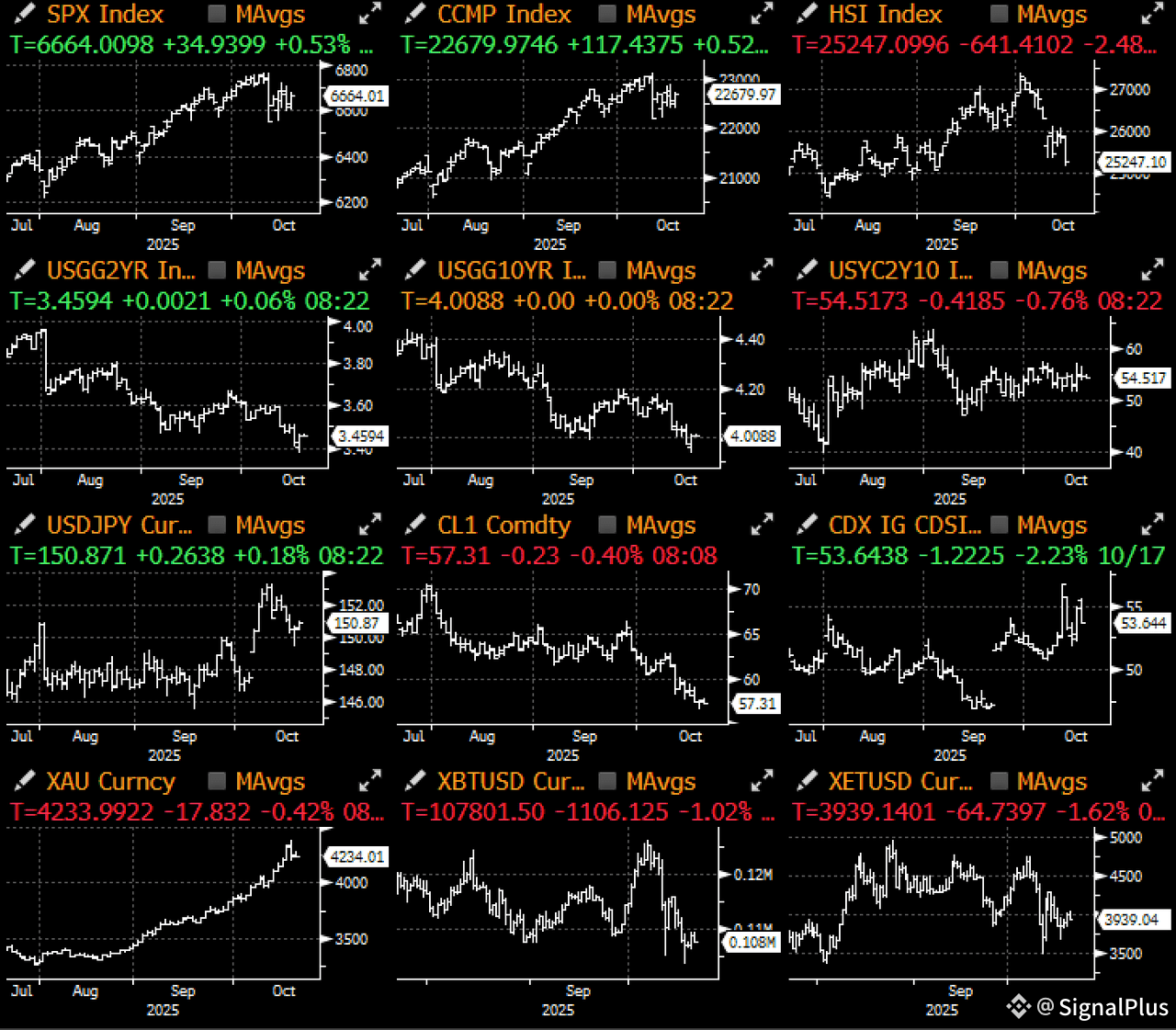

Macro ended a tumultuous week on a strong note, with yet another ‘TACO’ from President as he publicly admitted that high tariffs on China are not “sustainable” and that he will indeed meet President Xi in two weeks as telegraphed by Treasury Bessent and his team.

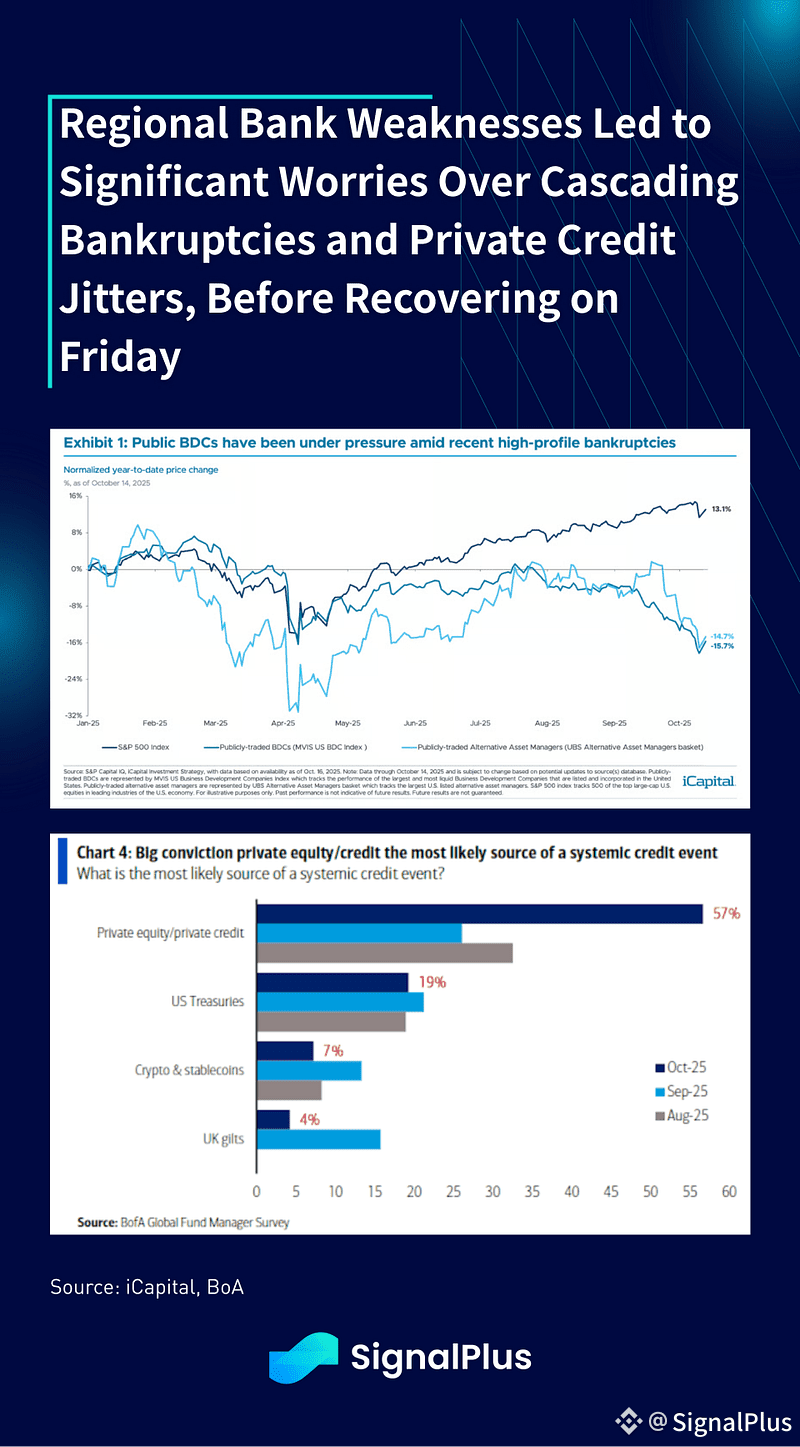

Furthermore, yet another quarter of stronger than expected results for bank earnings helped calm some of the private credit worries from the First Brands bankruptcy and the subprime auto lender write off (Tricolor, $170M charge-off), even despite Jamie Dimon ominiously stating that “And I probably shouldn’t say this, but when you see one cockroach, there are probably more. And so we should — everyone should be forewarned on this one.”, with regards to more credit defaults down the line.

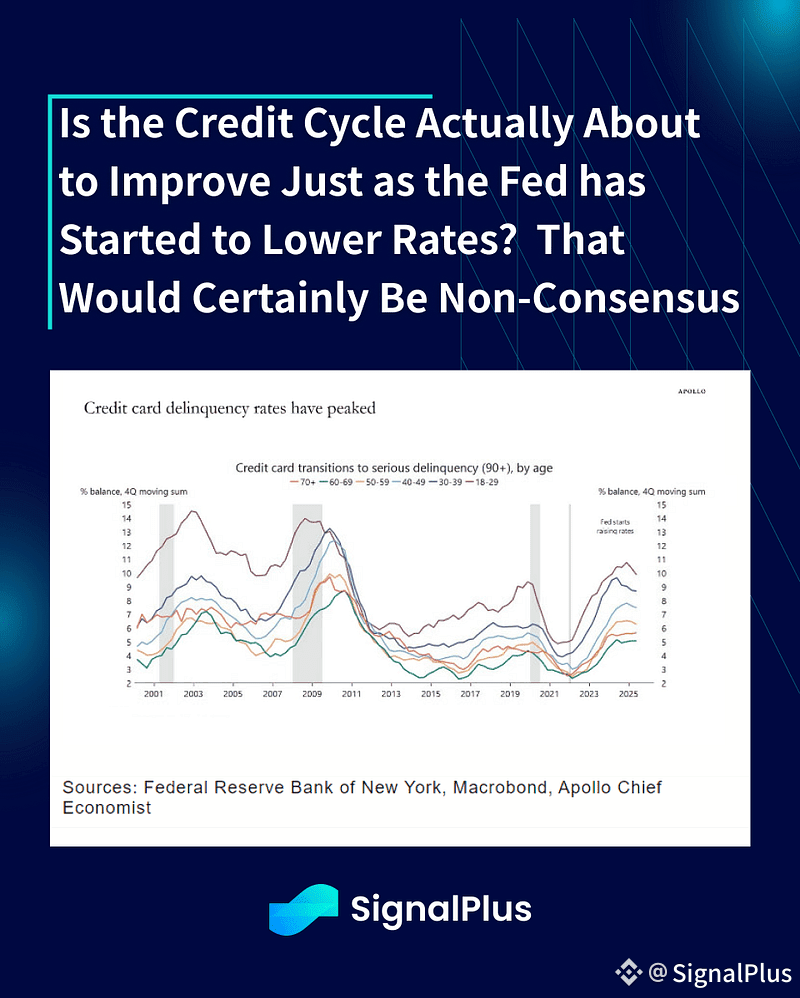

On the flip-side, high velocity credit card data was actually better in Q3 based on Wall Street reports, with analysts reporting a further acceleration in Q3 consumer spending based JPM data reporting +9%, Citi at +4%, and Wells Faro at +6.3%, all above their Q2 pace.

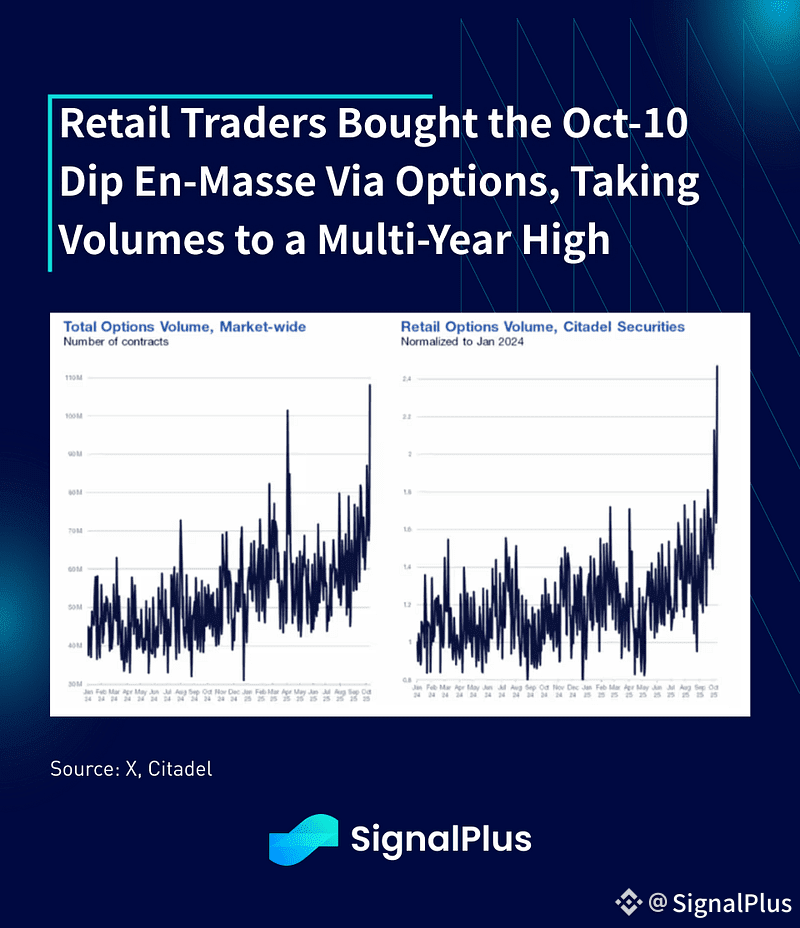

Furthermore, recently released data shows retail buyers being extremely aggressive in buying the equity dip from two Friday ago, as option volumes exploded to the highest levels in 2 years with traders betting on a USA-China descalation, which has worked brilliantly against for the 2nd time in a row. Will we get a 3rd crack on the TACO trade?

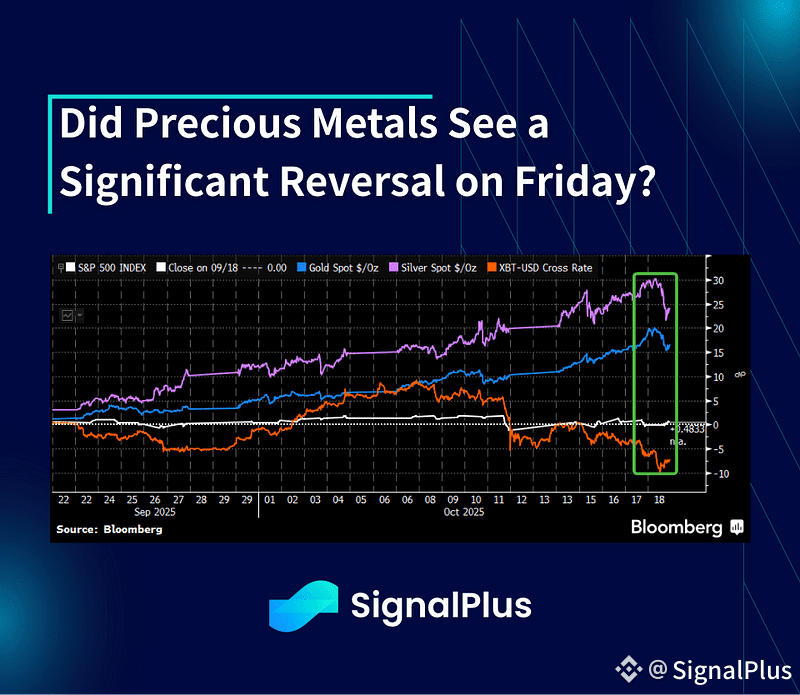

While equities and credit markets largely calmed down on Friday, precious metals fell by the most in 6 months (Silver -5%), showing the 1st signs of weakness after a record setting run. Significant profit-taking and VaR de-risking flows likely drove some of the selling flow, with traders likely focusing on PNL protection as geopolitical headline risks continue to add volatility to safe-haven assets.

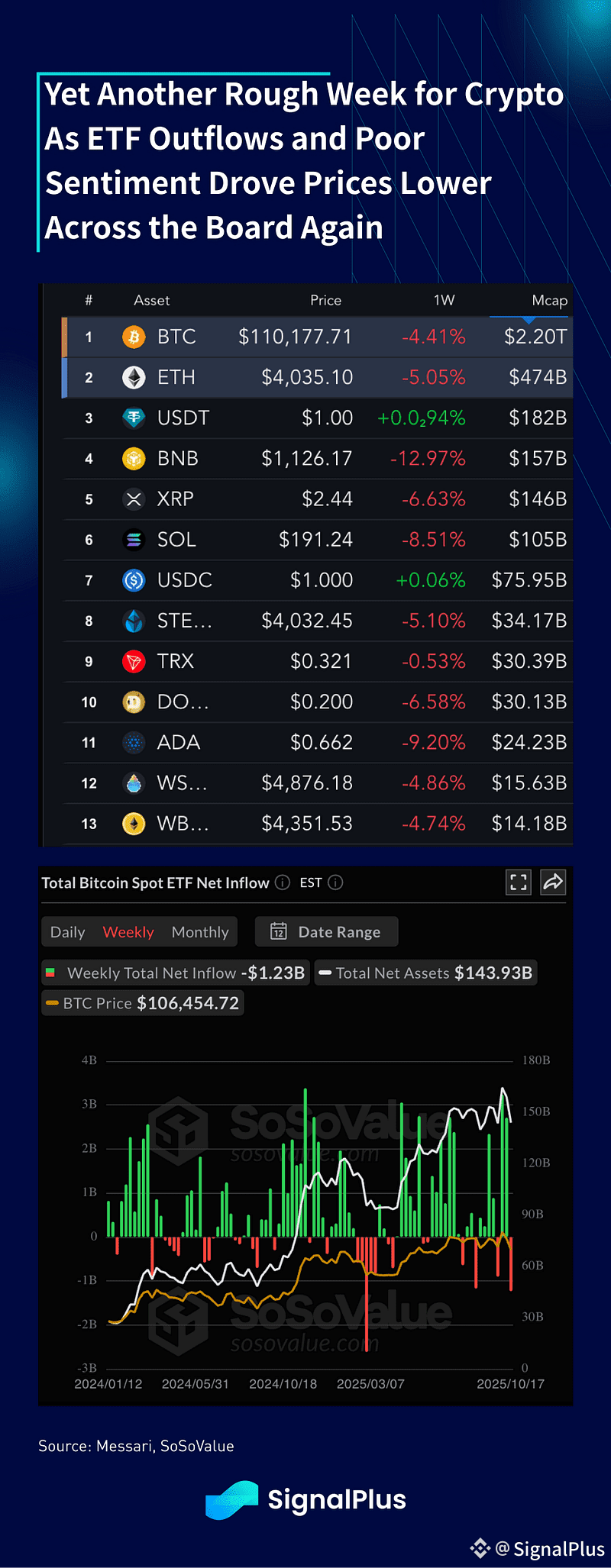

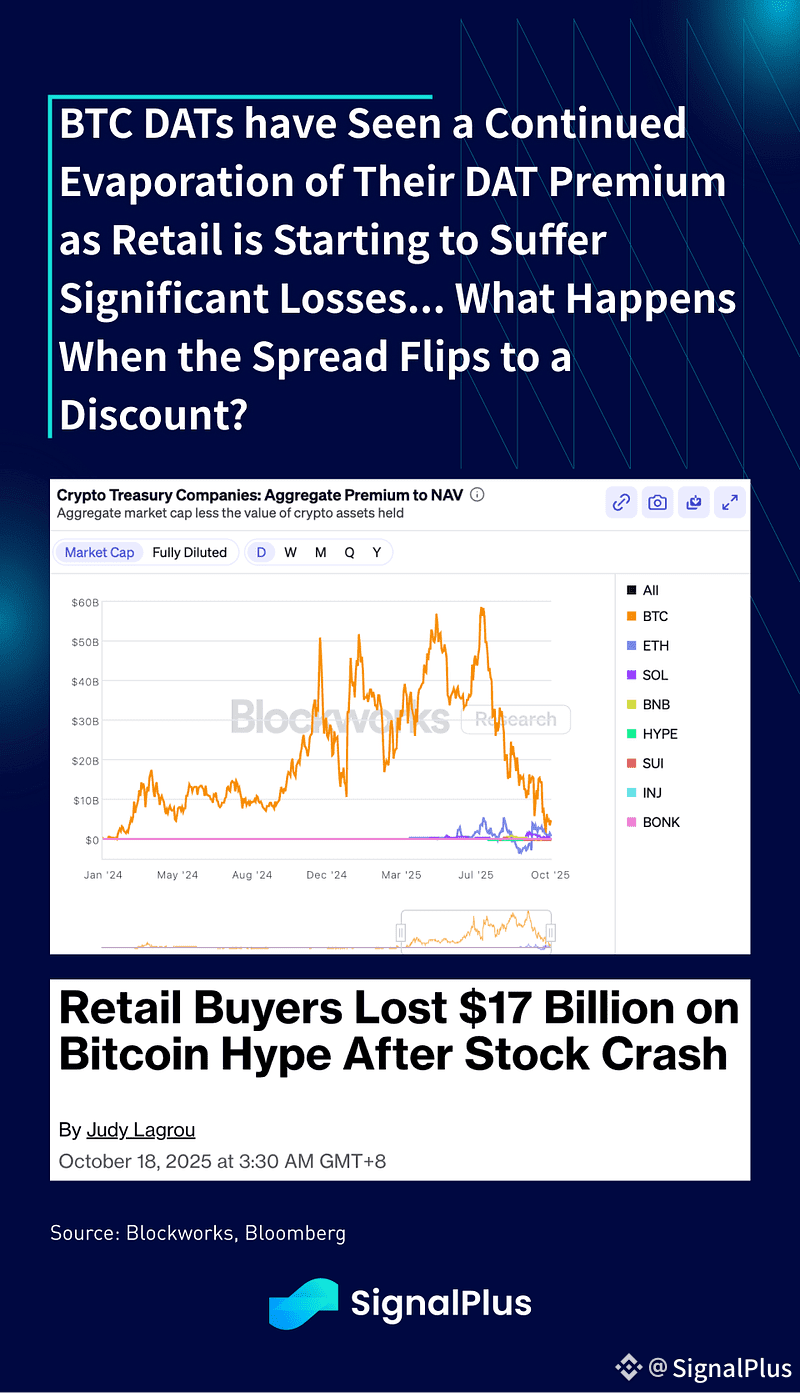

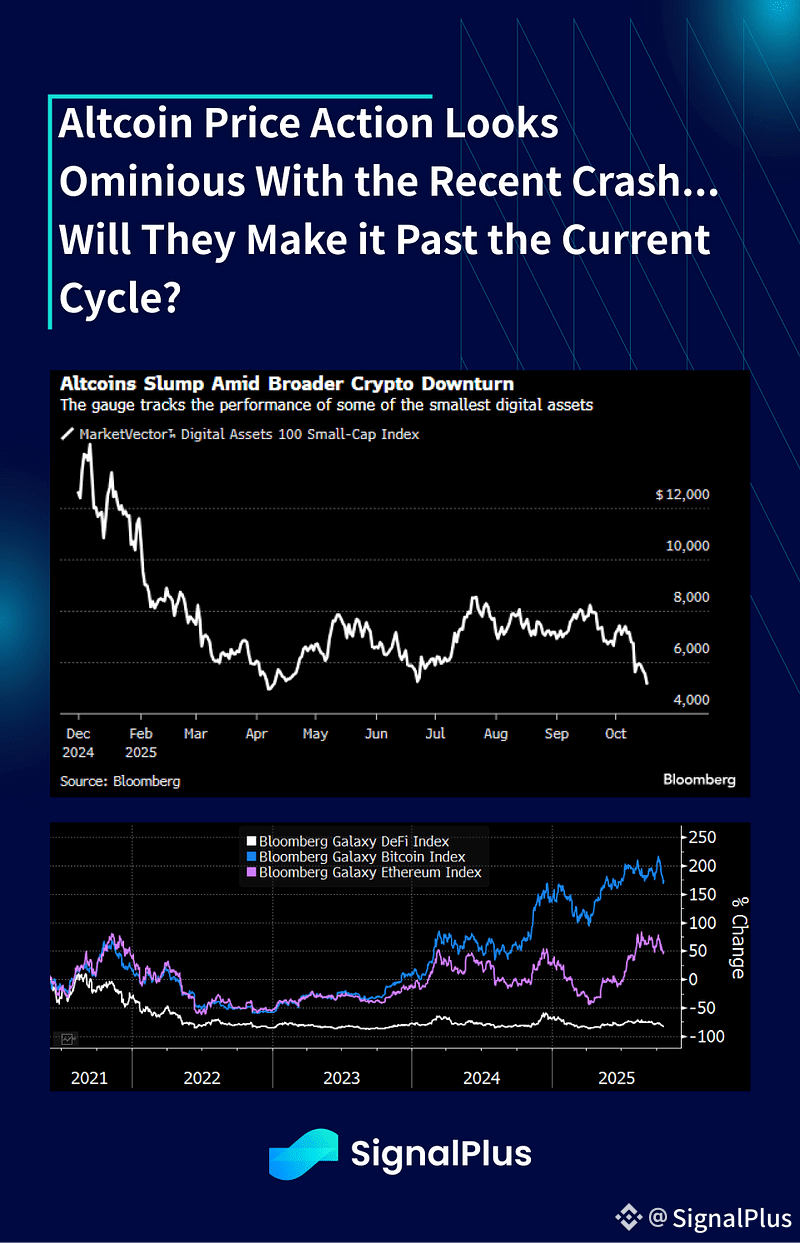

Crypto certainly has seen better weeks, with prices suffering yet another drawdown last week after the altcoin flash crash from the week before. Bloomberg reports that retail investors have lost $17bln across BTC DATs after the recent crash, with BTC ETFs seeing the 2nd worst weekly outflows YTD (-1.2bln) while DAT premium continued to crater to record lows.

DAT company owners have done well through this process, as they monetized their shares at a significant NAV premium to buy extra Bitcoin holdings, but that’s of little consolation to shareholders who have suffered a cumulative loss of $55b+ in equity premium since the early summer.

As we have long feared, this generation’s altcoins might not see much of a recovery, with the industry’s focus shifting back to TradFi’s centralised model (DAT, ETFs, private chains), and AUM/TVL continuing to shrink as ‘degen losses’ mount without a new FOMO narrative. The loss of a core Ethereum Foundation researcher (Dankrad Feist) to Stripe-owned Tempo is another sign of the seismic change in ecosystem values, while the recently announced halt of stablecoin plans out of China offers a reality check against immediate, mainstream integration.

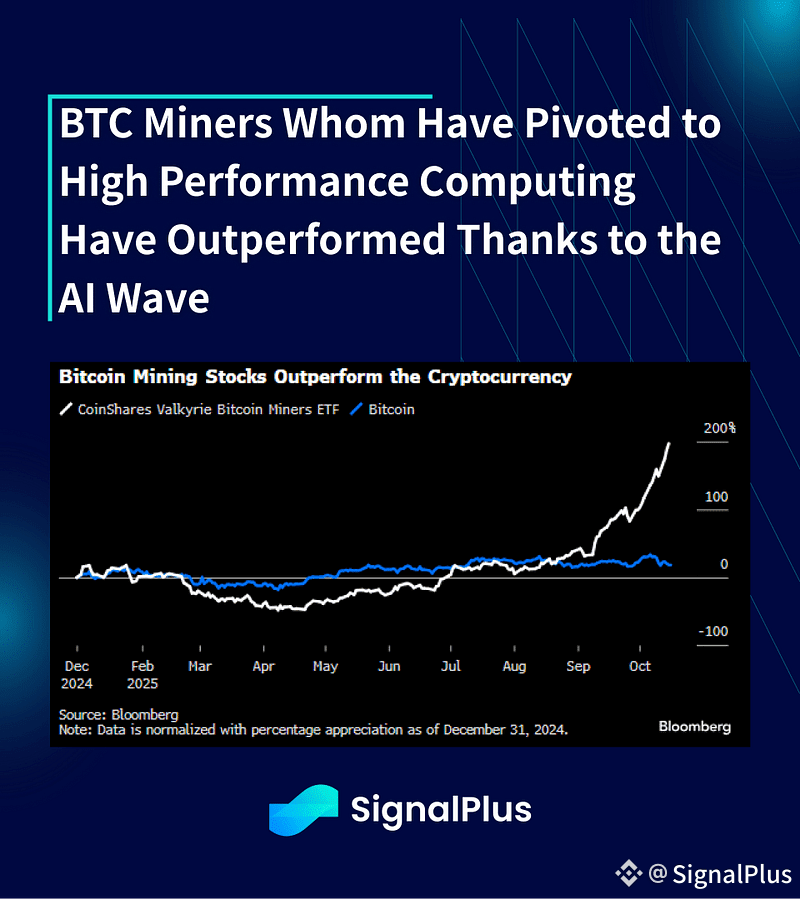

Finally, one of the few crypto-related proxies that have done well is with the public miners, who are increasingly shifting to a hybrid model to deploy their powerful hardware into AI and high performance computing (HPC) to benefit from the booming AI wave. The pivot towards AI appears to come in the wake of last year’s BTC halving, which has squeezed profit margins and forcing miners to pivot towards other economic models. Will the industry’s sustained lower hashrates help to limit supply and propel BTC prices upwards again in the medium term? Only time will tell.

Finally, the economic data calendar remains in a semi-blackout with the US government shut-down for a record 3 week period now… We might soon run out of macro things to talk about if this were to continue!

Good luck & good trading everyone.