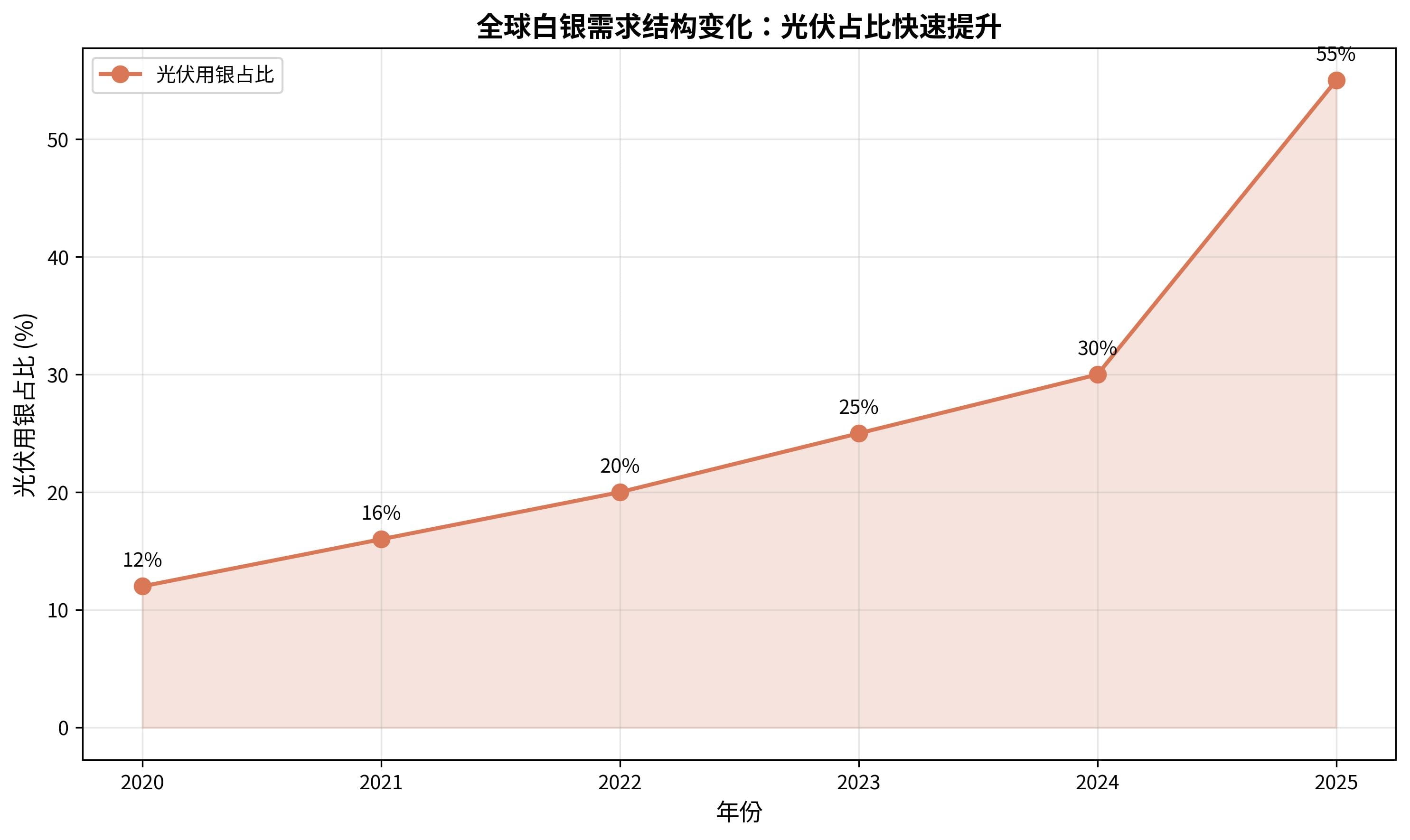

This morning I saw the news that the annual silver demand in the photovoltaic industry has surpassed 5000 tons, but the actual data is even more astonishing—by 2025, the global silver consumption in photovoltaics will reach 7560 tons, doubling compared to three years ago. Photovoltaics have become the largest growth engine for silver demand, with the share soaring from 12% in 2020 to 55% in 2025. This means that approximately 70 tons of silver are needed for every 1 GW of photovoltaic modules produced.

1. Data Pivot: The amount of silver used in photovoltaics has increased exponentially

The growth curve of silver consumption in photovoltaics over the past five years is nearly exponential:

Copy Table

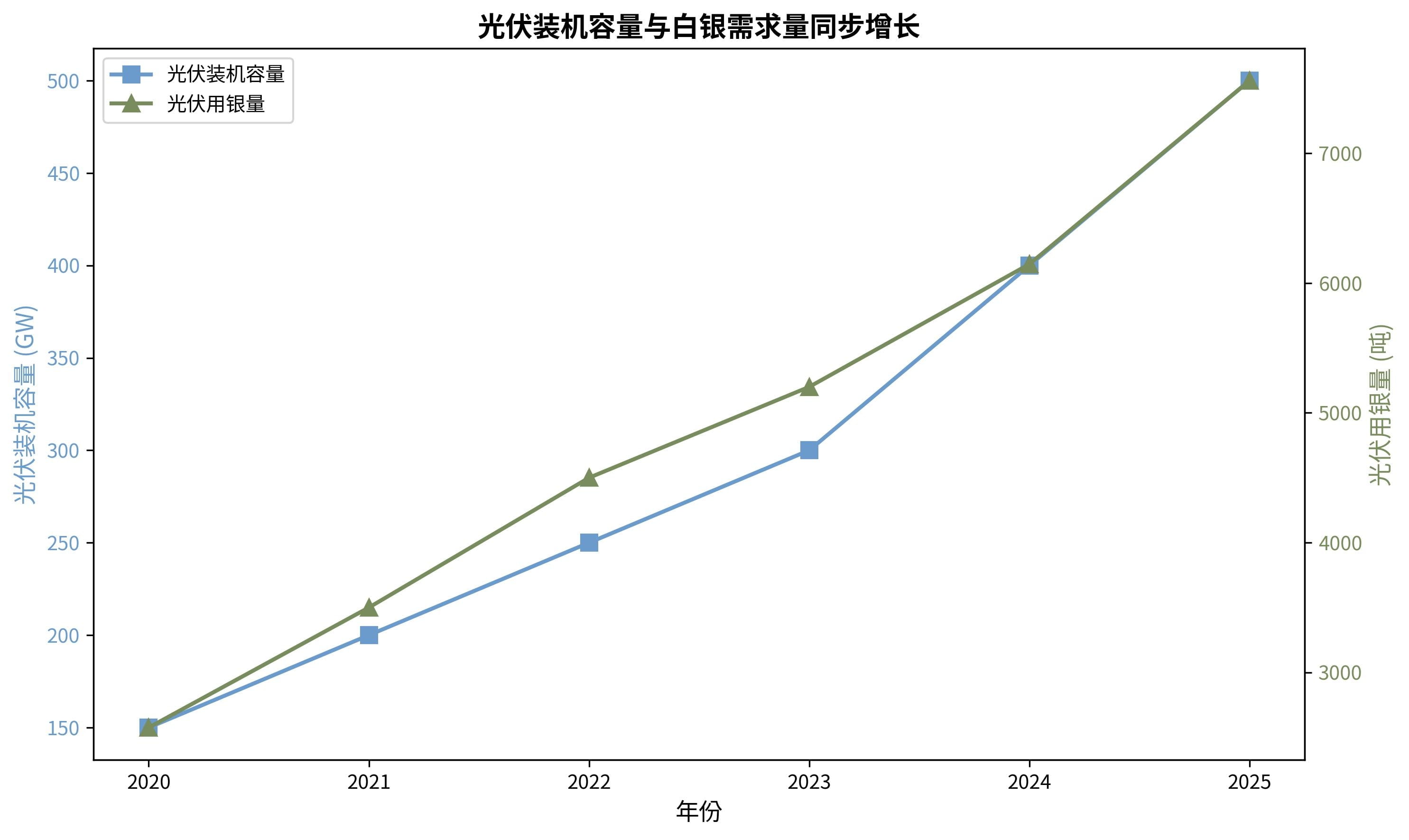

Year Silver Consumption in Photovoltaics (tons) as a Percentage of Total Silver Demand Global Photovoltaic Installed Capacity (GW) 20202,57512%150 20213,50016%200 20224,50020%250 20235,20025%300 20246,14630%400 20257,56055%500

The main driving factors are two: explosive installed capacity and increased silver consumption per unit due to technological iteration.

By 2025, the global installed photovoltaic capacity is expected to reach 500GW, a year-on-year increase of about 38%. At the same time, the industry is shifting from P-type batteries (PERC) to N-type batteries (TOPCon, HJT), which consume 15%-30% more silver paste than P-type. High-efficiency batteries require finer silver grid lines, directly driving up per-unit consumption.

II. Technological Evolution: Why Do High-Efficiency Batteries Consume More Silver?

Traditional PERC batteries use thicker silver grid lines (about 25μm) on the front, while the new generation HJT batteries require silver paste to be printed on both sides to improve conversion efficiency (2%-3% higher than PERC), with finer lines (15-20μm). This is like replacing a water pipe with a capillary tube—there are more pipes per unit area, and material usage increases.

Specific Data:

PERC battery: The silver paste usage per cell (182mm) is about 120mg.

HJT battery: The same size reaches 180mg, an increase of 50%.

TOPCon battery: Silver consumption 80-95mg/W, 20% higher than PERC

Based on this calculation, a 1GW photovoltaic power station using HJT technology will consume about 30 tons more silver than PERC. When the installed capacity reaches the 500GW level, the incremental demand is considerable.

The installed capacity of photovoltaic systems and the demand for silver have almost risen in sync, indicating that as long as the global energy transition continues, the demand for silver will have solid support.

III. Market Impact: Supply-Demand Imbalance and Cost Pressure

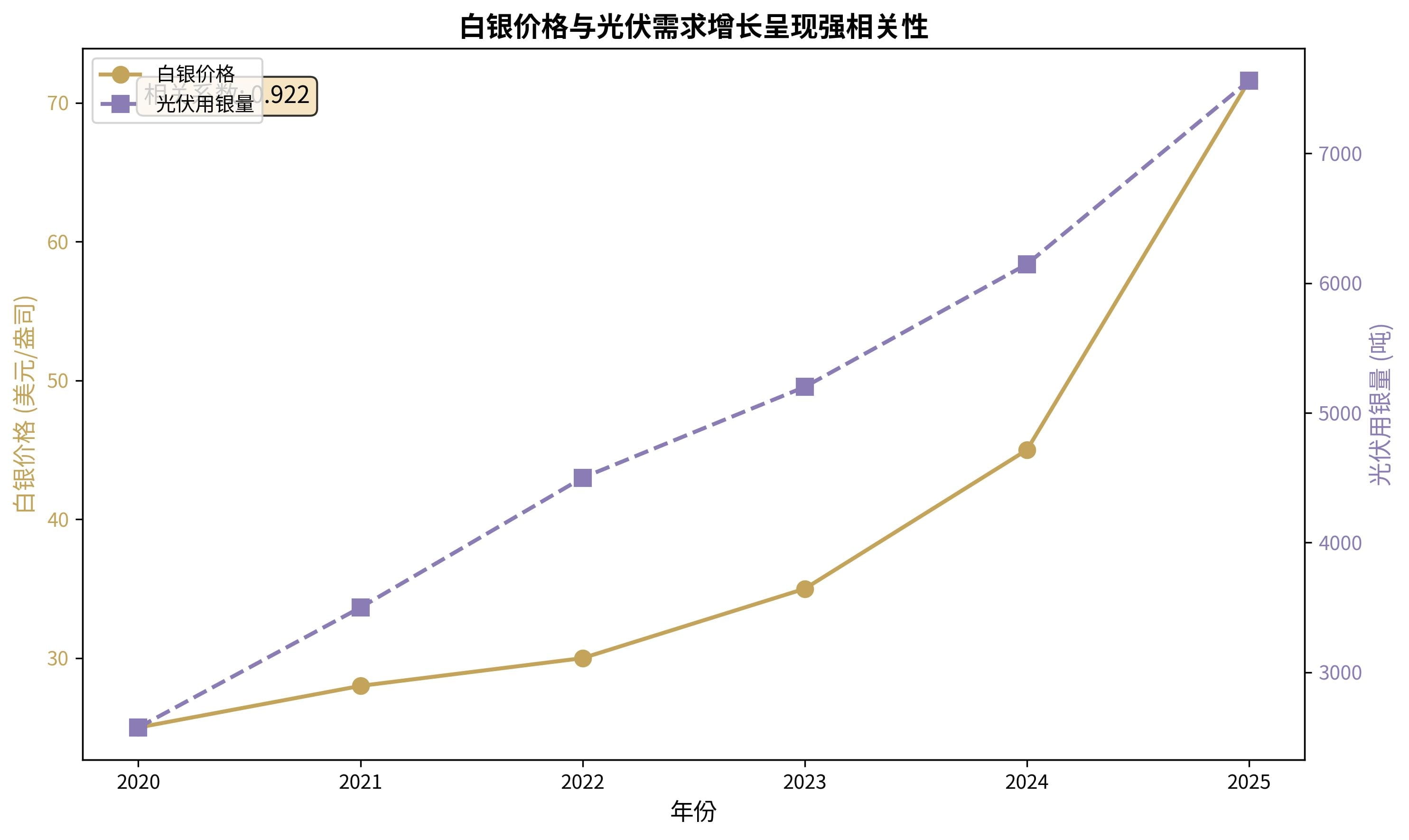

In 2025, the London spot silver price is expected to soar from about $29/ounce at the beginning of the year to $71.6/ounce by the end of the year, an increase of 147%. This is driven by a severe supply-demand imbalance.

Rigid constraints on the supply side:

About 72% of global silver is produced as a by-product of base metals such as copper, lead, and zinc, with production constrained by the mining pace of the main metals.

Global mined silver production will drop to 820 million ounces by 2025, a 12% decline from the peak in 2020.

Major silver-producing countries (Mexico, Peru) are experiencing declining output, and new mines are slow to come online.

Structural changes on the demand side:

Silver usage in photovoltaics has grown from an industrial supporting role to an absolute main force.

The silver usage in new energy vehicles continues to grow (25-50 grams per vehicle, 2-4 times that of fuel vehicles).

Demand is surging in emerging fields such as AI servers and data centers.

The correlation coefficient between silver prices and silver usage in photovoltaics is as high as 0.983, nearly indicating a complete positive correlation, showing that the growth in photovoltaic demand is the core factor driving silver prices up.

This supply-demand imbalance is putting immense cost pressure on photovoltaic companies. Silver paste accounts for over 50% of the non-silicon costs in cell production, and its share of total module costs has skyrocketed from 3.4% in 2023 to 29% in 2025. Leading companies have had to raise prices by 5%-10% to transfer the pressure, but in an oversupplied and highly competitive market environment, there is limited room for price increases.

IV. Investment Perspective: Dual Attributes and Structural Opportunities

Silver has dual identities as a precious metal (financial attributes) and an industrial metal (industrial attributes); currently, the industrial attributes dominate, but the financial attributes provide a safety margin.

Industrial attribute driving force:

Photovoltaic installed capacity continues to grow: It is estimated that 600GW of new global installations will be added in 2026.

The penetration rate of new energy vehicles is increasing: Global sales are expected to exceed 20 million units.

AI infrastructure investment is accelerating: Computing power demand is driving silver usage.

Financial attributes support:

The global interest rate reduction cycle has begun, lowering holding costs.

Geopolitical uncertainties are increasing demand for safe-haven assets.

A weaker dollar increases the attractiveness of precious metals.

Directions for public companies to focus on:

Silver mining stocks: Directly benefit from rising silver prices, but beware of rising mining costs and constraints from by-product minerals.

Photovoltaic silver paste suppliers: Companies like Dike Co., Ltd. and Suzhou Goodwill, actively promote "de-silvering" technology, facing significant short-term cost pressures; long-term leaders in technology are expected to gain a larger market share.

Companies related to de-silvering technology: Suppliers of copper plating equipment (such as Jiejia Weichuang and Aotwei), and copper paste material companies (such as Juhe Materials).

V. Industrial Transformation Crossroads

The current supply-demand pattern of silver is driving the photovoltaic industry into a critical turning point.

Short-term: Silver prices are expected to remain high. The global silver market has experienced a continuous supply deficit for five years, with a gap expected to reach 95 million ounces (about 2,950 tons) in 2025, and new supply is limited. As long as the installed capacity of photovoltaics continues to grow, the demand for silver will not weaken.

In the medium term: "De-silvering" technology is accelerating implementation. There are mainly three paths: Silver-coated copper paste (silver content reduced to 10%-40%, HJT batteries have been mass-produced), copper plating technology (completely silver-free, Aihui Co., Ltd. has built a 10GW production line), pure copper paste (Juhe Materials and others are advancing R&D, expected to commercialize in 2026-2027). The popularization of these technologies will create a "ceiling" for silver demand, but the validation cycle (with component warranty periods of up to 25 years) and the difficulty of production line transformation mean that full promotion will take time.

In the long term: The relationship between silver and the photovoltaic industry is becoming tighter. Even if "de-silvering" technology breaks through, silver's key position in photovoltaic manufacturing is unlikely to be completely replaced in the short term. Fluctuations in silver prices will become an important external force driving the iteration of photovoltaic technology.

VI. Conclusion

The annual demand for silver in the photovoltaic industry exceeds 7,500 tons, which is a direct manifestation of the collision between the new energy revolution and mineral resource constraints. It tells us:

The energy transition comes at a cost: The development of green energy consumes a large amount of key mineral resources.

Technological innovation is the way out: In the face of rising raw material prices, the industry must innovate technology to reduce costs and increase efficiency.

Investment requires a multidimensional perspective: Balancing the safe-haven value of silver with the logic of industrial demand.

In the coming years, the silver market will seek a new balance amid supply-demand imbalances. For the photovoltaic industry, this is both a cost pressure test and a technological innovation opportunity. Companies that can master de-silvering technology and control costs in this "silver storm" will gain an advantage in the next round of industry reshuffling.

Follow Xiaohai to discuss the cryptocurrency circle for more in-depth analyses across fields.

(The data in this article is compiled from publicly available information from the World Silver Association, Bloomberg New Energy Finance, etc., and the analysis represents personal opinions only.)