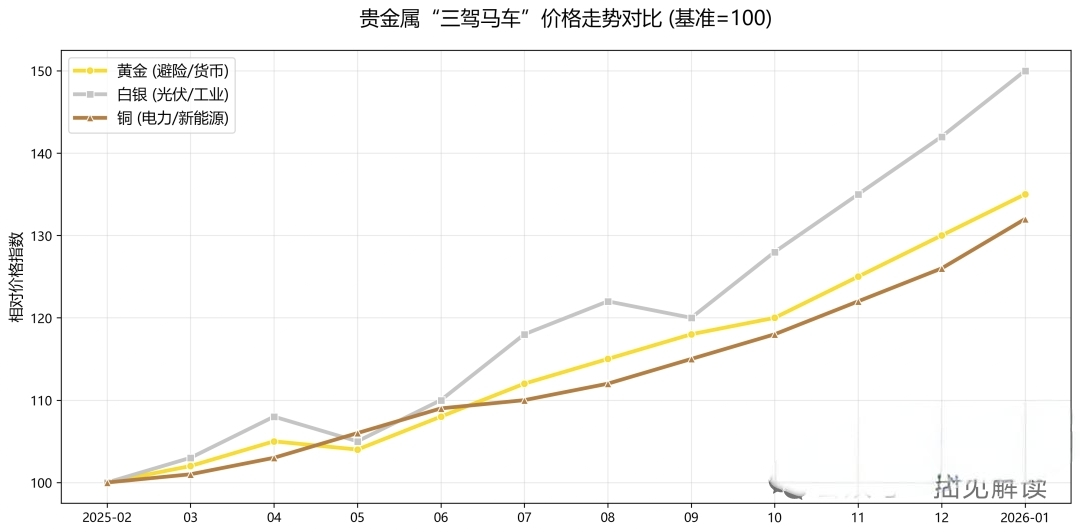

At the beginning of 2026, the global asset market is experiencing a 'dual-track frenzy' that crosses traditional and emerging sectors: gold has broken through the historical high of $4,700 per ounce, with UBS and Deutsche Bank directly setting a target of $6,000; silver skyrocketed 20% in a single month, with an annual increase of 120% in 2025, aiming for the $100 mark; copper prices have stabilized at $10,000 per ton, reaching a ten-year high and aiming for $12,000. Meanwhile, the crypto market is also boiling—gold-pegged PAXG and XAUT tokens saw a year-on-year trading volume surge of 300%, while the locked value (TVL) of mining concept NFTs and DeFi protocols surpassed $20 billion. This resonance celebration of hard assets and digital assets is not merely a coincidence of speculative funds but the inevitable result of the collision of five forces: the Kondratiev wave cycle, the collapse of dollar credit, geopolitical turmoil, energy revolution, and blockchain innovation, which are reshaping the underlying rules of global wealth allocation.

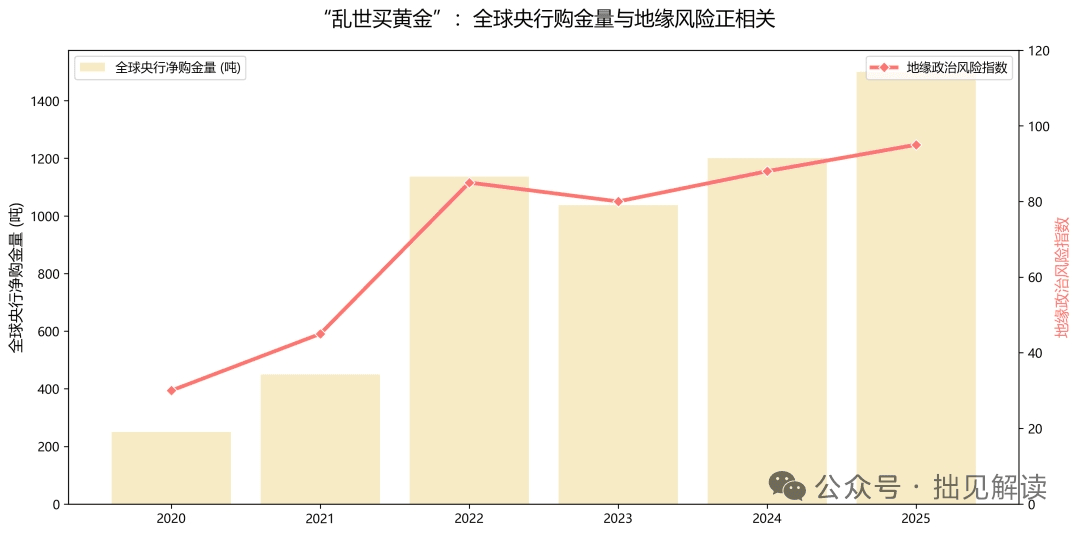

The rise in gold prices signifies the 'return of the king' in the era of credit currencies for super-sovereign assets, while cryptocurrency provides digital wings for this return. Under the dual pressure of Kondratiev waves and global stagflation, the safe-haven properties and value storage functions of gold are pushed to the extreme. Central banks worldwide have begun a 'gold hoarding mode', with net purchases of gold by central banks and ETFs reaching 965 tons between 2022 and 2026, while the increase in mine production and recycled gold can only meet half of the demand, with the supply-demand gap continuing to widen. More critically, the de-dollarization wave is sweeping the globe, with $36 trillion in U.S. Treasury debt weighing heavily, interest payments exceeding $1.5 trillion, and the monetization of fiscal deficits continuously diluting the purchasing power of the dollar, making gold the core choice for various countries to replace dollar assets—non-traditional gold-buying countries like Finland and Brazil are joining the ranks of increasing holdings, and the proportion of gold in global central bank foreign exchange reserves has risen to its highest level since 2010.

In the digital world, the value logic of gold has been completely reconstructed by blockchain technology. Tokens such as PAXG and XAUT, which are pegged to physical gold, achieve a 1:1 asset backing, preserving gold's anti-inflation properties while addressing the pain points of poor liquidity, difficulty in fragmentation, and high storage costs associated with physical gold, becoming a 'bridge asset' connecting traditional finance and the crypto market. Data shows that by 2025, the total issuance of stablecoins pegged to precious metals globally will exceed $5 billion, with PAXG's market value reaching $2.8 billion and daily trading volume increasing by 270% compared to 2024. Even more innovative is the 'gold collateral mining' model, where users deposit PAXG into DeFi protocols, earning stable annualized returns of 8%-12% while participating in arbitrage from gold price fluctuations. This 'traditional assets + on-chain finance' approach has attracted a large number of traditional gold investors, pushing the digital allocation ratio of gold from 0.8% in 2023 to 3.2% by early 2026. Although gold prices may experience a short-term correction of around 10%, the triple support from central banks buying on dips, long-term allocation funds, and on-chain demand has led Deutsche Bank to maintain a positive outlook on its long-term trend, predicting that gold prices could reach $6,000 per ounce within the year, while the market value of crypto tokens pegged to gold may also exceed $10 billion simultaneously.

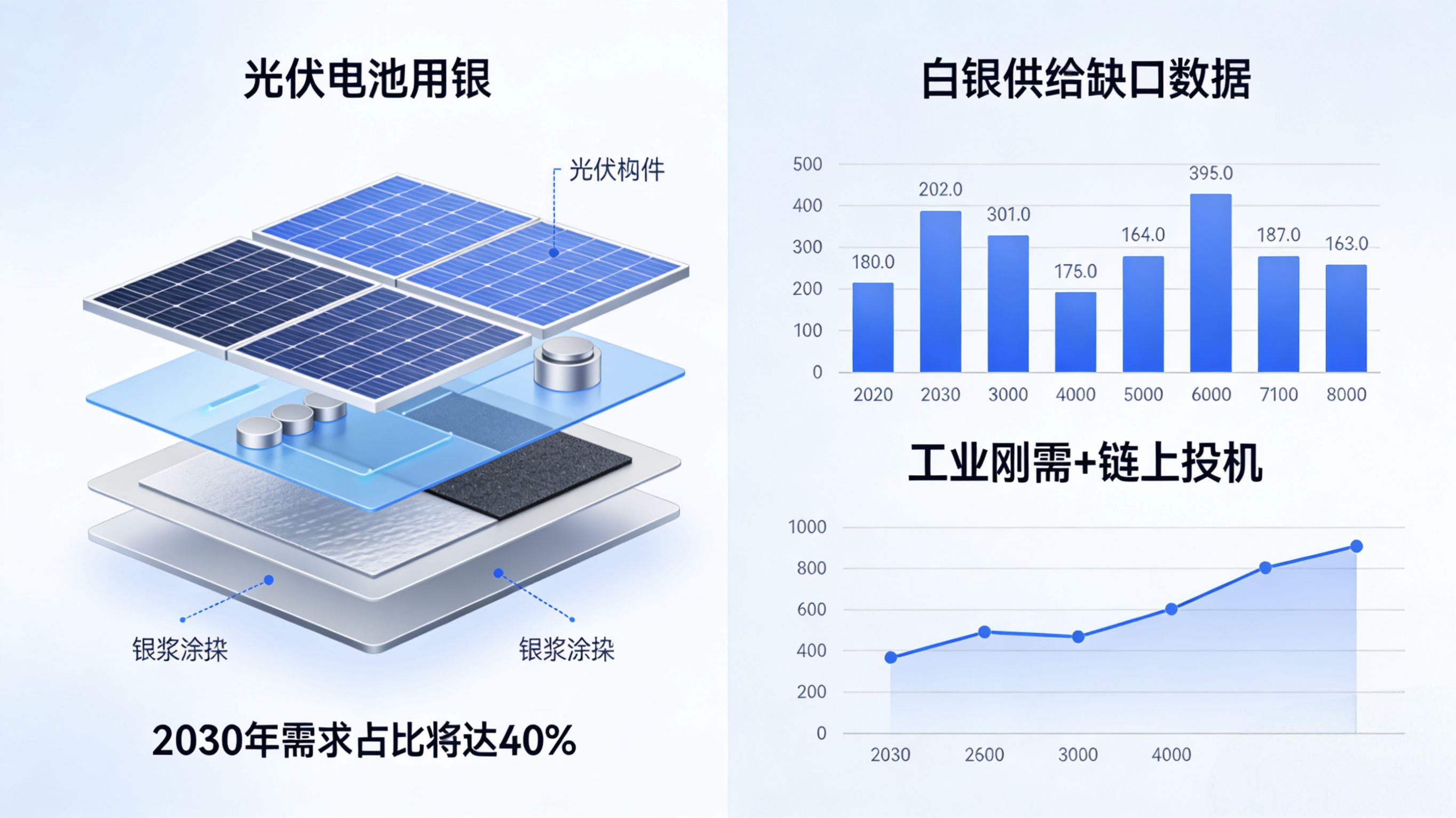

The silver market is characterized by a threefold explosion of 'precious metal attributes + industrial attributes + on-chain speculative attributes', making it the 'king of elasticity' between traditional and emerging markets. The supply side has already sounded the alarm: silver has been in a supply-demand gap for five consecutive years, with a cumulative gap of nearly 820 million ounces from 2021 to 2025, equivalent to an entire year's global production. More critically, 70% of silver production is a byproduct of gold, copper, lead, and zinc mining, making it impossible to expand production independently. Coupled with declining ore grades, ESG policy restrictions, and insufficient long-term investment, the supply side is virtually 'inelastic'. The demand side faces a double whammy: the demand for silver in the photovoltaic industry has surged, with its material cost share in solar cells skyrocketing from 14% to 29%, and it is expected that by 2030, photovoltaic demand will account for 40% of total silver demand; while private investment demand in China and India has exploded, with India even including silver as collateral for loans, further activating market liquidity.

The crypto market accurately captures the high elasticity characteristics of silver, giving rise to a series of innovative play styles. Some platforms have launched synthetic assets of silver mining stocks, allowing investors to bet on silver price fluctuations and mining company performance through contract trading simultaneously. The trading volume of such products surpassed $8 billion in 2025, becoming a 'favorite' for high-risk preference funds. NFT projects focused on the photovoltaic industry chain have also emerged, binding the application scenarios of silver in photovoltaic components, mining processes, and green energy returns, creating a composite subject of 'physical assets + digital rights', with a leading photovoltaic NFT project achieving a locked amount of $1.2 billion within three months of its launch. However, the volatility of silver far exceeds that of gold, and it lacks the central bank's gold purchase support, making its corresponding crypto assets even more volatile—historically, silver has plummeted 70% from its peak, and the current gold-silver ratio remains at a high of 80 (historical average 60), with both the potential for upward correction and the risk of adjustment. Deutsche Bank warns that investors participating in on-chain silver-related assets must strictly control leverage, setting a stop-loss line of 20%-30% to avoid being 'squeezed' by short-term fluctuations.

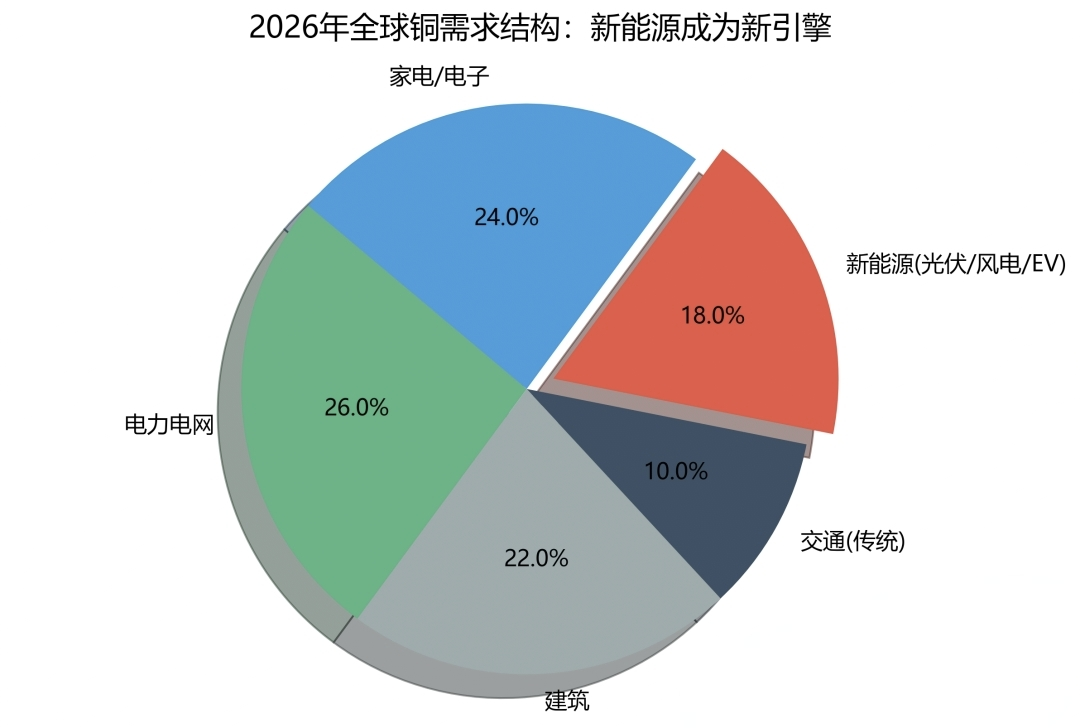

The strong price of copper marks the official arrival of the 'new oil era', while cryptocurrency provides an efficient vehicle for the value release of the copper industry. The demand side is ignited by both AI and the energy revolution: AI data centers consume three times the copper of traditional facilities, with a single large-scale project consuming up to 50,000 tons of copper; the copper used in electric vehicles is 2.9 times that of fuel vehicles, coupled with global grid upgrades to accommodate wind and solar new energy, the growth rate of copper demand is expected to reach 2.5%-3% by 2026, and S&P Global predicts that by 2040, the copper supply gap will reach 40% of global production. The bottlenecks on the supply side further amplify the gap: new copper mines take 10-15 years from exploration to production, and existing mines face multiple issues including declining ore grades in Chile, mudslides in Indonesian mining areas, and operational disruptions in Congolese copper mines, resulting in extremely low supply elasticity for copper.

Cryptocurrency's empowerment of the copper industry focuses on two core aspects: financing and asset circulation. Traditional copper mining project financing relies on bank loans and equity financing, which are cumbersome, lengthy, and have extremely high thresholds, while blockchain technology has given rise to STOs (Security Token Offerings), completely breaking this deadlock. In 2025, three South American copper mining companies raised over $1.5 billion through STOs, allowing token holders to share copper mining profits proportionally, with an annualized return rate of 18%, significantly higher than the average returns of traditional mining stocks, attracting global crypto investors to participate in mineral resource allocation. At the same time, DeFi protocols focused on the copper industry chain have emerged, launching products like 'copper price insurance' and 'mining revenue staking', helping mining companies hedge against price volatility risks while providing investors with diversified participation channels. Data shows that by early 2026, the total market value of copper-related crypto assets reached $4.5 billion, a 350% increase compared to 2024, becoming a 'certain offensive target with both growth and yield' in the eyes of institutions.

This asset frenzy spanning metals and cryptocurrency is fundamentally driven by the global economic structural reconstruction and a fundamental shift in asset pricing systems. The weakening of dollar credit has made hard assets reemerge as value anchors, while blockchain technology has broken down the liquidity barriers of traditional assets, enabling mutual empowerment of hard assets and digital assets. For investors, blindly chasing after price increases is inadvisable; precise allocation should be based on risk preferences: conservative investors can allocate gold ETFs, physical gold, or pegged tokens like PAXG and XAUT as a 'ballast' with a 5%-15% proportion, balancing safety and liquidity; stable investors can increase allocation in low-leverage copper mining ETFs and leading mining STO tokens to share in the long-term growth dividends of the industry chain; aggressive investors, when participating in silver-related crypto assets and mining NFTs, must base their involvement on a deep understanding of supply and demand fundamentals, strictly set stop-loss limits, and remain vigilant of high volatility risks.

The global asset market in 2026 represents both a concentrated release of cyclical forces and a key node of technological innovation. The robustness of gold, the elasticity of silver, and the hard-core nature of copper resonate wonderfully with the innovation, efficiency, and flexibility of cryptocurrency, together forming a new landscape for asset allocation. In the context of ongoing global uncertainty and the continuous shrinkage of the purchasing power of credit currencies, grasping the core contradiction of supply-demand imbalance, embracing the development trend of asset digitization, and adhering to long-term allocation logic are crucial to seizing opportunities in this asset repricing across cycles and fields, realizing value preservation and appreciation of assets. In the future, as blockchain technology deeply integrates with traditional mining and precious metal markets, more innovative asset forms may emerge, continuously promoting the evolution and reconstruction of the global asset allocation system.