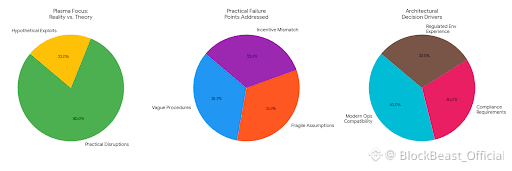

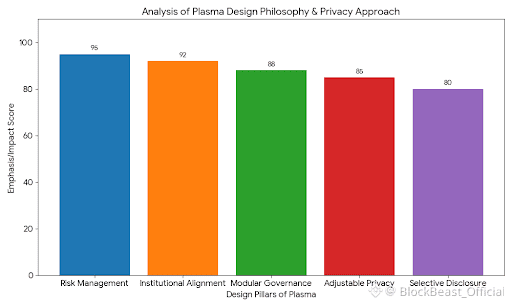

Plasma comes across less as a manifesto about reinventing money and more as an effort to make blockchain systems compatible with the realities of modern payment operations. That difference is significant. Experience inside regulated financial environments tends to shift focus away from hypothetical exploits and toward the issues that actually disrupt systems in practice: vague procedures, fragile assumptions, and incentive structures that clash with compliance requirements. Many of Plasma’s architectural decisions appear shaped by an awareness of those practical failure points.

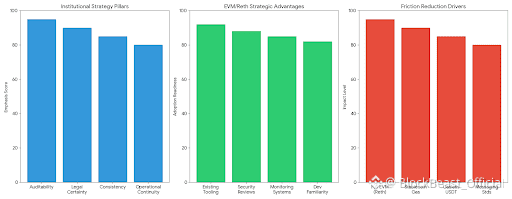

Fundamentally, Plasma treats stablecoins as the core medium of settlement rather than as just another application running atop a general-purpose chain. This reversal is subtle but important. In conventional financial infrastructure, money itself is not an abstraction layered on later—it is the foundation that determines messaging standards, risk frameworks, and operational processes. By making stablecoins central instead of relying on a volatile native token, Plasma aligns more closely with how payment rails are assessed in real-world contexts: through consistency, auditability, and legal certainty. Elements such as stablecoin-denominated gas fees and gasless USDT transfers are less about end-user convenience and more about removing sources of friction that can halt institutional adoption over seemingly minor ambiguities.

Its decision to maintain full EVM compatibility using Reth reflects a cautious approach to developer and operational risk. From an institutional perspective, unfamiliar technology introduces uncertainty. Custom virtual machines, new programming models, or unconventional execution semantics expand the scope of audits and slow internal approval processes. While EVM compatibility does not inherently guarantee security, it does provide continuity. Existing tooling, monitoring systems, and security review practices can be reused rather than rebuilt, reducing the number of unknown variables institutions must evaluate before committing resources or integrating infrastructure.

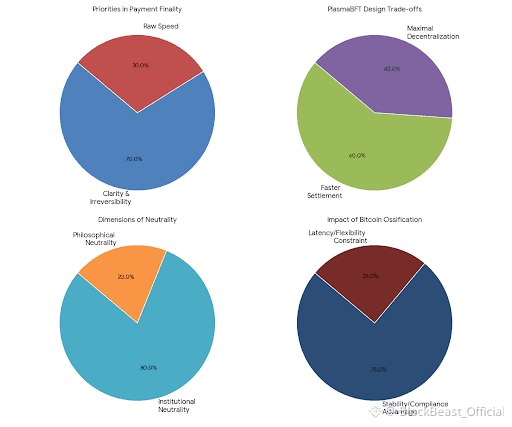

The use of PlasmaBFT to achieve sub-second finality follows the same pragmatic logic. In many payment and settlement environments, finality is valued less for speed alone and more for clarity. Institutions need to know precisely when a transaction is irreversible and under what conditions. Faster confirmation is only meaningful if the guarantees can be clearly articulated to auditors and risk committees. Introducing a custom consensus model inevitably adds new trust assumptions, and Plasma appears to acknowledge rather than obscure that reality. The design treats faster settlement as a deliberate trade-off against maximal decentralization, framing it as a conscious decision rather than an accidental compromise.

Anchoring security to Bitcoin reflects a particular interpretation of neutrality that resonates with regulated finance. Here, neutrality is not primarily philosophical; it is institutional. Bitcoin’s governance is slow-moving, conservative, and resistant to rapid change or capture. While this rigidity is often criticized within crypto-native communities, it is advantageous from a compliance standpoint. Systems that evolve too quickly are difficult to assess, insure, and regulate. Bitcoin’s relative ossification provides a stable external reference, even if it introduces latency and constrains flexibility.

Privacy is approached with comparable restraint. Rather than positioning privacy as absolute secrecy, Plasma treats it as adjustable. This mirrors established financial systems, where confidentiality must coexist with auditability and lawful oversight. Mechanisms that allow selective disclosure—enabling parties to demonstrate compliance without exposing unnecessary information—are not regulatory concessions but operational necessities. Fully opaque systems may be rhetorically attractive, but they are incompatible with most institutional mandates. Designing for varying degrees of visibility allows participation by users and entities with very different regulatory obligations.

The separation between consensus and execution further underscores a design philosophy oriented around risk management. Modularity does not automatically imply superiority, but it does create clearer boundaries when things go wrong—which they inevitably do in production systems. Isolating failures becomes easier when components are loosely coupled. This separation also simplifies governance: changes to execution environments can be assessed independently from consensus modifications, reducing the potential impact of errors and aligning better with slow-moving change management processes common in regulated organizations.

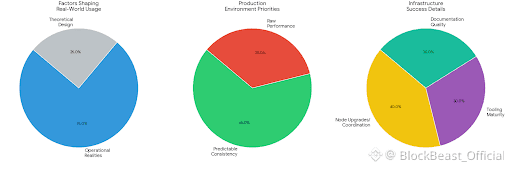

Plasma does not attempt to obscure its constraints. Bitcoin anchoring introduces real settlement delays, especially for workflows that depend on rapid cross-chain finality. Trust assumptions around bridges and migration mechanisms remain unavoidable. Operational realities—validator coordination, upgrade procedures, and incident response—will ultimately shape real-world usage more than theoretical design advantages. A serious infrastructure project acknowledges these limitations early because they influence everything from service guarantees to regulatory disclosures.

Much of what determines success here lies in the unglamorous details of infrastructure. Node upgrades are not merely technical updates; they carry operational risk. Poor coordination can cause downtime, inconsistent state, or even compliance violations if transaction processing becomes unclear. Tooling maturity affects whether problems are caught proactively or only after users are impacted. Clear documentation determines whether integrations work correctly from the outset or require repeated fixes under pressure. In production environments, consistency often outweighs raw performance. Predictable behavior, even if imperfect, is easier to trust than speed paired with instability.

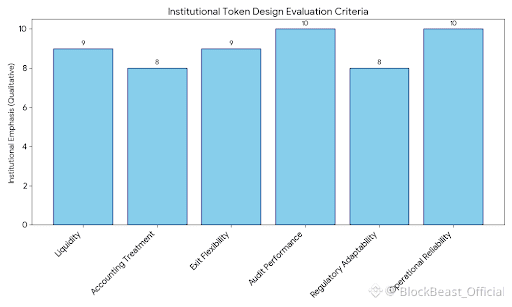

From an institutional standpoint, token design is evaluated less on speculative potential and more on liquidity, accounting treatment, and exit flexibility. Participants need to know whether positions can be entered and unwound without market disruption, whether holding a token creates balance-sheet complications, and whether its function is narrowly defined. Conservative token economics—avoiding tight coupling between core functionality and speculative incentives—lower barriers for organizations accountable to financial statements rather than narratives.

Ultimately, Plasma presents itself as infrastructure designed to withstand scrutiny rather than generate hype. Its success is unlikely to be measured through social traction or short-term growth metrics. Instead, it will be evaluated on quieter criteria: the ability to pass audits cleanly, adapt to regulatory shifts without destabilizing the system, and operate reliably over long time horizons. For those who have watched systems fail not due to lack of vision but due to insufficient discipline, this focus on durability, clarity, and operational modesty may be its most compelling strength.