For years, Ethereum was discussed as a future possibility. A network that could change finance one day. That conversation has quietly ended. What’s happening now is not theory, not testing, and not marketing hype. Major financial institutions are actively using Ethereum to run real products, with real capital, in live markets.

This shift matters because institutions don’t move first for ideology. They move when systems work better, faster, and cheaper than existing ones. And Ethereum is starting to check those boxes.

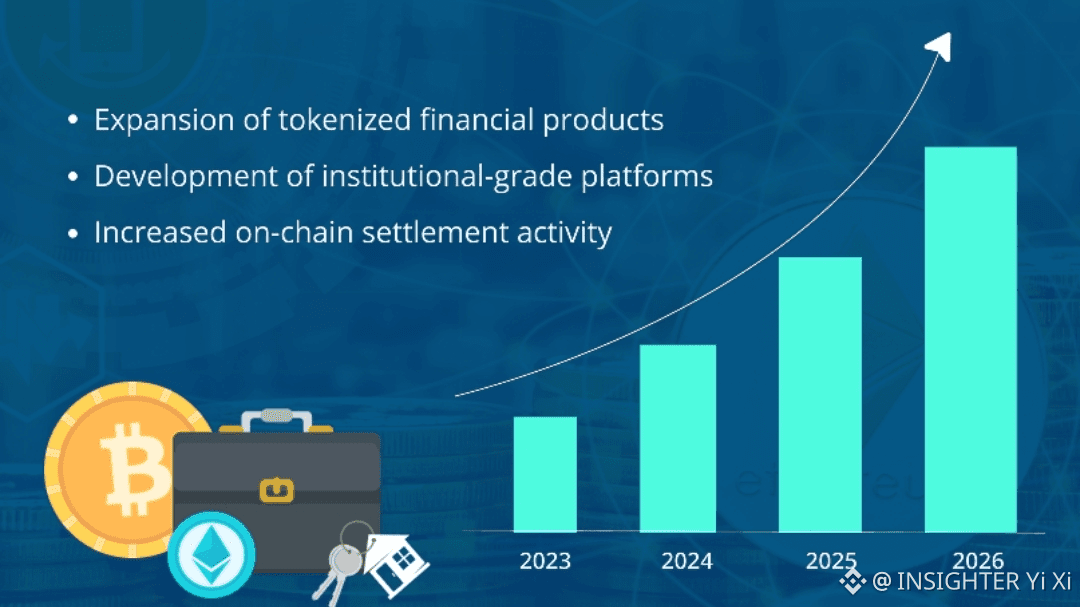

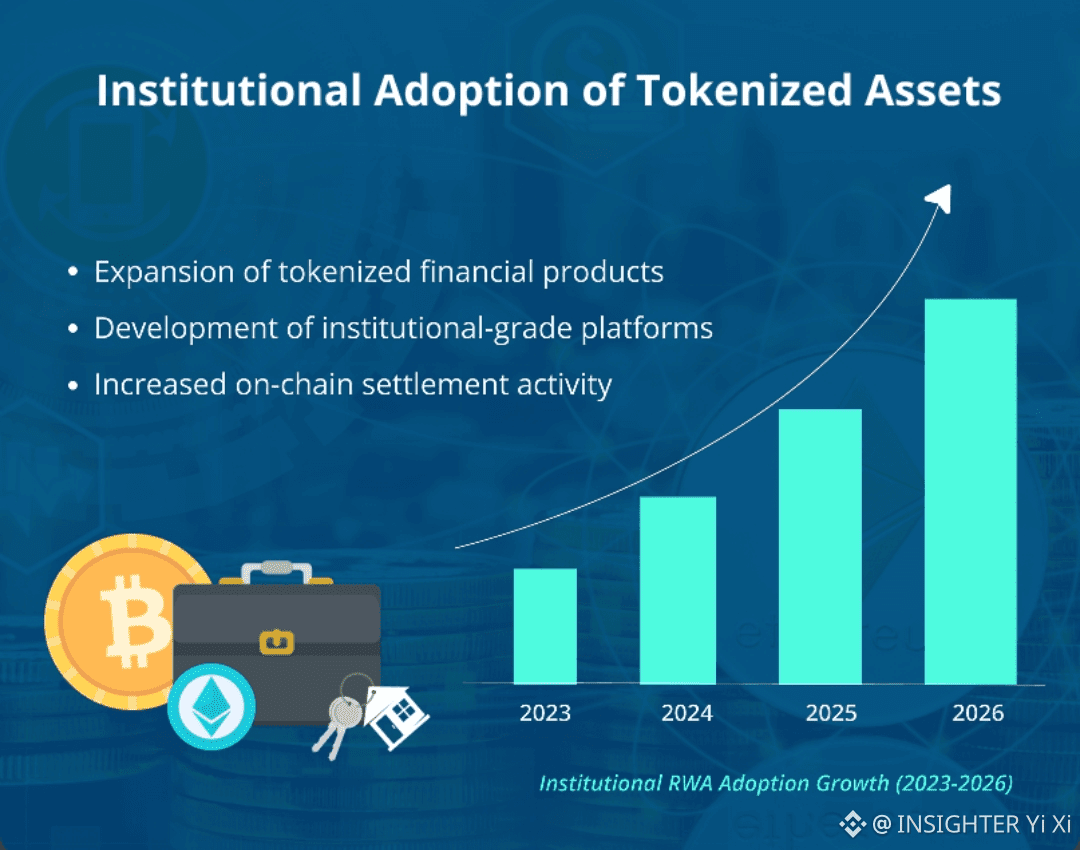

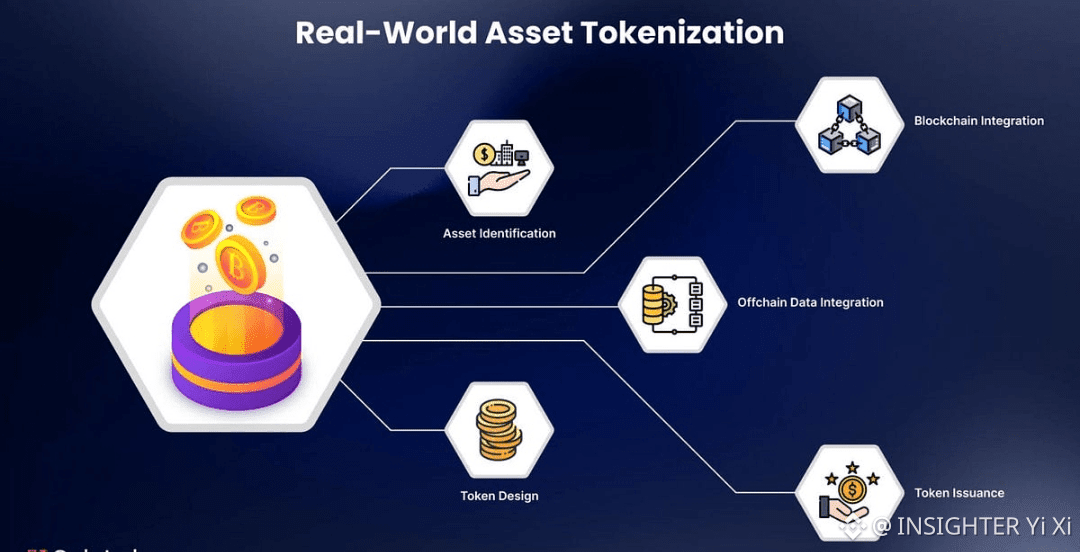

Over the past year, more than 30 large financial firms have launched products directly on Ethereum. These are not crypto-native experiments. They include tokenized stocks, money-market funds, bank deposits, stablecoins, and on-chain settlement systems. The common thread is simple: Ethereum is being used as a neutral base layer for moving and settling value, similar to how the internet became the base layer for information.

The products themselves reveal the intent. Tokenized U.S. stocks and ETFs are now trading on Ethereum rails. Traditional asset managers are issuing tokenized funds that settle on-chain instead of through legacy clearing systems. Banks are deploying capital into tokenized instruments using their own balance sheets, not customer test funds. Payments companies are expanding stablecoin settlement to bypass slow and fragmented cross-border systems.

This isn’t about replacing banks. It’s about upgrading how money moves between them.

Ethereum offers something legacy finance struggles with: a shared, programmable settlement layer that doesn’t belong to any single institution or country. Assets can move 24/7. Settlement is near-instant. Transparency is native. Rules are enforced by code instead of paperwork. For global finance, those properties are extremely difficult to ignore.

Network data supports this transition. A large portion of ETH is now locked in staking, reducing liquid supply and signaling long-term participation rather than speculative flipping. Wallet creation continues to grow, but more importantly, transaction behavior is shifting toward structured, repeatable flows that resemble settlement activity instead of retail trading noise.

At the same time, Ethereum faces a real challenge. As more institutions build on top, complexity increases. More layers, more tools, more abstractions. Ethereum’s co-founder has warned that unchecked complexity could harm security and user control. This isn’t a technical footnote. It’s the central risk of success. Financial infrastructure must be boring, predictable, and resilient. If Ethereum loses those traits, trust erodes quickly.

This tension defines Ethereum’s current moment.

On one side, global finance is moving on-chain because the benefits are too strong to ignore. On the other, the network must scale without turning into a fragile system only specialists understand. The outcome will determine whether Ethereum becomes a permanent part of global finance or stalls under its own weight.

One thing is already clear.

Ethereum is no longer just a crypto platform people trade on.

It’s becoming a financial coordination layer institutions are actively building around.

Markets usually price narratives early.

Infrastructure gets priced later.$BTC

#WhoIsNextFedChair #TrumpCancelsEUTariffThreat #WEFDavos2026 #GoldSilverAtRecordHighs #BTCVSGOLD $ETH $SOL