I keep coming back to an uneasy question while watching @Dusk trade in real time why does it still behave like a speculative privacy token when its architecture resembles regulated financial infrastructure? That disconnect is the first signal. Markets struggle to price things that don’t fit clean categories. Dusk isn’t “privacy” in the Monero sense, and it isn’t traditional compliance infrastructure either. It embeds regulatory constraints directly into cryptography, which means demand isn’t driven by anonymity seekers it’s driven by institutions trying to minimize friction. That kind of demand arrives late, but once it arrives, it tends to stay.

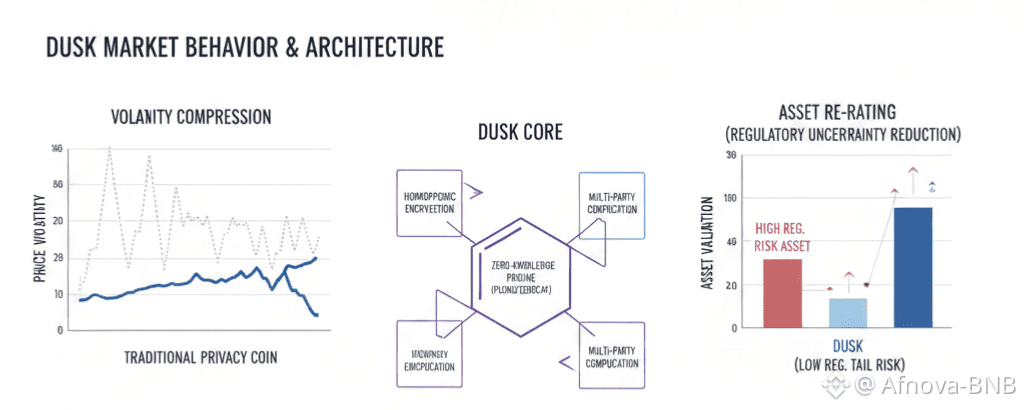

The second shift in perspective comes from treating zero-knowledge not as a feature, but as a cost-reduction mechanism. PLONK and ZeroCaf aren’t just technical achievements; they compress the marginal cost of privacy. Older privacy chains sacrifice performance to obscure data. Dusk inverts that trade-off: privacy is the default execution path, optimized in Rust and built around curves that favor efficient proofs. Liquidity cares about that. High-overhead systems amplify volatility—fees spike, confirmations wobble, market makers pull back. By removing those stress points at the base layer, Dusk creates conditions where volatility compression can happen before adoption, not after.

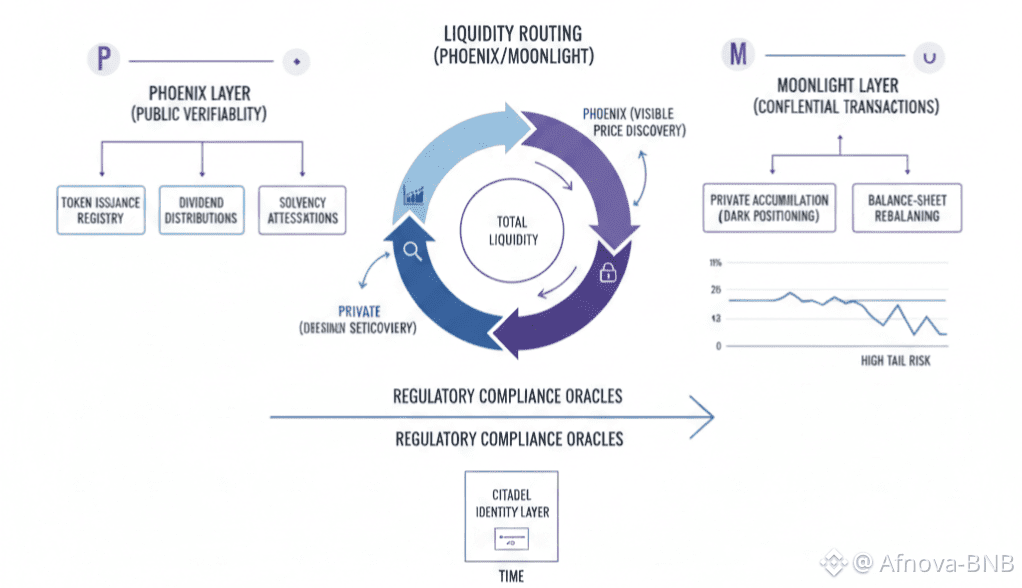

The Phoenix–Moonlight split is where my assumptions really start to break down. Most chains force a binary choice between transparent and private. Dusk allows applications to move between modes within the same flow. That isn’t a UX flourish—it’s control over market structure. Phoenix anchors public verifiability: issuance, dividends, solvency proofs. Moonlight conceals intent: accumulation, secondary trading, balance-sheet rebalancing. When both exist together, liquidity doesn’t disappear—it reroutes. Price discovery stays visible while positioning goes dark. Traders consistently underestimate how constructive that is for sustained volume.

At that point, I stop thinking about users and start thinking about issuers. Tokenized bonds, equities, and funds aren’t ideological—they care about compliance surface area. Citadel’s zero-knowledge identity layer reframes identity from permanent exposure into conditional proof. Permission to transact becomes separable from who the actor is. From a market standpoint, that reduces regulatory headline risk, which lowers discount rates on future cash flows. Assets that reduce regulatory uncertainty don’t explode upward—they quietly re-rate.

Another signal appears when I watch on-chain behavior during low-volume periods. Dusk activity thins, but it doesn’t evaporate the way incentive-driven chains do. Systems propped up by subsidies hollow out in drawdowns. Systems tied to necessity—settlement, reporting, compliance—keep moving. That persistence rarely shows up on charts at first. Liquidity providers notice it before anyone else. Then spreads tighten. Then narratives follow.

There’s also a subtler angle around censorship risk. Fully public chains expose too much; fully private ones expose too little. Both invite pressure. Dusk’s selective disclosure acts as a pressure-release valve. Regulators don’t want raw data—they want specific proofs. By offering cryptographic assurance instead of blanket transparency, Dusk lowers the incentive for heavy-handed enforcement. From a trading perspective, that reduces tail risk. Assets with lower tail risk don’t pump fast—but they survive long enough to compound.

The last realization is uncomfortable but important: Dusk may never become a retail favorite. And that’s fine. Its real market isn’t social sentiment; it’s existing financial infrastructure migrating on-chain. When that shift happens, it won’t look like a hype cycle. It will look like quiet integrations, steady blockspace demand, and an asset that slowly stops behaving like a lottery ticket and starts behaving like collateral.

So when I see Dusk drifting sideways while shipping this kind of architecture, I don’t read it as weakness. I read it as patience being mispriced. And markets have a long history of eventually correcting that particular inefficiency.