Entering 2026, cross-border remittances remain a 'high premium' pain point in global finance. Although the digitalization process is accelerating, the cost structure remains complex.

1. Current in-depth analysis of remittance costs

According to the latest monitoring data from the World Bank for early 2025 and 2026, the global average remittance cost still hovers around 6%, far exceeding the 3% target set by the United Nations Sustainable Development Goals (SDG).

1. Composition of costs: Where is the 'money going'?

Remittance costs are not a single fee, but rather an aggregation from multiple dimensions:

SWIFT network intermediary fees: Traditional remittances rely on an agent bank model. Each time funds pass through an intermediary bank, a wiring fee is deducted.

Exchange rate premium (FX Markup): This is the most hidden cost. The exchange rates offered by banks or remittance agencies are usually 2% - 5% different from the market midpoint, especially for non-mainstream currencies (such as certain African or Southeast Asian currencies).

Compliance and risk control costs: By 2026, global anti-money laundering (AML) and sanction screening requirements will tighten further. Financial institutions pass these compliance system and manual review costs on to users.

New taxes in 2026: It is worth noting that starting from January 1, 2026, some countries, including the United States, will begin imposing a remittance tax of about 1% on specific cross-border remittances, further increasing the total cost.

II. How does the Plasma public chain solve these problems?

In the competition of Layer 2 scaling solutions in 2026, the Plasma architecture (especially the new generation of Plasma integrated with ZK proofs, such as the XPL network) has undergone a significant technological revival. Unlike the mainstream Rollups solutions, Plasma has unique advantages in solving the 'remittance cost':

1. Extremely low 'bottom line price' (Data Availability Advantage)

Limitations of Rollups: Solutions like Arbitrum or Optimism need to return all transaction data to the Ethereum mainnet, which means their gas fees have a 'floor price' constrained by the mainnet.

Breakthrough of Plasma: Plasma only puts the 'root proof' of the computation result on-chain, keeping the vast majority of data off-chain. This allows the cost of a single transaction to be reduced to below $0.01, and even achieve zero gas fees for stablecoin transfers.

2. Native optimization of stablecoins

The Plasma network in 2026 is deeply integrated with stablecoins like Tether (USDT).

Direct settlement: Through liquidity pools of stablecoins on the Plasma chain, remittances no longer need to go through multiple intermediary banks, achieving direct peer-to-peer settlement.

Solving exchange rate losses: The remitter sends local currency from Country A (converted to stablecoin), and the recipient withdraws directly in the local area. By using decentralized exchanges (DEX) for stablecoin conversion, the cost is much lower than the bank's exchange rate markup.

3. Balancing privacy and compliance

The new generation of Plasma introduces selective disclosure privacy.

Users can remain anonymous when transferring funds (reducing the risk of data leakage), but for large remittances, Plasma can automatically generate 'compliance proof' for regulators via ZK proofs, satisfying AML requirements without exposing the user's complete wallet history, thus reducing the high regulatory fees associated with manual compliance audits.

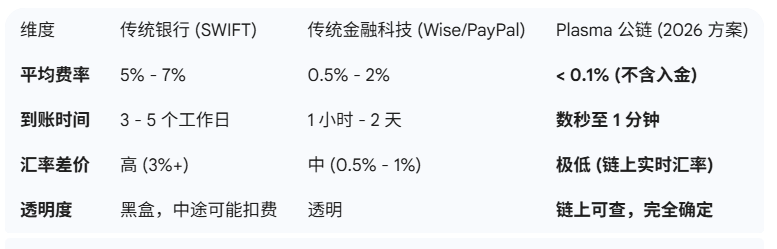

III. Comparison table of traditional vs. Plasma remittances

Summary

@Plasma The public chain significantly reduces the interaction cost of the blockchain itself through data off-chain, while utilizing stablecoins to bypass the expensive traditional intermediary networks. In 2026, if you need high-frequency, small-amount cross-border payments, the payment network based on#Plasma architecture is almost the most optimal low-cost choice available today.

$XPL