Recently, an article from Santiago (an OG investor who entered the circle in 2013) caused a huge stir in the English community. He analyzed the structural problems facing the current cryptocurrency industry in a rational and systematic way: even with favorable regulations, institutional entry, and improved infrastructure, the prices did not respond. This observation deserves serious consideration from all long-term participants.

1. Overview

Because the entire cryptocurrency market is often disconnected from reality. Bitcoin is a unique existence — a perfect narrative: digital gold. Its market value is approximately $1.9 trillion, while gold is about $29 trillion. Less than 10% of gold's market value, with room for growth in the future. This is a well-understood hedge + options value combination.

But combined, Ethereum + Ripple + Solana + everything else surprisingly has a market value of ~1.5 trillion dollars, making the narrative less stable.

Although no one questions the potential of this technology anymore, and very few say it's a scam, the real question is:

Can an active user really be worth tens of trillions in an industry with only 40 million?

Meanwhile, OpenAI is rumored to IPO at a valuation close to $1 trillion, with user numbers about 20 times that of the entire crypto industry.

How much real value have these chains actually created? Can they support so much money?

In the past, making money was simple: invest in infrastructure. Early holding or participating in ETH, SOL, DeFi.

But now many projects' pricing defaults to the assumption that there will definitely be 100 times the usage and 100 times the revenue in the future, and after issuing tokens, they become ghost chains.

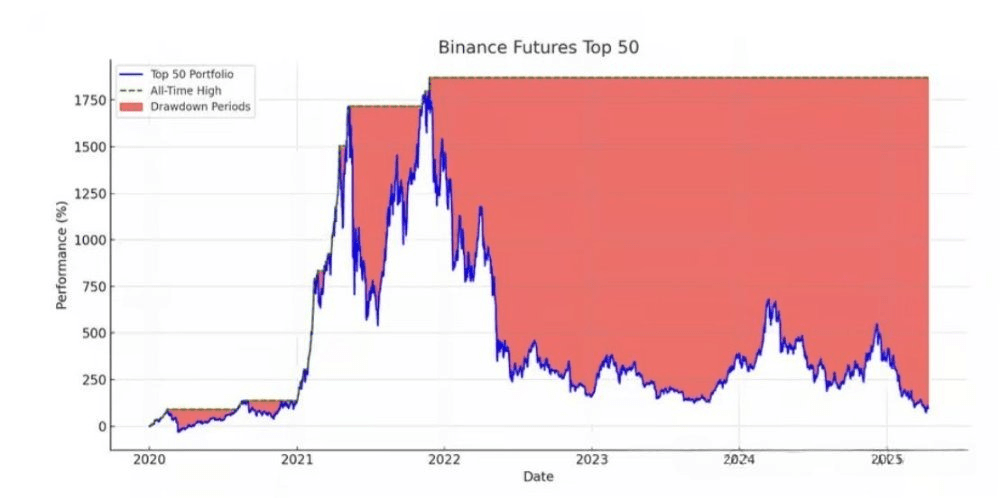

Comparing to NVDA makes it clear how big the crypto bubble is

Compare with the 'gods' of the tech world—Nvidia, its valuation is 40–45x earnings (not revenue).

While Nvidia has:

Real income

Real profit

Global enterprise demand

Predictable contract sales

And non-casino users

2. Core viewpoints

Narrative dividend decline: The market can no longer drive prices up based solely on concepts.

User structure changes: a significant loss of retail investors, with the ability to absorb far lower than in the past two cycles.

Institutional behavior rationalization: VC, market making, project team selling pressure is ongoing and highly certain.

Token utility is overestimated: 90% of projects do not have rigid demand.

Weakening value capture: fees do not flow back, and the disconnection between protocols and tokens is common.

Liquidity centralization: BTC, ETH, leading L2, leading Infra occupy the vast majority of funds.

The stagnation is not a coincidence, but a structural trend.

3. Industry background

3.1 The market enters a 'low increment + excessive competition' phase

The growth of the crypto market in recent years mainly comes from:

Retail money pouring in

Yield narrative-driven (DeFi, GameFi, AI narratives, etc.)

Token incentives + Airdrop expansion

Low interest rate easing cycle

But from 2022–2025:

Macroeconomic liquidity tightening

Retail activity is declining

Airdrop is harder to stimulate new users

High-frequency narratives lead to attention dilution

L2, AI Infra and other tracks are overly crowded

Currently, the situation is:

Most tokens have no reason to support huge valuations

Value capture is limited

Income mainly relies on the cyclical speculation of casino products

3.2 Significant changes in user structure and liquidity

Core trend: Attention, users, liquidity are highly concentrated.

4. Core problem analysis: Why can’t tokens rise?

4.1 First layer reason: Lack of real demand

Most tokens assigned 'value capture scenarios' have not materialized in reality, including:

Governance is not demand (participation is almost zero)

Gas is not demand (the chain itself does not require a lot of Gas)

Staking is not demand (staking does not bring real income)

Transaction fees are extremely low, and annual fee sharing is insufficient to support market value

Use cases are not tied to the token (protocol use ≠ token use)

Summary:

Investors like to discuss TPS, block space, and various complex rollup technologies, but users actually only care about four things: cheap, fast, simple, and can it solve the problem—so the most important thing is always: who are the users, and what do they want to solve.

4.2 Second layer reason: Selling pressure is deterministic and continuous

The structure of the crypto market creates immense long-term selling pressure:

Venture capital unlocking and selling pressure

Project team affiliation (Vesting)

LP reward selling pressure

Market making costs and liquidity maintenance

Token releases incentivized by DAO

Cross-chain bridge operational funding needs

On the supply side:

Sellers are certain, buyers are uncertain.

This is the structural dilemma of the vast majority of tokens.

4.3 Third layer reason: Capital + narrative dual centralization

Funds are rapidly concentrating towards the head:

Mainly flowing to BTC / ETH

Redistributed to SOL, TON, strong L2

Radiating to a few star narrative tokens (AI, ZK, Restaking)

Small and medium projects have extremely low 'visibility' in competition:

Unable to gain sustained attention

No deep liquidity support

No funding pool to support prices

No community builds long-term buy orders

Leading to:

The project is doing well, but the token still has no buy orders.

4.4 Fourth layer reason: Decoupling of protocol value and token value

Such projects are very common in the current cycle:

Protocol trading volume increases

User activity growth

Fee increases

Ecosystem expansion

TVL growth

But token performance is completely stagnant.

This is because:

The money earned by the protocol did not return to the token.

Common scenarios include:

Transaction fees belong to LP / Validator, not the tokens

Token inflation is too high, drowning out yields

Tokens are just 'governance tokens', with weak value capture

The project team deliberately avoids the risk of 'tokens as securities', leading to conservative value design

Ultimately forming a classic industry phenomenon:

‘The protocol is good, but the token is bad.’

5. What does it mean for investors?

5.1 Value capture > The technology itself

By 2025, technology will not be a scarce commodity; the design of token value capture will be the most scarce capability.

Investment logic must shift from:

'If the project does well' → 'the token can capture value'

5.2 Three types of tokens worth focusing on

Projects with fee recovery (Fee → Token) structure

Tokens strongly tied to real usage

Compliant with trend narratives + valuable capture of head assets

6. Future outlook

The market doesn’t care about your story; investment returns to fundamentals

No matter how a chain claims to be the 'mother of all chains' or 'world computer', it ultimately depends on:

How much do you actually earn each year?

Are these incomes derived from real economic activities?

Crypto is no longer the only hot topic in the arena

In the past: the 'high beta gambling table' of global venture capital was in Crypto

Now: AI has become the protagonist, Crypto has retreated to a supporting role

Liquidity is selective, AI is the protagonist, crypto is not.

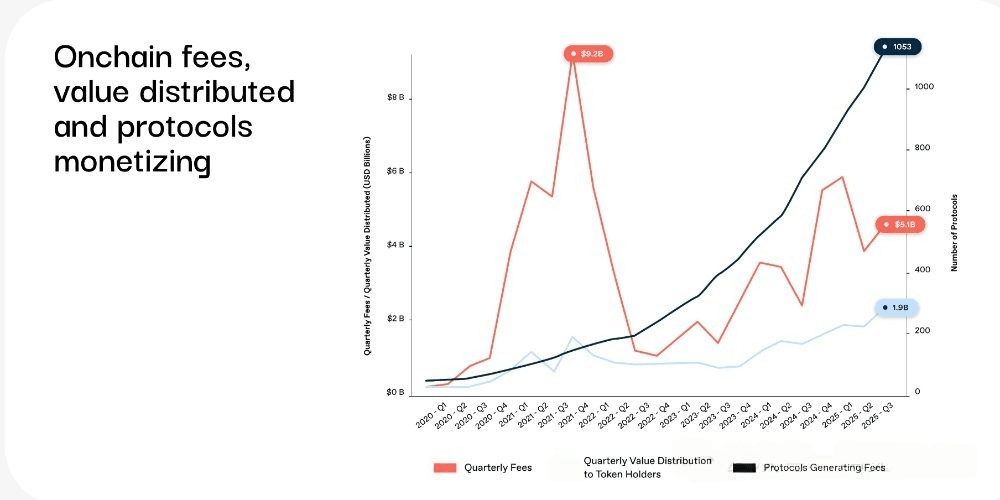

The real 'economic value' roughly comes from:

Transaction fees (Fee), tips (Tips), MEV (extractable value) can barely be considered the 'gross income' of public chains.

In this regard:

Ethereum: Approximately $2 billion in revenue per year, market value ~$400 billion, about 200–400x PS (and it’s still cyclical revenue), Solana: Annualized over $1 billion, market value ~$750–800 billion, about 20–60x PS

Moreover, there’s a more terrifying fact: this is not 'compounding income'

These incomes are not robust, enterprise-level regular incomes, but highly cyclical speculative flows.

This is not SaaS income; this is Las Vegas.

The more critical issue is that these incomes are not compounding, sustainable, or predictable enterprise-level incomes. They heavily rely on speculative flows, hence are essentially closer to Las Vegas than a stable SaaS model. During bull markets, perpetual contracts soar, meme coin fervor, frequent leverage and liquidations, arbitrage bots are active, on-chain fees skyrocket; but in bear markets, trading decreases, minting stagnates, liquidations are rare, on-chain activity plummets, and income almost disappears.

This is not: long-term contracts, or predictable income, but rather: 'three years of no activity, then three years of income' periodic flow. You cannot assign a Shopify valuation multiple to a casino that only fills up every 3-4 years.

7. Conclusion

What should we do now?

· Blockchain technology is not an issue

· Huge potential

· The industry is still in its early stages

What we need to do next is to reassess:

· Evaluate projects based on real usage and 'income quality', not ideology

· Distinguishing 'sustainable income' from 'cyclical casino income'

· The winners of the last cycle are not necessarily the kings of the next cycle

· Stop treating token prices as indicators of technical validation

If tokens have no demand and no value capture, the market will not buy in. No one will choose AWS over Azure just because Amazon's stock price is stronger than Microsoft's for a certain week. We can continue to wait for enterprises to adopt, or we can start pushing it now. Move real GDP onto the chain

The real big opportunity is: embedding crypto technology into already large enterprises, replacing outdated financial pipelines, and improving real business efficiency.

This is the trillion-dollar opportunity.