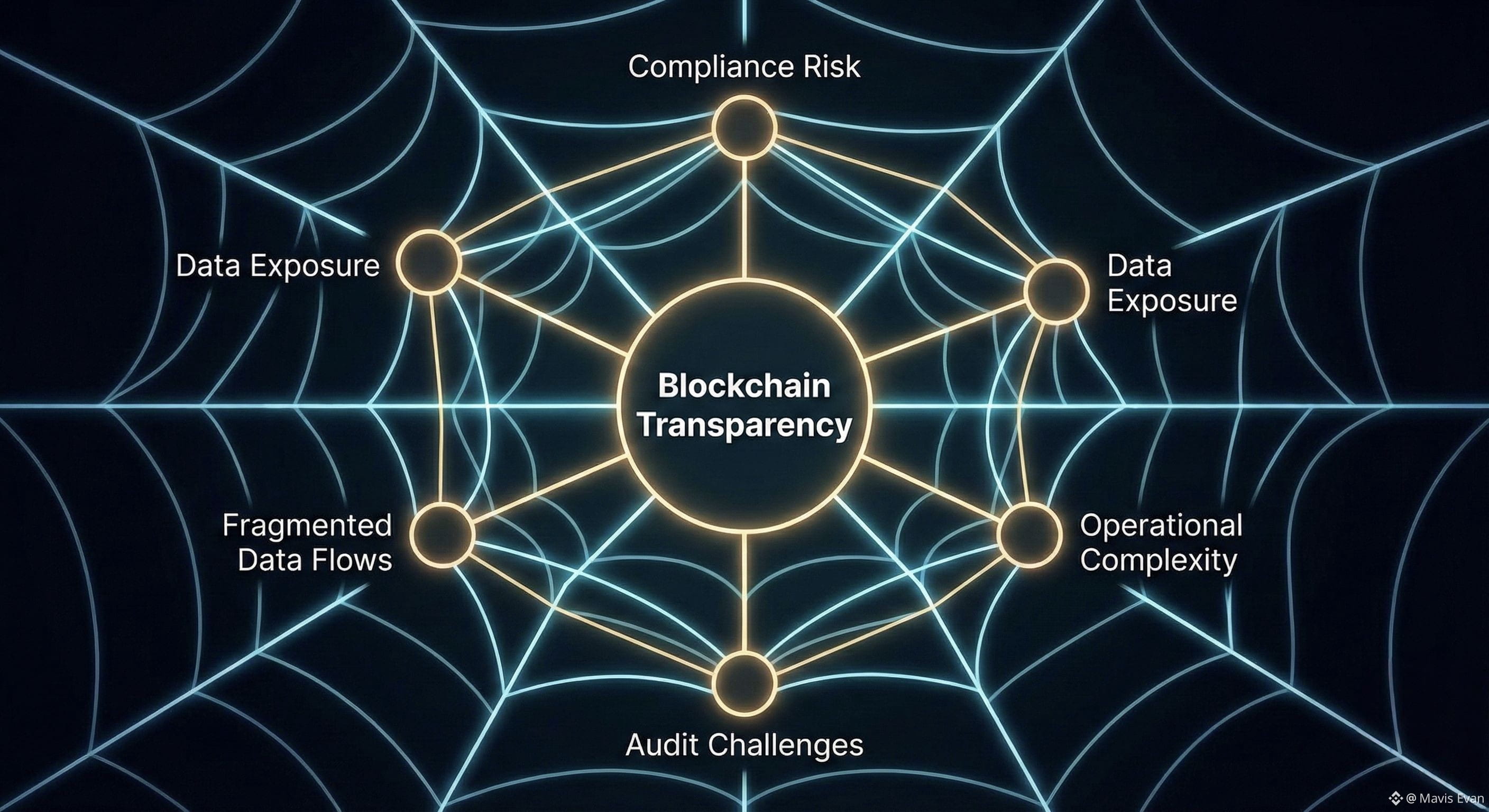

Long before blockchain entered mainstream financial discussion, regulated markets were already grappling with a difficult balancing act. Financial systems must be transparent enough to satisfy regulators, auditors, and counterparties, while remaining private enough to protect sensitive positions, identities, and strategies. Traditional infrastructure solves this tension through legal boundaries, controlled disclosure, and trusted intermediaries. Public blockchains, by contrast, default to radical transparency. Every transaction, balance change, and interaction is globally visible and permanently recorded. This design works well for open networks and censorship resistance, but it breaks down when applied to regulated finance, where confidentiality is not optional and mistakes carry legal and reputational consequences.

In practice, most blockchains ask institutions to compromise. Either they accept full transparency and attempt to manage privacy off-chain, or they rely on complex add-ons that obscure data without integrating cleanly into compliance and audit processes. These approaches tend to create operational risk rather than reduce it. Privacy layers bolted onto transparent systems often complicate audits, fragment data flows, and introduce trust assumptions that undermine the original promise of decentralization. As a result, many financial institutions remain unable to deploy meaningful value on-chain beyond limited pilots or synthetic representations.

Dusk Network was designed as a response to this structural gap rather than an attempt to overturn existing financial logic. Its starting assumption is that regulated finance will not adapt itself to blockchains that ignore confidentiality, accountability, and legal constraints. Instead, blockchain infrastructure must adapt to the realities of how financial systems already operate. Dusk approaches this not as an ideological stance on privacy or decentralization, but as an engineering and governance problem shaped by real-world incentives and obligations.

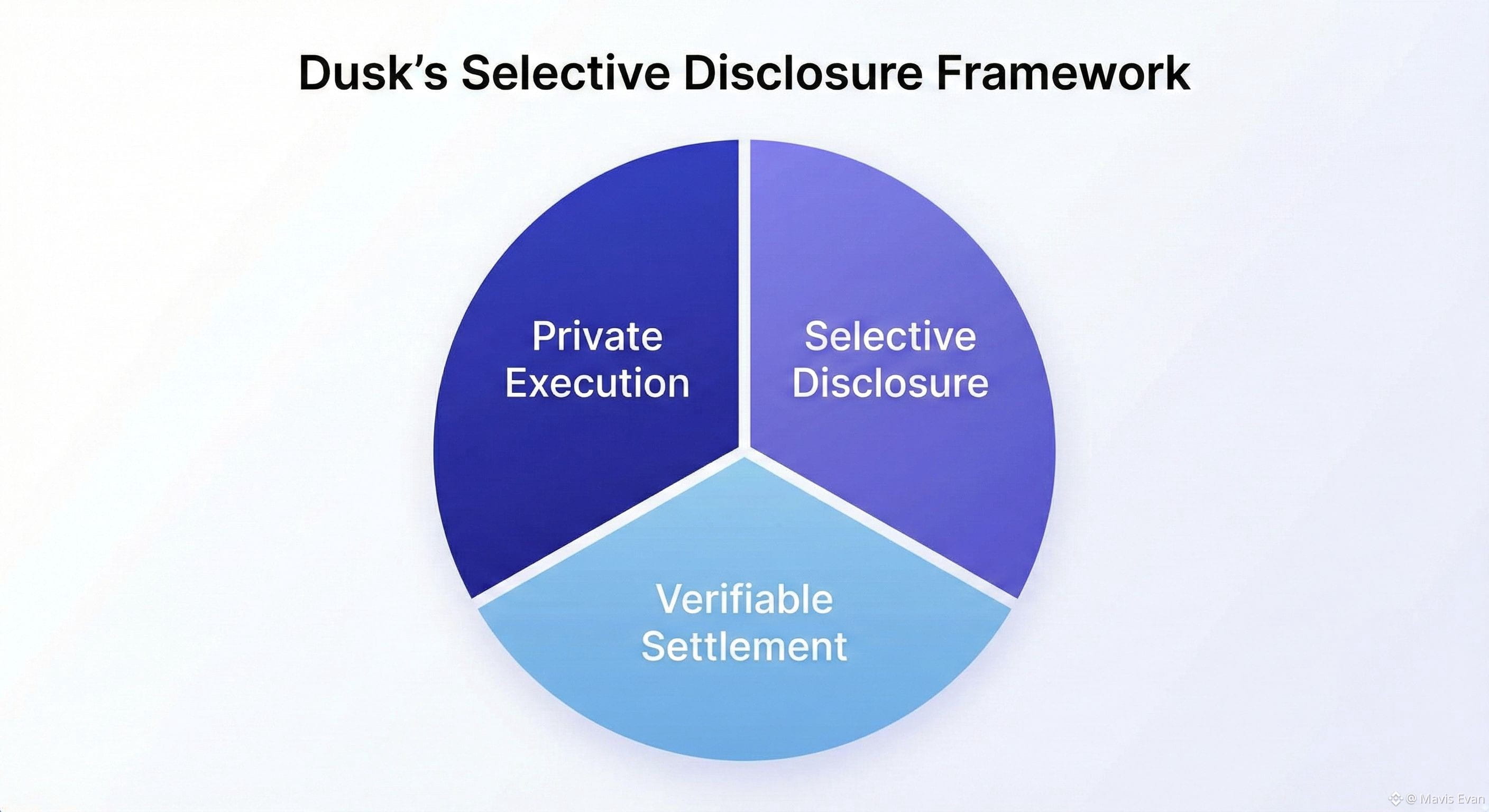

At a conceptual level, Dusk’s architecture is built around selective disclosure. Rather than exposing all transaction data to all participants, the system allows information to be shared only with the parties that need to see it, while still enabling the network to verify that rules have been followed. This distinction matters in practice. Financial institutions do not need secrecy for its own sake. They need assurance that sensitive data remains confidential, while regulators and auditors retain the ability to verify compliance. Dusk’s design accepts the tension between these requirements and treats it as a core architectural constraint rather than an afterthought.

The modular structure of the network reflects this pragmatism. Execution, privacy, and settlement are treated as distinct but coordinated functions. This separation allows financial applications to evolve without forcing all participants into the same risk profile. For example, an issuer of tokenized securities can define how ownership data is disclosed, how transfers are validated, and how compliance checks are enforced, without exposing proprietary information to unrelated network users. The blockchain provides shared guarantees around correctness and finality, while application-level logic governs who can see what, and when.

Consider a regulated entity issuing tokenized equity to a limited group of investors. The issuer must maintain an accurate cap table, enforce transfer restrictions, and produce auditable records for regulators. On most public blockchains, this would either expose investor identities and positions or require off-chain registries that weaken on-chain guarantees. On Dusk, the issuance and lifecycle of the asset can remain on-chain, with ownership and transaction details disclosed only to authorized parties. Auditors can verify compliance without relying on opaque intermediaries, and regulators can be granted access without turning the asset into a public dataset.

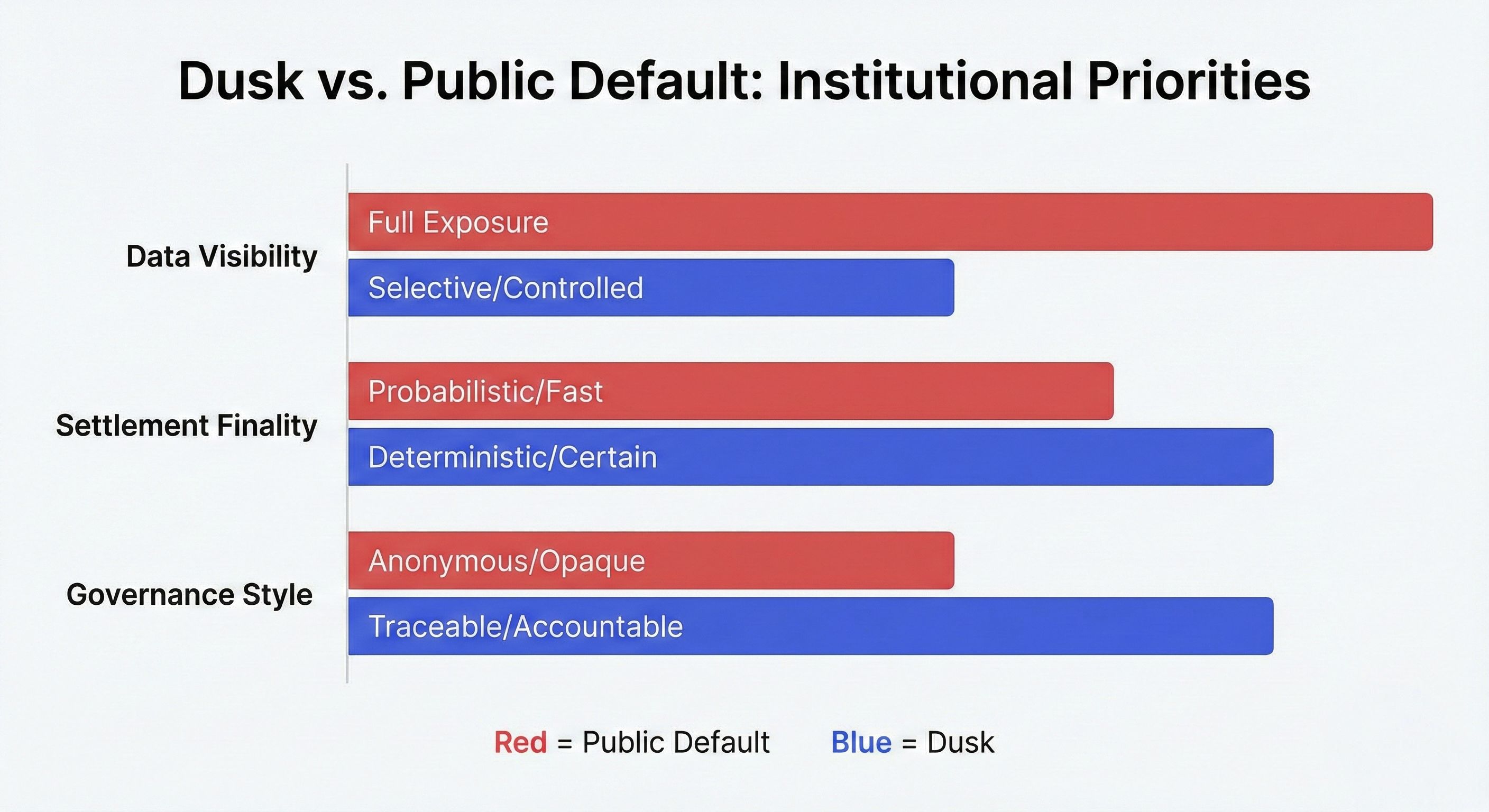

Settlement processes benefit from similar design choices. In traditional finance, settlement finality is meaningful only if it aligns with legal ownership and reporting standards. Dusk’s approach emphasizes deterministic execution and verifiable outcomes over raw throughput. This makes the system slower in some dimensions than highly optimized public chains, but more predictable in contexts where reversibility, disputes, and compliance obligations matter more than speed alone. These trade-offs reflect an understanding that institutional users value certainty and accountability over maximal performance.

Governance on Dusk follows the same logic. Rather than assuming that all governance activity should be public and anonymous, the network supports structures that resemble formal decision-making environments. This allows protocol evolution to take place in a way that mirrors how regulated systems manage change: through traceable decisions, accountable participants, and controlled disclosure. The goal is not to eliminate decentralization, but to shape it so that it remains compatible with long-term institutional participation.

The DUSK token plays a functional role within this framework. It is used to pay for network operations, secure consensus, and coordinate incentives among validators and participants. Its purpose is to sustain the economic integrity of the network, ensuring that those who maintain it are aligned with its reliability and correctness. The token is not positioned as a speculative vehicle, but as an internal mechanism that supports predictable network behavior.

In the broader evolution of blockchain infrastructure, Dusk occupies a position that prioritizes durability over novelty. As financial markets explore tokenization, on-chain settlement, and programmable compliance, the systems that endure will be those that integrate smoothly with existing legal and institutional frameworks. Dusk does not promise to replace traditional finance or abstract away its complexities. Instead, it acknowledges those complexities and builds around them, offering infrastructure that aligns with how regulated finance actually functions. In doing so, it contributes to a quieter but more consequential shift: moving blockchain from experimentation toward infrastructure that can be used responsibly at scale.