August twenty twenty five marked inflection point in stablecoin infrastructure. Circle announced Arc blockchain. Stripe revealed Tempo built with Paradigm. Google unveiled Cloud Universal Ledger targeting financial institutions. PayPal refined its approach. Established chains like Ethereum and Solana tightened stablecoin integration. The two hundred twenty five billion dollar stablecoin market suddenly had every major player building specialized payment rails. But one company already made its bet months earlier. Tether CEO Paolo Ardoino personally invested in Plasma. Bitfinex led the seed round. The world’s largest stablecoin issuer reporting fifteen billion dollars profit in twenty twenty five chose its preferred infrastructure before the arms race began.

The strategic logic differs fundamentally from other players. Circle building Arc makes sense since they control USDC and want optimal infrastructure. Stripe building Tempo aligns with their payments empire vertical integration. Google building GCUL leverages cloud platform reaching billions. These companies create infrastructure serving their existing business models. Tether took different approach. Rather than building proprietary chain, they backed independent infrastructure optimized specifically for USDT while maintaining operational separation. The relationship creates strategic advantages without operational constraints.

When Four Hundred Million People Need Dollar Access

Tether reported transaction volume increase of one hundred twenty percent in first half twenty twenty five compared to entire twenty twenty four. The growth concentrated in specific regions. Sixty six percent of new transaction volume came from West Asia, Middle East, and Africa. These aren’t speculative traders moving between exchanges. They’re exporters in Istanbul’s Grand Bazaar sourcing USDT weekly to hold earnings in currency they trust. Store owners in Buenos Aires paying staff through stablecoin rails faster than Argentinian banking system. Commodity traders in Dubai using USDT for cross-border trade. Workers globally remitting money to families using stablecoins rather than expensive traditional services.

The pattern reveals fundamental demand driving stablecoin adoption. People living in countries experiencing currency instability, capital controls, and expensive remittance systems desperately need access to dollar-denominated value. Traditional banking infrastructure either doesn’t serve them effectively or prices them out entirely. Stablecoins provide permissionless access to dollars that move at internet speed without requiring bank accounts or meeting minimum balance requirements. The one hundred fifty six billion dollars in USDT payments under one thousand dollars processed during twenty twenty five demonstrates transactional use rather than trading speculation.

Paolo Ardoino described the dynamic clearly. As emerging markets face de-dollarization pressure from China promoting gold-backed currencies and BRICS nations proposing combined currency alternatives, Tether represents the last stronghold for US dollar hegemony. Taxi drivers in Nigeria and small business owners in Argentina holding USDT have vested interest in dollar viability. The distribution creates decentralized ownership of dollar-denominated value reaching populations traditional financial infrastructure ignores. Tether becomes form of dollar diplomacy extending American soft power to regions where physical presence diminished.

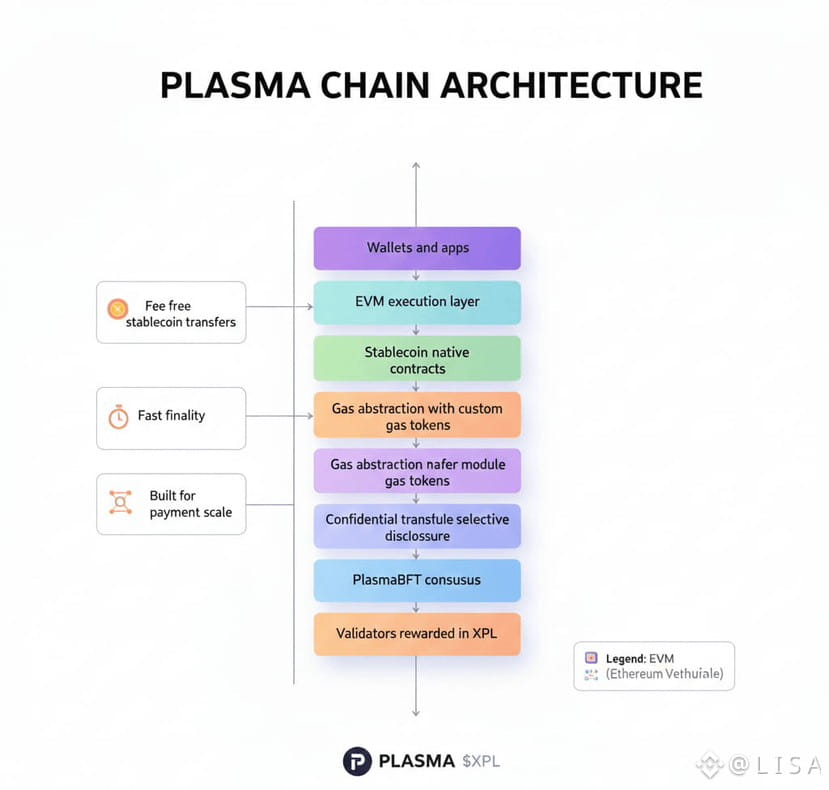

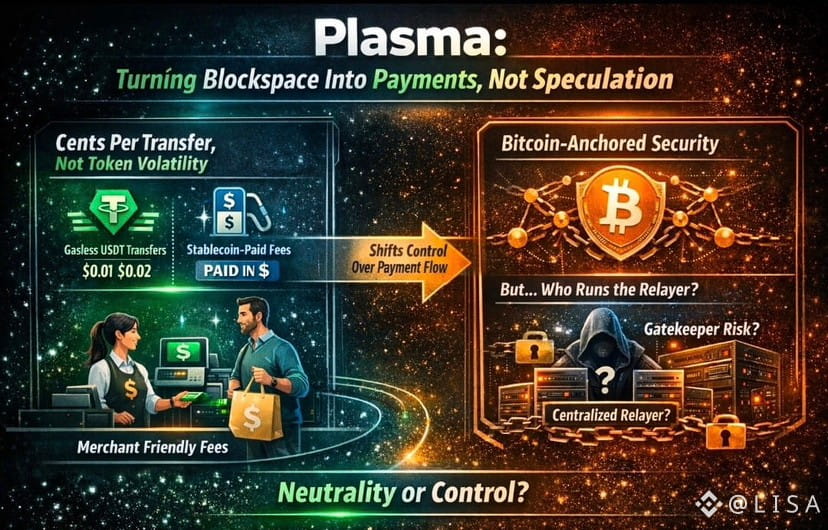

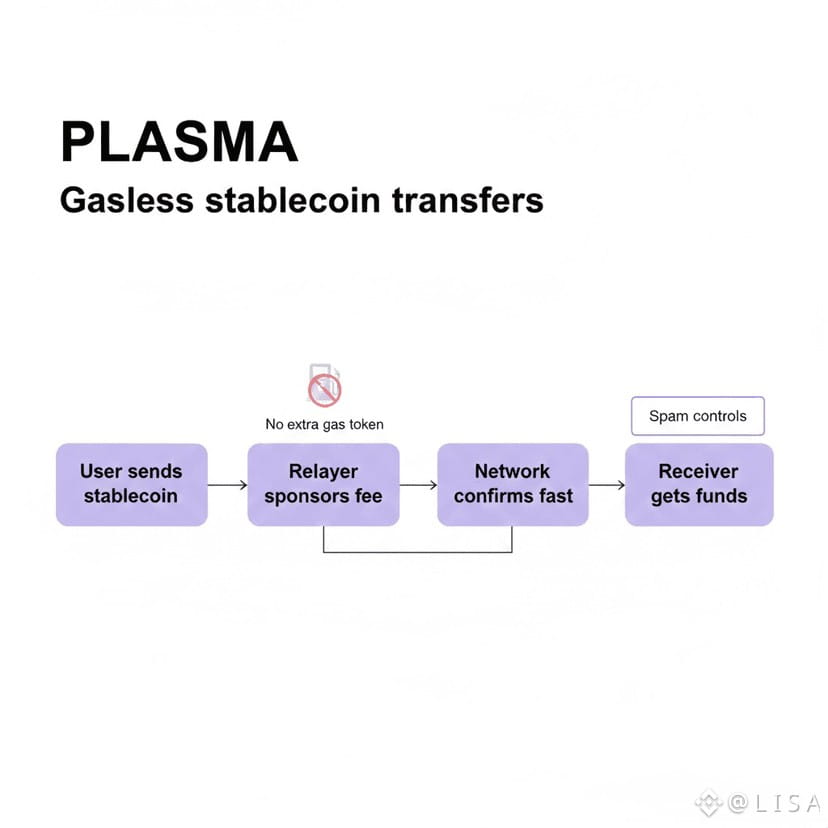

This context explains why Plasma matters strategically. With five hundred million USDT users globally and fifteen billion dollars annual profit from ninety nine percent margins, Tether needs infrastructure matching ambition scale. Ethereum remains dominant for USDT but gas fees kill micropayments. Tron offers lower costs but represents single point of dependency. Plasma provides purpose-built infrastructure optimized specifically for USDT transfers with zero fee capability and institutional grade security through Bitcoin anchoring. The relationship positions Plasma as preferred rails for moving digital dollars at scale without Tether needing to operate blockchain infrastructure directly.

Plasma One Becoming The Front Door Nobody Expected

September twenty second Plasma announced Plasma One neobank with physical and virtual debit cards working in one hundred fifty countries at one hundred fifty million merchants. Users spend directly from stablecoin balance earning ten percent yields without lockups. Four percent cashback on purchases. Zero fee USDT transfers. Fast onboarding in minutes.

The economics work through DeFi integration. Plasma launched with two billion dollars deployed across one hundred protocols including Aave, Ethena, Fluid generating yields distributed to users. Card issued by Rain using Plasma as payment backbone. Users load USDT then spend anywhere cards accepted. Everything operates in stablecoins with yield accruing until spend.

The geographic targeting reveals calculated approach. Initial focus on emerging markets showing organic stablecoin growth. Local teams establish peer-to-peer cash networks. BiLira brings Turkish lira on-ramps. Yellow Card enables African remittances. Distribution meets users where dollar access matters most. The consumer product solves blockchain’s adoption problem. People see neobank offering better yields and cashback without understanding underlying infrastructure.

When Giants Enter Stablecoin Infrastructure War

Plasma raised twenty four million February and launched September. Circle announced Arc in August. Stripe revealed Tempo September fourth. Google unveiled GCUL August twenty seventh. The stablecoin infrastructure arms race compressed into months.

Circle’s Arc centers USDC as native fuel promising fast settlement with currency exchange. Makes sense for issuer earning ninety six percent revenue from Treasury yields. But faces adoption challenge. Why would Tether use Circle’s blockchain? Competitive dynamics limit partnerships.

Stripe’s Tempo extends payments empire through vertical integration. After acquiring Bridge for one point one billion and Privy wallet, blockchain completes stack. Targets merchants through Visa, Deutsche Bank, OpenAI, Shopify relationships. Built-in AMM lets users pay gas with any stablecoin. But will competitors use Stripe-controlled infrastructure?

Google’s GCUL positions as neutral infrastructure layer. Python-based contracts accessible to finance developers. CME Group completed testing with twenty twenty six launch. Leverages cloud platform reaching billions. Targets institutional market.

Established chains defend territory. Ethereum dominates with sixty eight percent DeFi value locked. Tron cut energy costs sixty percent reducing USDT fees from four dollars to under two acknowledging Plasma threat. Solana grows fastest alternative ecosystem. The proliferation creates fragmented landscape. Multiple specialized chains, general purpose optimization, payment company extensions, tech giant infrastructure all competing for twenty seven point six trillion annual stablecoin volume.

Whether Distribution Matters More Than Technology

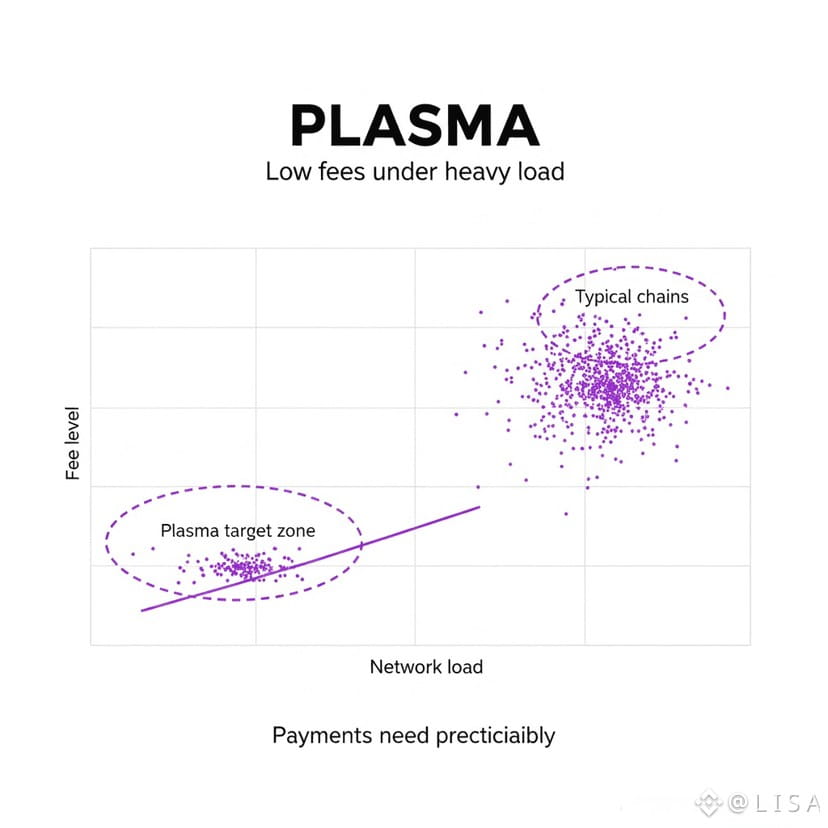

Plasma faces adoption reality despite technical excellence. PlasmaBFT consensus achieves thousands of transactions per second with sub-second finality. Reth execution layer provides full EVM compatibility. Bitcoin anchoring delivers institutional security guarantees. Protocol level paymaster enables zero fee USDT transfers. The architecture works. But technology rarely determines winner in infrastructure competition. Distribution determines winner.

Circle brings USDC with sixty five billion dollars circulation and institutional relationships throughout traditional finance. Stripe processes one point four trillion dollars annual merchant volume with existing payment infrastructure. Google reaches billions through cloud platform with hundreds of institutional partners. Ethereum hosts established DeFi ecosystem with years of battle-tested infrastructure. Tron controls significant USDT volume through low cost transfers. Each competitor possesses distribution advantage Plasma lacks.

Plasma’s counter-strategy relies on consumer product creating organic adoption. If Plasma One gains traction in emerging markets where stablecoin demand highest, retail payment volume follows. Four percent cashback and ten percent yields attract users. Zero fee transfers provide utility. Physical cards enable spending anywhere. The application becomes reason to use infrastructure rather than infrastructure searching for application. Success depends on converting waitlist into actual users then scaling across one hundred fifty countries.

The Tether relationship provides strategic edge others cannot replicate. As USDT continues rapid growth particularly in West Asia, Middle East, and Africa, Plasma positioned as preferred infrastructure. Paolo Ardoino’s personal investment signals confidence beyond typical blockchain partnerships. Bitfinex leading funding rounds connects Plasma to broader Tether ecosystem. The alignment creates natural distribution channel if Plasma proves infrastructure scales reliably. Tether earning fifteen billion dollars annually can afford supporting preferred payment rails permanently if strategic value justifies cost.

The geographic focus targets markets where need greatest. Emerging markets experiencing currency instability desperately need dollar access. Traditional infrastructure serves them poorly. Stablecoin adoption already shows organic growth. Plasma One designed specifically for these users rather than wealthy markets with functioning banks. Local teams understand regional challenges. Partnerships address specific onboarding barriers. The approach prioritizes solving real problems for underserved populations rather than competing directly with established players in mature markets.

The Test Nobody Can Avoid

The fundamental question facing all stablecoin infrastructure projects is whether specialized payment rails can capture meaningful share from general purpose chains or remain niche solutions. Ethereum and Tron dominate current stablecoin volume through years establishing network effects. Developers understand tooling. Users trust security. Liquidity concentrates on proven infrastructure. Displacing incumbents requires compelling advantage justifying switching costs.

Plasma’s advantage thesis combines multiple elements. Zero fee USDT transfers eliminate friction for micropayments and remittances. Bitcoin anchored security provides institutional confidence. EVM compatibility enables familiar developer experience. Tether relationship creates strategic alignment with largest stablecoin issuer. Plasma One offers consumer application addressing adoption barriers. The combination targets specific use cases where established chains underserve users rather than competing broadly across all dimensions.

The competition intensifies rather than consolidates. More specialized stablecoin chains launch monthly. Established chains improve stablecoin features. Traditional payment companies extend into blockchain. Tech giants build institutional infrastructure. Regulatory clarity particularly through US GENIUS Act and EU MiCA creates framework enabling compliant stablecoin operations. The market opportunity grows large enough supporting multiple successful participants rather than winner-take-all outcome.

We’re watching transformation of global payment infrastructure. Stablecoins processed twenty seven point six trillion dollars in twenty twenty five exceeding combined Visa and Mastercard volume. The infrastructure supporting this activity determines who captures value from digital dollar movement. Whether specialized chains optimized for specific use cases or general purpose platforms supporting diverse applications better serve this market remains open question. The answer determines whether Plasma’s focused approach or competitor’s broader strategies win market share.

The consumer test arrives through Plasma One adoption. Can neobank designed specifically for stablecoin users gain traction in emerging markets? Will four percent cashback and ten percent yields attract retail adoption? Does zero fee transfer utility drive sustained usage? The application success determines whether Plasma converts technical infrastructure into actual payment volume. Infrastructure without users remains expensive science experiment. Users without friction point toward infrastructure capturing real adoption.

The strategic bet Tether placed on Plasma reflects conviction that purpose-built infrastructure optimized specifically for USDT movement at scale matters more than retrofitting general purpose chains. Whether this conviction proves correct determines if Plasma becomes preferred global payment rails for digital dollars or specialized solution serving niche markets. The answer shapes how hundreds of millions of people access dollar-denominated value in economies where traditional banking fails them. That outcome matters beyond typical blockchain competition.