statements rules;

Disqualification from serving as an executive: Referring to the SEC v. Scott D. Sullivan case, Adam Foroughi could be permanently banned from serving as an executive of a publicly traded company.

Recovery of illegal gains: Profits from stock sales since May 2025 may be fully recovered;

Risk of falsifying accounting records: If the salary expenses of hundreds of engineers in the Beijing and Hangzhou teams are falsely recorded, they will face huge fines, similar to the SEC v. Monsanto Company case.

Even more seriously, Deloitte, the legal counsel, and the financial institutions that recommended the stock to AppLovin, if found to have failed to report the matter, may face the revocation of their professional licenses or even criminal prosecution.

III. Follow-up Preview: Three Deadly Pieces of Evidence Are About to Be Revealed

As of January 22, 2026, AppLovin's stock price had fallen 2.22% to $520.755, with a total market capitalization of $175.992 billion. But this is just the beginning. CapitalWatch has obtained key records from AppLovin's internal systems, and the next round of revelations will focus on three core areas:

1. Data Security Crisis: CUHK Team Accesses US User Privacy

The chain of evidence shows that AppLovin's permission system allowed its Beijing and Hangzhou teams to access core privacy data from a massive number of US-based devices. From IAM role configurations and database access policies to VPN audit logs and data outbound records, the complete evidence proves that this is not just a simple compliance issue, but a national security incident involving US data sovereignty.

2. 40%-60% internal discount: A fraudulent tactic to inflate revenue figures by incurring losses.

AppLovin artificially inflated the installation volume and revenue of its games through internal subsidies (settlement discounts of 40%-60% of market price). A prime example is its strategic investment in Magic Tavern, whose Project Makeover achieved peak monthly revenue exceeding 300 million yuan, but this growth was actually achieved through AppLovin's internal subsidies, resulting in losses to generate momentum for its IPO.

3. The Myth of High ROAS Debunked: The Digital Illusion of a Closed-Loop Perspective

The "high return on investment (ROAS)" that Axon Engine claims to offer is not a true incremental capability, but rather stems from the advantages of the MAX/AXON closed-loop ecosystem and its internal circulation. Once the metrics are changed to real metrics such as net profit and cash recovery, its performance will decline significantly, which is seriously inconsistent with the public narrative.

In conclusion: Lies will eventually be exposed; the storm has only just begun.

AppLovin attempted to deceive the market by exploiting cross-border information asymmetry, but business records don't lie, job advertisements don't lie, employee tracking doesn't lie, and the flow of funds from criminal groups certainly doesn't lie. From a "money laundering channel" for Southeast Asian black markets to businesses where the CEO himself fabricated information, every glamorous label on this Nasdaq-listed company conceals unspeakable dirty deals.

CapitalWatch has issued a warning: stop responding with empty statements. As more evidence continues to emerge, the valuation bubble of $APP will eventually burst, and those responsible will inevitably face severe legal penalties. For investors, the most important thing now is to see through the nature of this scam and stay away from this "time bomb" that could explode at any moment.

We will continue to follow this battle between transnational financial crime and securities fraud.

Disclaimer: This article is for market information interpretation and opinion sharing only, and does not constitute any investment advice. The market is risky, and investment requires caution. Readers should make independent judgments and decisions, and bear all risks themselves.