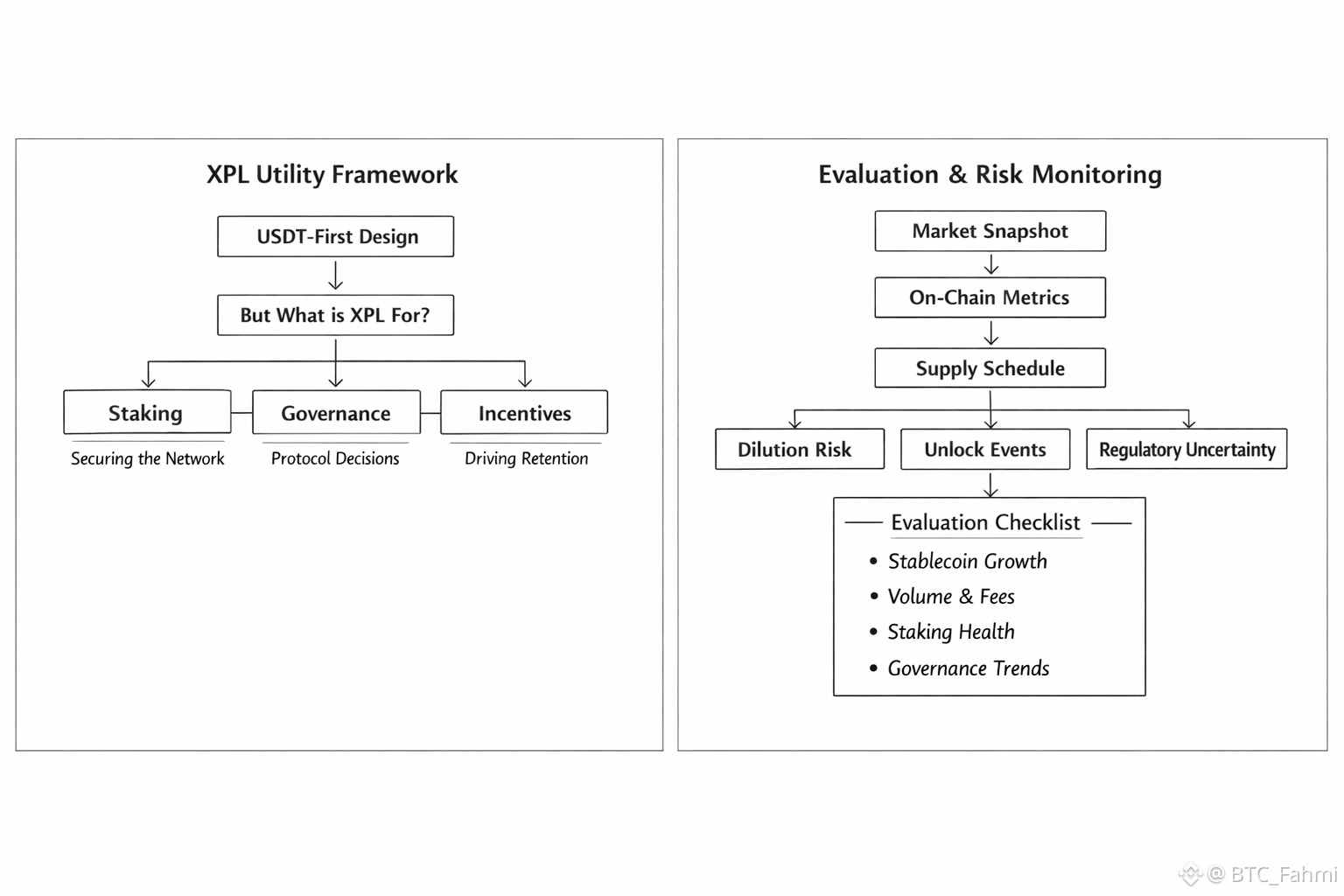

If you have ever tried to move a small amount of USDT during a busy market, you know the feeling: the transfer itself is simple, but the network makes you pay a toll that can feel out of proportion. Plasma is built around that exact pain, pushing a stablecoin first design where everyday USD₮ transfers are meant to be near instant and close to fee free, with full EVM compatibility so apps can live where the payments live.

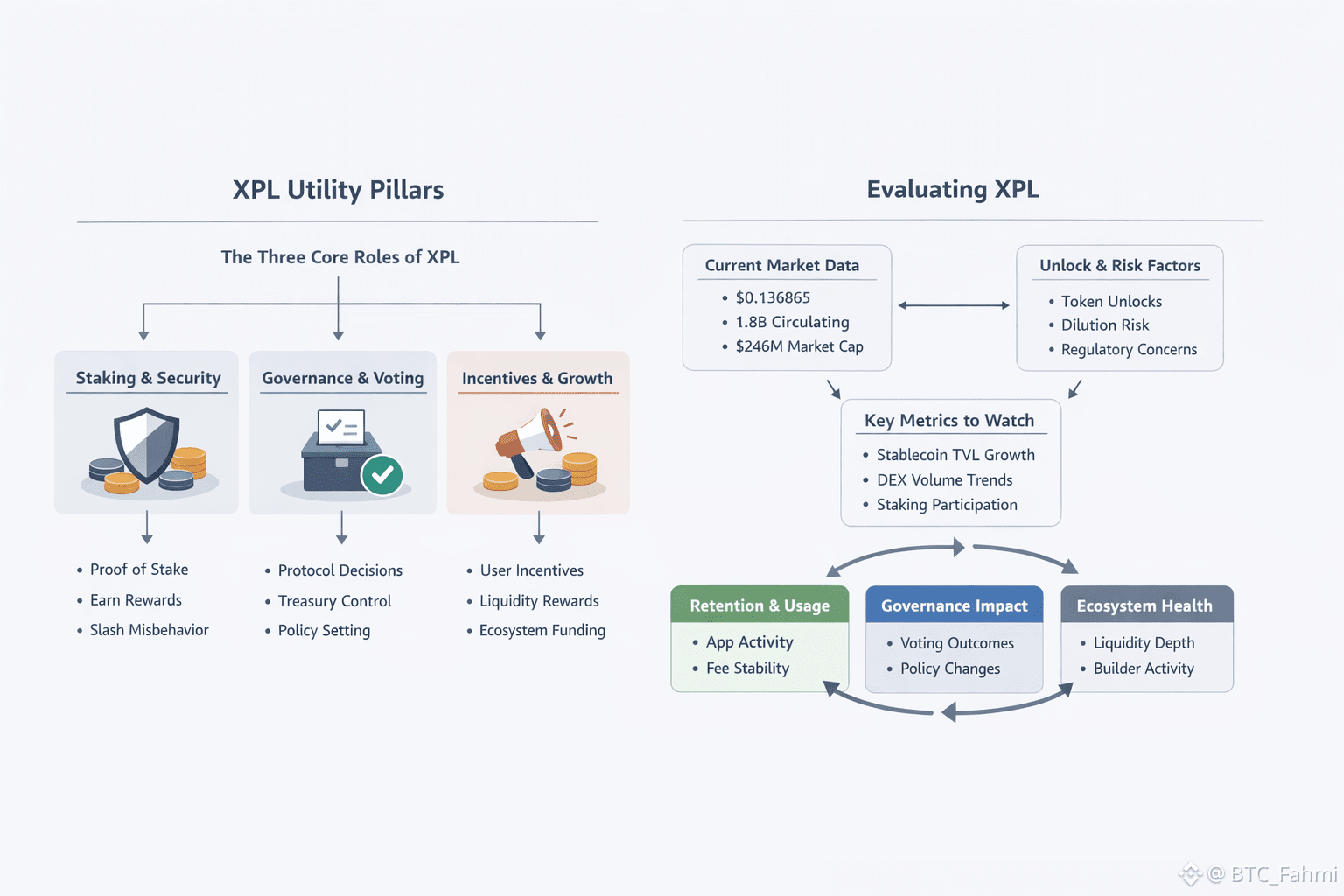

That design choice creates an immediate question for traders and investors: if basic stablecoin transfers do not require you to constantly buy the native token just to move money, what is XPL actually for? The honest answer is that XPL becomes less of a toll token and more of a control and alignment token. It is the asset that secures the network through staking, coordinates long term decisions through governance, and funds the economic incentives that decide whether Plasma becomes sticky infrastructure or a chain people try once and forget.

Start with staking, because it is the most concrete. Plasma uses a proof of stake model where validators bond XPL to participate in consensus and earn rewards. That is not abstract, it is literally how blocks keep getting produced when markets are chaotic and volume spikes. Plasma’s own FAQ also highlights a specific design nuance: misbehavior is punished through reward slashing rather than slashing staked principal, and delegation is intended to let holders earn staking rewards without running validator infrastructure. Those details matter because they change the risk profile and the likely participation rate, which feeds back into security and yield dynamics.

Governance is the second leg, and it is where “beyond gas fees” becomes most visible. Governance power is not valuable just because voting exists, it is valuable if the protocol has meaningful parameters to steer: validator policies, incentive budgets, treasury usage, and how the chain balances growth versus dilution over time. In other words, XPL is a claim on influence. That influence can be worth very little early on, then become material once real payment flows, stablecoin liquidity, and institutional integrations are large enough that small parameter changes shift outcomes.

The third leg is incentives, and this is where traders should think in terms of retention, not just APY. Crypto is full of chains that looked busy for a month because rewards were high, then went quiet when emissions rotated elsewhere. Plasma is explicitly trying to win on usability, but usability alone rarely retains users if there is no reason to keep balances and activity on the network. Incentives, whether they are paid to validators, liquidity providers, builders, or distribution campaigns, are basically Plasma’s customer acquisition budget. If that budget is spent in a way that creates habits, recurring app usage, and deep liquidity, you get retention. If it is spent in a way that creates mercenary farming, you get churn.

Now place today’s market data where it belongs: as a snapshot of what the market is pricing while this retention story is still being written. As of January 29, 2026, Binance shows XPL around $0.136865, down about 5.36% over 24 hours and up about 9.18% over 7 days, with a 24 hour range roughly $0.134 to $0.147. Market cap is shown near $246M with about $110.9M in 24 hour volume. CoinMarketCap lists total supply at 10B XPL with about 1.8B circulating, and it also anchors the drawdown context by showing an all time high around $1.68 in late September 2025.

On chain, DefiLlama shows Plasma hosting about $1.864B in stablecoins with USDT dominance around 80.88%. It also shows how early and uneven usage can be: DEX volume around $8.13M in the last 24 hours, but a steep week over week change, which is exactly what a retention problem looks like in metrics form. The same dashboard shows chain fees around $221 over 24 hours, which reinforces the core point: if the chain is designed to minimize user fees, XPL’s long term relevance leans harder on staking security, governance control, and well targeted incentive design rather than fee extraction.

One more piece traders tend to underweight is supply schedule risk, because it often arrives on a calendar rather than on a chart pattern. Plasma’s docs state that 10% of initial supply was allocated to the public sale, with non US purchasers unlocked at mainnet beta, while US purchasers are under a 12 month lockup that fully unlocks on July 28, 2026. Tokenomist also flags additional unlock cadence, listing a next unlock date of February 25, 2026, and it reports a higher unlocked supply figure than some exchange trackers, which is your reminder that circulating, unlocked, and freely tradable are not always the same number.

Risks worth pricing in

The obvious risk is that incentives fail to translate into real demand. If users can send stablecoins without touching XPL, then XPL demand must come from security participation, governance conviction, and ecosystem participation that feels necessary rather than optional. The next risk is dilution and unlock driven volatility, especially around known cliffs like July 28, 2026 for US public sale allocations. Finally there is execution and regulatory risk: stablecoin rails attract scrutiny precisely because they aim to be used at scale, and governance quality matters because poorly designed votes can turn a network into a battleground instead of infrastructure.

If you are evaluating XPL as more than a short term trade, treat it like you would evaluate a payments company, not a meme market. Watch whether stablecoin balances on Plasma keep growing whether app fees and volumes stabilize rather than spike and fade, whether staking participation looks healthy, and whether governance decisions start to matter in ways you can measure. Then read the tokenomics and vesting calendar yourself, track the next unlock dates and only size exposure in a way you can live with through volatility. The best edge here is not being early, it is being precise about whether Plasma is solving the retention problem in the real world, not just on launch week charts.

Article

Beyond Gas Fees: XPL Token’s Role in Staking, Governance, and Economic Incentives within the Plasma

Disclaimer: Includes third-party opinions. No financial advice. May include sponsored content. See T&Cs.