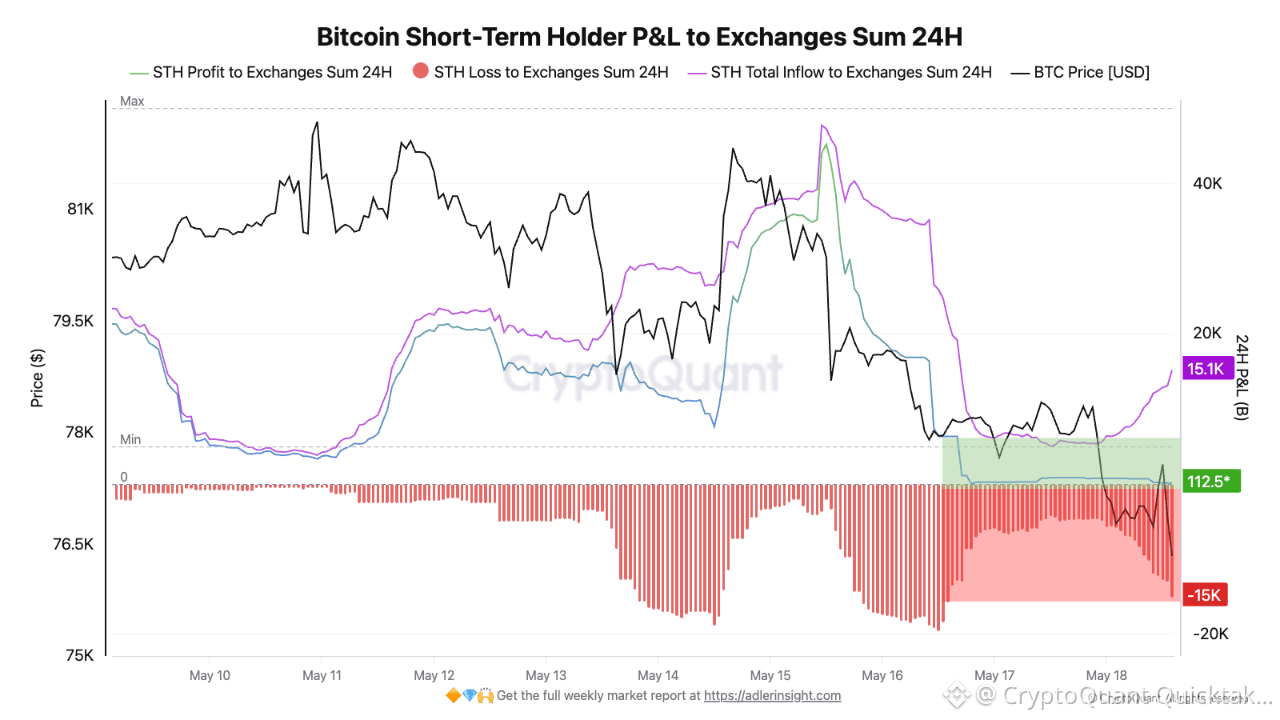

The recent Bitcoin decline between May 16 and May 18 reveals an important behavioral split inside the short-term holder cohort.

The metric “Bitcoin Short-Term Holder P&L to Exchanges Sum 24H” tracks whether short-term holders are sending coins to exchanges while sitting on unrealized profits or unrealized losses.

In other words, it helps separate two very different types of sell-side behavior: voluntary profit-taking versus forced or emotional loss realization.

What stands out in the latest move is the extreme imbalance between profitable and loss-making short-term holder flows.

As of the latest reading, short-term holders in profit sent only ~112 BTC to exchanges over the last 24 hours. In practical terms, that is almost irrelevant compared with the scale of loss-driven activity. During the same window, short-term holders in loss sent roughly 15,000 BTC to exchanges, while total STH exchange inflows also stood near 15,100 BTC.

That means that almost the entire short-term holder inflow came from coins being moved at a loss. Profit-taking represented less than 1% of total STH exchange inflows, while loss realization accounted for virtually the whole flow.

This is the key analytical signal.

The recent BTC decline does not appear to be driven by short-term holders locking in gains. Instead, it looks like a capitulation-style reaction from underwater investors. Those who were still in profit largely stayed inactive, while those whose positions moved into red territory became the dominant source of exchange supply.

So the current structure suggests a classic weak-hand flush: price falls, recent buyers lose confidence, loss-making coins move to exchanges, and the market absorbs forced sell-side liquidity.

The question now is whether this ~15K BTC loss-driven inflow fades quickly, which would support the idea of a short-term reset, or continues expanding, which would imply that impatient capital is still being pushed out of the market.

Written by MorenoDV_