Brothers, good evening. Azu believes that what is most lacking in the stablecoin sector today is not 'yet another faster chain,' but an infrastructure that can truly push USD stablecoins into everyday payments, cross-border settlements, and merchant collections. Plasma's approach is very straightforward—no longer let users buy Gas to transfer USD₮, then calculate fees, and suffer from congestion and failed transactions. It defines itself on its official website as a 'high-performance Layer1 born for USD₮ payments,' aiming to make money flow like internet messages: fast, certain, predictable costs, and able to directly connect with real-world payment networks and financial systems.

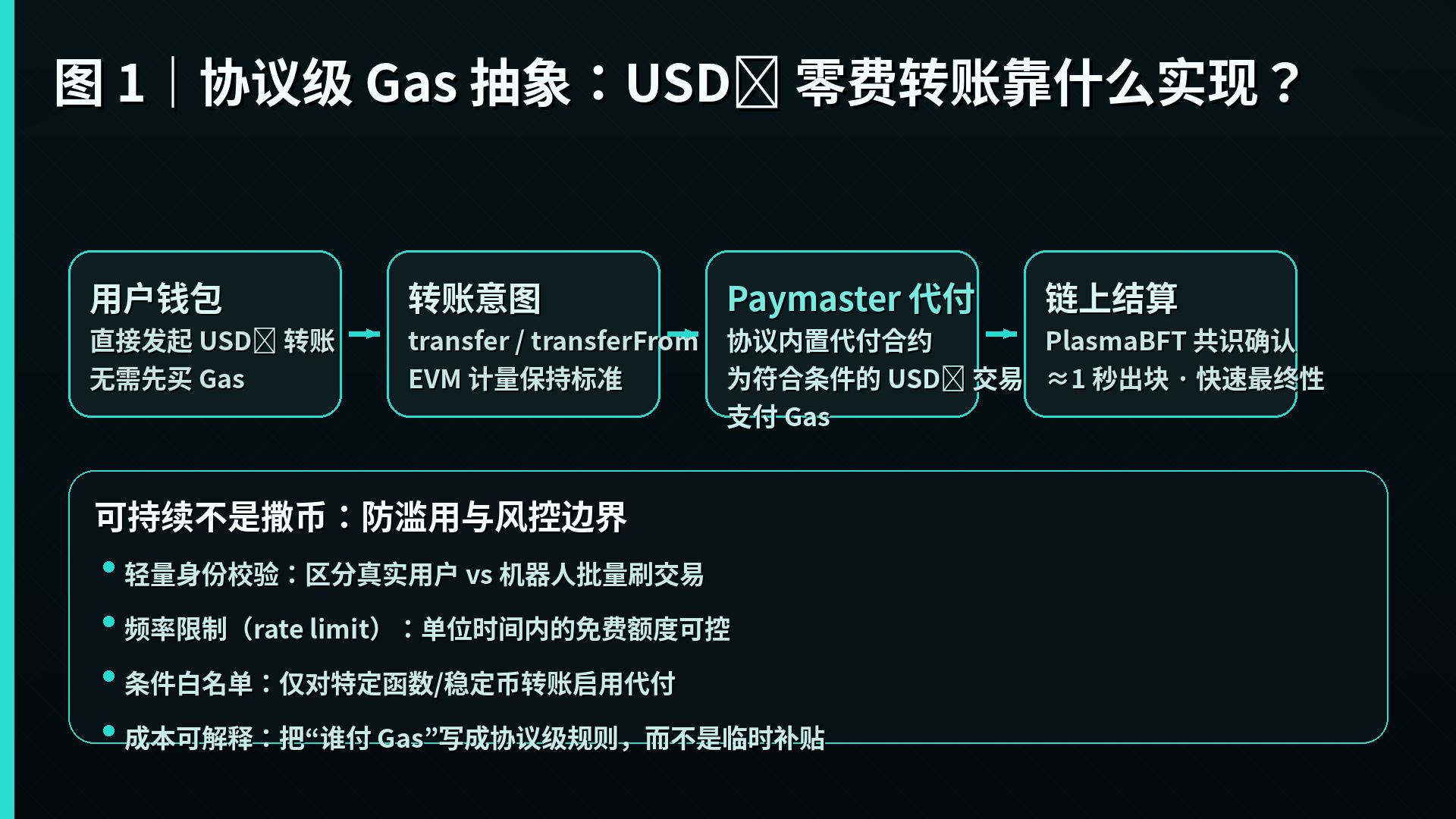

Many people instinctively think that 'zero fees' is a gimmick, but I suggest you first look at how Plasma implements it at the protocol level. Plasma still uses the standard EVM gas measurement method, so developers do not need to learn a new 'strange VM'; the logic behind the ledger execution does not need to be rewritten. The real innovation lies in making 'who pays for Gas' a protocol-level capability: there are well-maintained paymaster contracts in the network that specifically cover Gas fees for eligible USD₮ transfers (transfer/transferFrom), along with lightweight identity verification and frequency limits to ensure sustainability rather than a 'spraying coins' subsidy. You will find that this is not a 'free lunch', but a productized payment track that incorporates cost control and anti-abuse rules into the protocol. More importantly, Plasma also supports 'custom Gas tokens'—project parties can register whitelisted ERC-20 tokens (such as stablecoins or ecosystem tokens) as Gas, allowing users to interact using assets they already possess instead of being forced to hold the native coin. For applications, this is a watershed moment in UX: transforming from 'on-chain products' to a 'payment experience as usable as an app.'

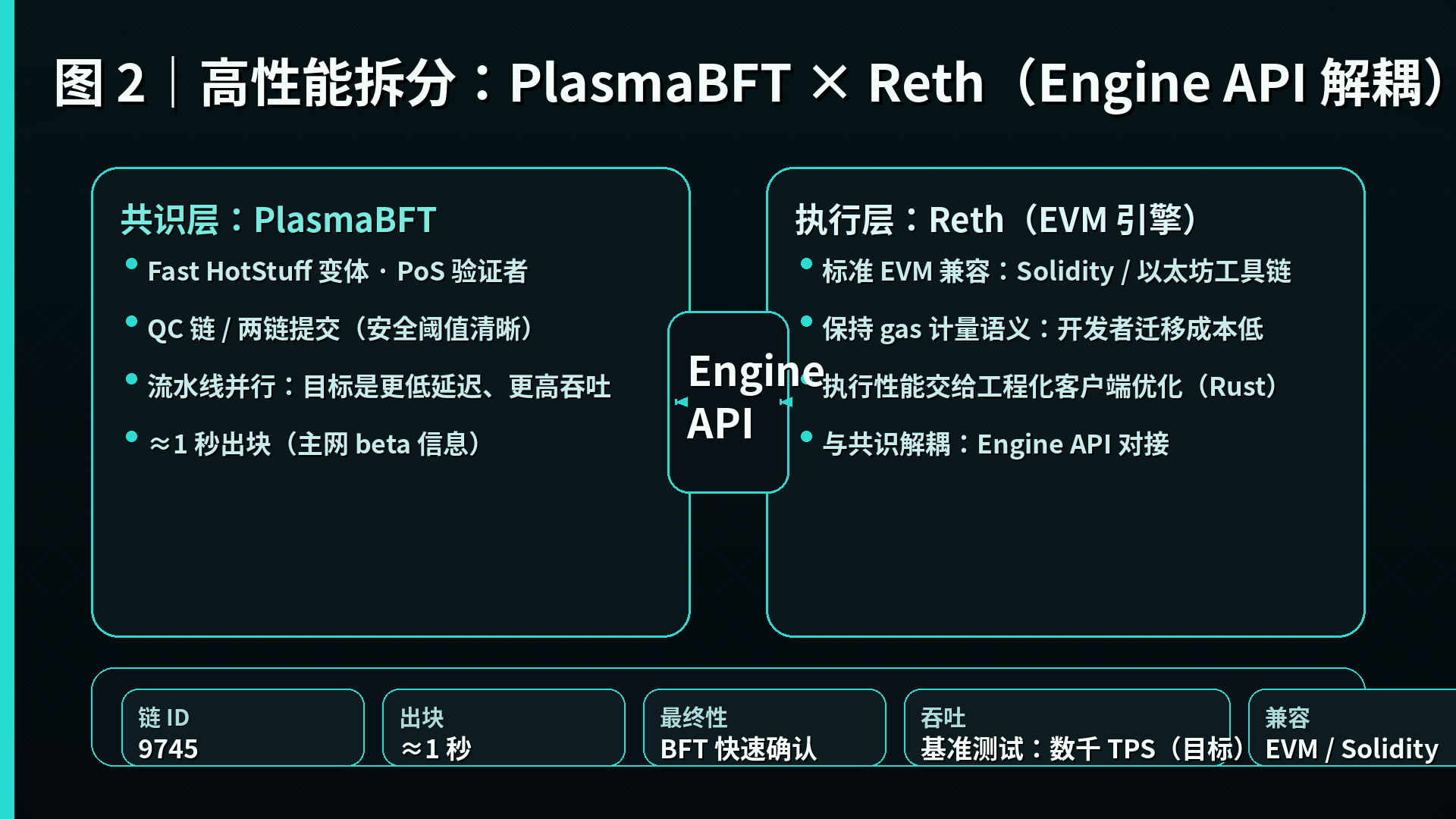

Looking deeper, Plasma adopts a 'high-performance consensus + Ethereum execution engine' split architecture: the consensus layer uses PlasmaBFT, which is a pipeline BFT implementation based on Fast HotStuff; the execution layer uses Reth (an Ethereum execution client written in Rust), and the two are decoupled through the Engine API. The advantage of this approach is very 'engineering-oriented': EVM compatibility is kept intact, performance bottlenecks are handled by the consensus pipeline, and latency and throughput are improved through parallel processing. The official documentation even clearly outlines PlasmaBFT's security threshold, QC chain, and the mechanisms of two-chain submissions, mentioning that its internal benchmark tests can achieve 'thousands of TPS' finality capability; the mainnet information also indicates the chain ID 9745, with an average block time of about 1 second, and a PoS consensus positioning variant of Fast HotStuff.

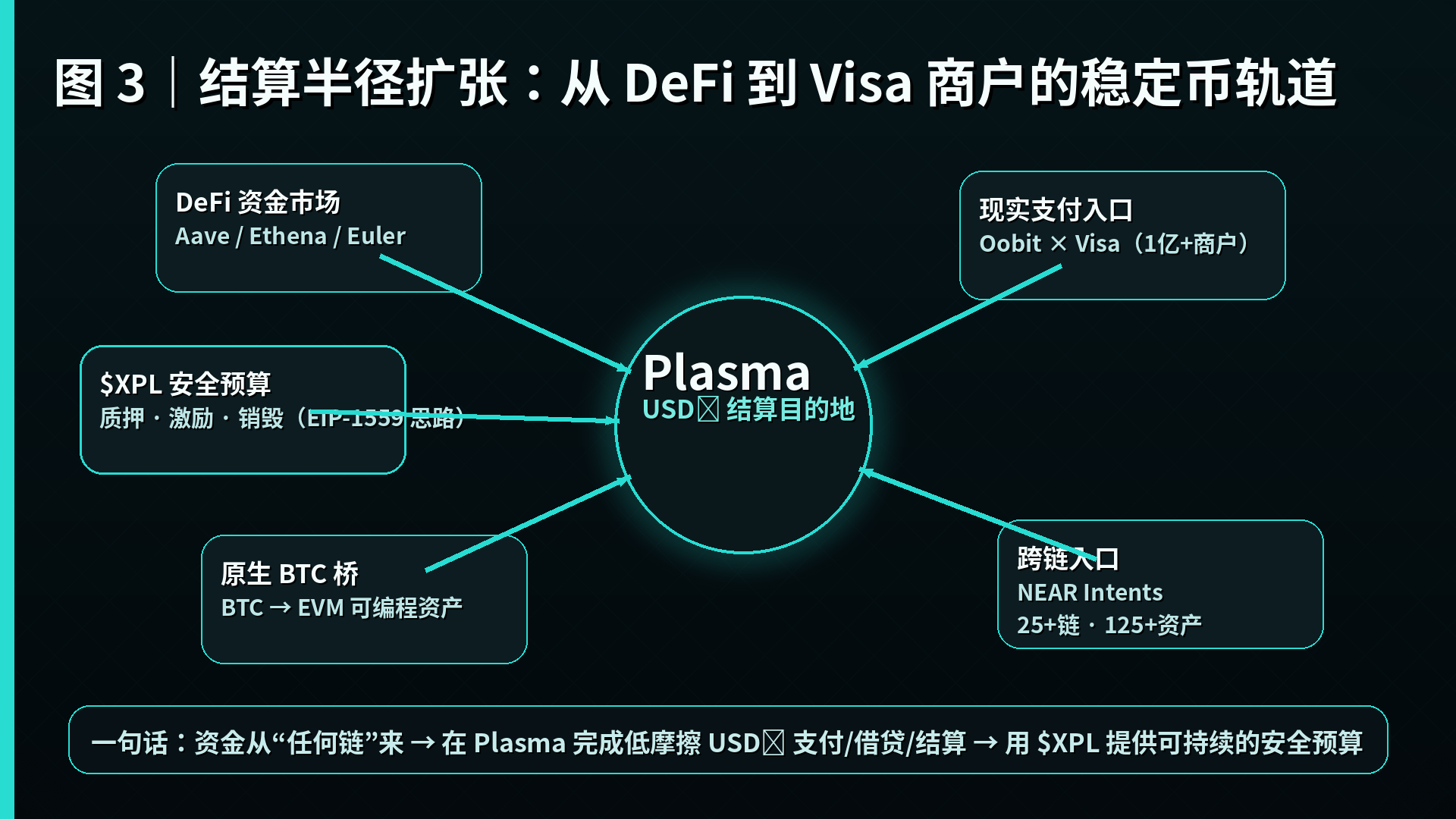

If you ask me what Plasma's most ambitious part is, I would say it is not 'faster', but 'more like financial infrastructure'. Its system overview also mentions a native, trustless Bitcoin bridge: events on the BTC chain are validated by a network of validators, bringing BTC into the EVM environment as programmable assets, rather than handing control over to a custodian. The stablecoin payment chain incorporates BTC as a top-quality collateral/value carrier into the same composable financial track, leading to possibilities such as collateral, liquidation, cross-asset liquidity, and risk control combinations aimed at institutions.

Having discussed the mechanics, let's talk about 'data'. Plasma has set a hard timeline in its mainnet beta announcement: the mainnet beta will go live on September 25, 2025, alongside the launch of the native token XPL, and emphasizes that 'there will be $2 billion in stablecoins actively on-chain on the first day'. The funds will be deployed to over 100 DeFi partners (such as Aave, Ethena, Euler, etc.), aiming for 'immediate usefulness', especially in the deep USD₮ market and with lower, more stable borrowing costs. It also disclosed a highly representative fundraising and community participation data: deposit activities promised over $1 billion in stablecoin liquidity in a short time, with public sale commitments reaching $373 million, far exceeding the limit. Do not underestimate these numbers; they indicate that Plasma initially regarded 'the settlement network must have liquidity first' as a matter of life and death.

As for whether there is real credit demand after the launch, Plasma has written a retrospective on Aave with very high information density: within 48 hours of the mainnet launch, Aave's deposit scale on Plasma reached approximately $5.9 billion, peaking at $6.6 billion in the middle of the month. Interestingly, it emphasized 'borrowing utilization rate' and 'borrowed amount'—active borrowing on Aave on Plasma reached $1.58 billion, with utilization rates for WETH and USD₮0 at around 84%, while the overall market utilization rate was approximately 42.5%, and the borrowing rate for USD₮0 has long been maintained in the range of 5–6%. This shows that the TVL display is not purely built on subsidies, but that a considerable proportion of funds are in real borrowing and strategic cycles. For cryptocurrency investors, this type of 'sustainable interest rate structure + predictable funding costs' is what can capture institutional and large-scale funds.

You might also be concerned about 'where the real-world payment applications are'. A very direct case is Oobit: it mentioned in its December 2025 announcement that it has integrated with Plasma, allowing users to use USD₮ on Plasma for consumption settlements at over 100 million Visa merchants, along with self-custodied wallets for direct payments and merchants receiving fiat currency instantly. You can understand this as: Plasma is not satisfied with just keeping the dollar stablecoin circulating in DeFi; it wants to bridge the 'last mile from wallet to cash register' and turn stablecoins into real money that can be spent.

Talking about $XPL, because this is where many people easily misjudge. Plasma's XPL documentation makes its narrative very clear: XPL is Plasma's core security asset, used for both transactions and network security, as well as for incentivizing validators; the initial supply is 10 billion tokens. In terms of distribution, 10% (1 billion) is for public sale, 40% (4 billion) is for ecosystem and growth, 25% (2.5 billion) for the team, and 25% (2.5 billion) for investors; non-US purchasers will unlock at the mainnet beta launch, while US purchasers will have a 12-month lock-up period until July 28, 2026. In terms of inflation, validator rewards start at an annualized 5%, decreasing by 0.5% each year until a long-term benchmark of 3%, and inflation will only begin after external validators and delegated staking go live. To hedge against long-term dilution, it also explicitly adopts an EIP-1559-like approach, permanently destroying base transaction fees to balance new issuance with 'growth in usage'. You will find that the logic here resembles traditional finance's 'security budget': the network must continuously pay security costs to support the settlement of stablecoin scales while controlling dilution within an understandable range.

Speaking of 'latest developments', I suggest you focus on how Plasma continues to expand its settlement radius. Around January 23, 2026, Plasma was reported to have integrated into the NEAR Intents system, allowing users to cross-chain swap between over 25 mainstream chains using more than 125 types of assets, covering core assets like XPL and USDT0. This means that Plasma does not want to become 'an isolated liquidity island for a new chain', but rather a settlement destination for stablecoins: funds can come from anywhere and settle into Plasma's payment and credit markets with lower friction. On the other hand, regarding 'payment infrastructure' itself, public information has also surfaced about the cooperation direction between Plasma One and Bridge (focusing on payment orchestration/infrastructure enhancement), which aligns with Plasma's positioning as a 'track that can be directly used by the financial system'—not just serving on-chain players, but catering to larger-scale payment and settlement needs.

Finally, I want to put it more directly: what does it mean for you? For ordinary users, the real rule change brought by Plasma is that you do not need to buy the native coin to transfer USD₮ first; the protocol-level paymaster will turn 'zero-fee transfers' into a reusable capability, but it will also prevent abuse through identity verification and frequency limits. The more you treat it as a payment track, the more you need to respect its risk control boundaries. For DeFi players, Plasma's value lies in 'a stable USD funding market + deep stablecoin liquidity'; you should not only look at TVL but also indicators that are closer to the essence of the credit market, such as borrowing utilization rates, borrowing scales, and interest rate stability. For developers, it provides EVM compatibility, an approximate 1-second block time, and Gas abstraction capabilities simultaneously, meaning you can write contracts using familiar Ethereum toolchains but create products as 'user-friendly' payment applications. For long-term investors, the key to $XPL is not 'short-term narrative fluctuations', but whether it can truly become the security budget and alignment hub for the payment settlement network as the scale of stablecoin adoption expands—this has been clearly outlined in its distribution, inflation trigger conditions, and EIP-1559-like burning design.

I won't make a call for you here, but I will provide you with a realistic judgment framework: when a chain dares to place 'zero-fee USD₮ transfers, composable credit markets, and real-world spendability' within the same product closed loop, and uses clear mechanisms and data to prove it is not just a PPT, then it deserves to be pulled out from the list of 'just another public chain' and placed in the observation pool of 'stablecoin financial infrastructure'. If you really want to follow up, keep an eye on three things: the pace at which zero-fee transfers expand from 'in-house products' to broader applications, whether the interest rate stability of Aave/credit markets can withstand volatility, and whether more real-world payment gateways (wallets/cards/merchant networks) continue to materialize.