Capital is torn between panic and greed, and the business model of digital asset treasury companies is facing a severe test.

Digital asset treasury companies are facing unprecedented pressure tests. As the cryptocurrency market continues to remain sluggish, companies that buy Bitcoin, Ethereum, and other cryptocurrencies through debt or fundraising have seen their stock price declines far exceed the value of the tokens they hold.

Over the past month, MicroStrategy's stock price has fallen by 25%, BitMine Immersion has dropped by more than 30%, while Bitcoin's drop during the same period was 15%. This extreme performance has raised doubts about the business model of 'leveraging cryptocurrency.'

One, capital tearing: Some flee while others hold firm

In the winter of the cryptocurrency market, institutional investors have shown a completely different attitude towards digital asset treasury companies.

Peter Thiel's Founders Fund has reduced its holdings in BitMine (BMNR) by half, while ARK Invest and JPMorgan have chosen to increase their positions against the trend.

On November 6, ARK Invest increased its stake in BitMine by 215,000 shares, valued at approximately $8.06 million. This capital tearing attitude highlights the market's divergence regarding the prospects of digital asset treasury companies.

Wall Street's well-known short seller Jim Chanos has consistently taken a strategy of shorting MicroStrategy while buying Bitcoin, believing that investors have no reason to pay a premium for Saylor's company. However, last Friday, he told clients it was time to close this trade. Chanos stated that while treasury company stocks are still overvalued, the premium levels are no longer extreme, 'the logic of this trade has basically been realized.'

Two, BitMine's dilemma: $3 billion in floating losses and capital consumption

As the second-largest cryptocurrency treasury company after MicroStrategy, BitMine is caught in enormous market pressure.

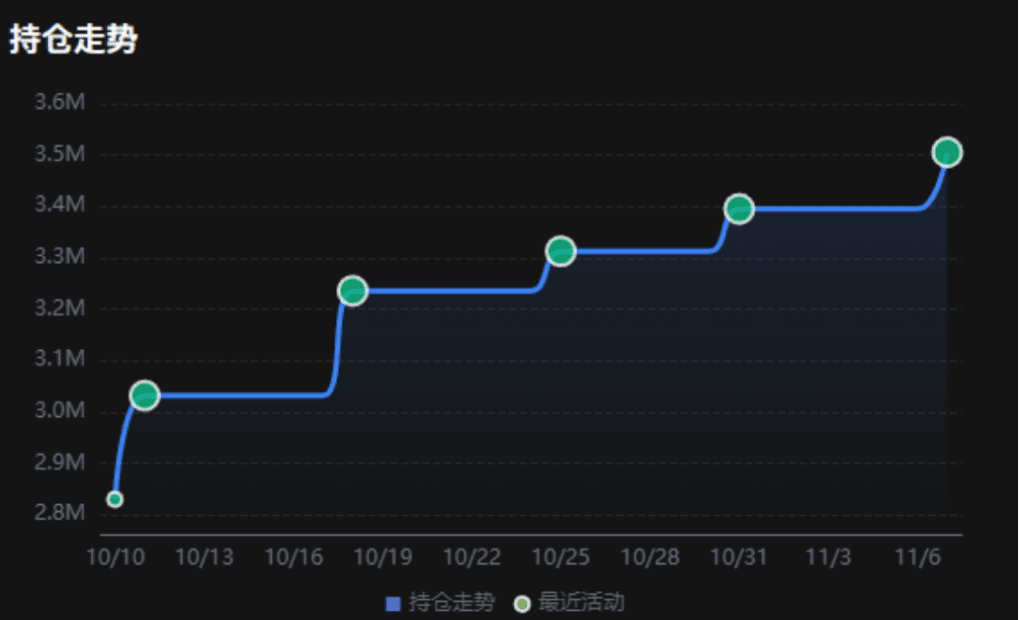

As of November 20, BitMine's holdings of Ethereum have reached 3.56 million, accounting for nearly 3% of the circulating supply, exceeding halfway to the long-term target of 6 million. However, based on the average purchase price of $4,009, BitMine's book losses are approaching $3 billion.

The company's stock price has fallen about 80% from its July peak, with a current market value of approximately $9.2 billion, below its ETH holding value of $10.6 billion (based on ETH at $3,000). Its mNAV (modified net asset value) has fallen to 0.86, reflecting market concerns about the company's unrealized losses and the sustainability of its funds.

Investor focus has shifted from 'how much more can we buy' to 'how much longer can we hold on.' Currently, BitMine's cash reserves are approximately $607 million, with the company's funding primarily coming from cryptocurrency asset income and secondary market financing.

Three, MicroStrategy's aggressive strategy: Continuous bottom fishing and financing innovation

Unlike BitMine, MicroStrategy (now renamed Strategy) continues to maintain an aggressive buying strategy amidst market declines.

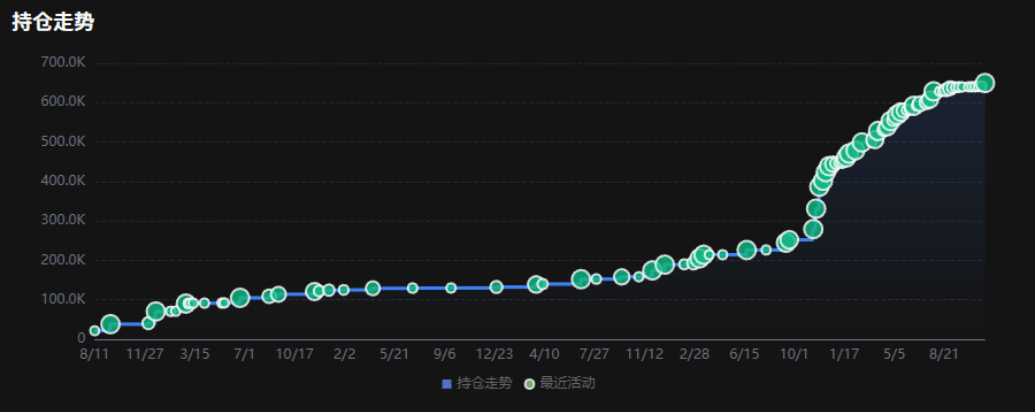

Between November 10 and 20, Strategy acquired 8,178 Bitcoins, valued at approximately $835.6 million, marking the company's largest Bitcoin acquisition since the end of July.

This purchase brings Strategy's total holdings to 649,870 Bitcoins, accounting for more than 3% of Bitcoin's total supply. The total cost of these Bitcoins is approximately $48.37 billion, with an average purchase price of $74,433.

Strategy's latest acquisition was primarily financed through the proceeds from its new preferred stock issuance. The company raised approximately $715 million through its STRE or 'Stream' series, expanding its high-yield tools to European investors. It also obtained an additional $131.4 million through its STRC or 'Stretch' preferred series.

Four, the leverage effect and the disappearance of premiums

The core issue of digital asset treasury companies is that investors are effectively paying a premium far above the net asset value of the companies holding cryptocurrencies.

Brent Donnelly, president of Spectra Markets, bluntly stated, 'This entire concept makes no sense to me. You're just buying a $1 bill for $2. Ultimately, these premiums will be compressed.'

The leverage effect has been amplified in the downturn. Matthew Tuttle stated, 'Digital asset treasury companies are essentially leveraged crypto assets, so when cryptocurrencies fall, they fall even more.' The MSTU ETF he manages aims to provide double the return of MicroStrategy, and the fund has plunged 50% in the past month.

Digital currency treasury companies initially provided a channel for institutional investors who previously found it difficult to invest directly in cryptocurrencies. However, cryptocurrency exchange-traded funds launched in the past two years can now offer the same solutions, weakening the unique value proposition of treasury companies.

Five, buying power has completely retreated

The current environment facing the cryptocurrency market is exceptionally severe, with major buying powers retreating.

Continuous capital outflows have occurred in Bitcoin and Ethereum spot ETFs. On November 19, the spot Bitcoin ETF saw an outflow of $254.5 million, while the spot Ethereum ETF experienced an outflow of $182.8 million. This marks the fourth consecutive day of net outflows for the Bitcoin ETF and five consecutive days for the Ethereum ETF.

Nick Ruck, director of LVRG Research, stated, 'This outflow trend indicates a cautious attitude among institutional investors, reflecting broader macroeconomic headwinds, such as fiscal uncertainty and rising interest rate expectations, eroding the 'value storage' narrative of these traditional assets.'

On-chain, Glassnode data reports that long-term holders (addresses holding more than 155 days) are currently selling approximately 45,000 ETH daily, amounting to about $140 million. This is the highest selling level since 2021, indicating a weakening of current bullish power.

Six, the value mismatch debate: Potential opportunities for BitMine

Amidst widespread pessimism in the market, voices suggesting that BitMine has a value mismatch are gradually emerging.

Compared to MicroStrategy's path, BitMine has chosen a completely different approach. MicroStrategy heavily relies on convertible bonds and preferred stocks to raise funds in the secondary market, with annual interest burdens in the hundreds of millions of dollars, and profitability depends on Bitcoin's unilateral rise.

Although BitMine diluted its equity through new stock issuance, it has almost no interest-bearing debt, while its held ETH contributes approximately $400-500 million in staking income each year, making this cash flow relatively rigid.

As one of the largest institutional holders of ETH globally, BitMine can fully utilize staked ETH for restaking (earning an additional 1-2%), operating node infrastructure, locking in fixed returns through yield tokenization, and even issuing institutional-grade ETH structured notes. These are operations that MicroStrategy's BTC holdings cannot achieve.

Currently, BitMine's market value in the US stock market is about 13% lower than the value of its ETH holdings. Within the entire DAT sector, this discount is not the most exaggerated, but it is significantly lower than the historical pricing center for similar assets.

As of November 20, after severe fluctuations, Bitcoin has fallen back to $91,253, while Ethereum has broken below the critical support of $3,000. Amidst the wailing of the market, Strategy's Michael Saylor still claims on social media that Bitcoin is currently on 'discount sale.'

The stock price of treasury companies has fallen to historic lows, with BitMine's mNAV at 0.86 and Strategy's mNAV at around 0.93. The market stands at a crossroads: one side is the potential end of the treasury model being replaced by ETFs, while the other side is a once-in-a-lifetime opportunity for valuation repair.