Sharing a very wonderful in-depth industry article, authored by a partner from Dragonfly Capital. The article deeply explores the current sentiment shift in the crypto market—from 'nihilism' to 'cynicism'—and powerfully defends the 'exponential growth' valuation logic of public blockchains by borrowing from the early development of the internet (especially Amazon).

The following is the full English translation:

In the past, I often told founders that the feedback they receive when launching a product would not be hatred, but indifference. By default, no one will care about your new public blockchain.

Now I have to stop saying such things. Monad just launched this week, and I've never seen a newly launched blockchain encounter so much hatred. I have been professionally investing in cryptocurrency for over 7 years. Before 2023, almost every new chain I saw at launch was met with enthusiasm or indifference.

But now, new public chains are born amid a chorus of hatred. Projects like Monad, Tempo, and MegaETH, which haven't even launched on the mainnet yet, are already facing an astonishing number of 'haters.' This is indeed a new phenomenon.

I've been trying to diagnose: why is this happening now? What does it mean for the psychological state of this market?

The remedy is worse than the disease.

Warning: This will be the most vague blockchain valuation article you've ever read. I don't have fancy metrics or charts to sell you. Instead, I will contradict the current zeitgeist of 'Crypto Twitter' (CT) — for the past few years, I've been on the opposite side of this spirit.

In 2024, I feel that what I'm rebutting is financial nihilism. Financial nihilism believes these assets don't matter; at the end of the day, they are all memes, and everything we've built is essentially worthless.

Thank goodness, that's no longer the atmosphere now. We're breaking that spell.

But the current zeitgeist is what I call financial cynicism: well, maybe this stuff has some value, maybe not all is a meme, but it is seriously overvalued, and it’s only a matter of time before Wall Street figures that out. It’s not to say all chains are worthless. But the value of these things might only be 1/5 to 1/10 of their current trading price (do you see those earnings multiples?), so you’d better pray hard that Wall Street doesn’t expose our tricks, because once they do, everything will go to zero.

Now there are many bullish analysts trying to counter this sentiment by exaggerating L1's valuation models, raising price-to-earnings ratios (PE), gross margins, and discounted cash flows (DCF).

At the end of last year, Solana proudly embraced REV (Revenue/Real Economic Value) as the ultimate indicator that could prove its valuation reasonable. They proudly announced: We — and only we — will no longer bluff to Wall Street!

Of course, almost immediately after embracing REV, the metric plummeted off a cliff (though $SOL interestingly outperformed REV). It's not that there’s anything wrong with REV. REV is a very clever metric. But this article isn't about metric selection.

Then there’s the launch of Hyperliquid. This is a DEX with real revenue, buybacks, and earnings multiples. The chorus says — look, see, I told you! Finally, for the first time ever, there’s a token that has real profits and reasonable earnings multiples. (Don't mention BNB, we're not talking about that.) Hyperliquid will devour everything because clearly, neither Ethereum nor Solana has any real earning capacity, and we can stop pretending to value them now.

Hyperliquid, Pump, Sky, these high-repurchase tokens are great. But the market has always had the ability to invest in exchanges. You can always buy Coinbase, or BNB, or whatever else. We hold $HYPE, and I agree it’s a great product.

But that’s not the reason why people invest in ETH and SOL. L1 public chains do not have the profit margins of exchanges, but that’s not why people buy them — if they wanted that, they could easily buy Coinbase stock.

Since I'm not criticizing the financial metrics of blockchain, maybe you think this article will denounce the evils of the 'token industrial complex.'

Clearly, everyone lost money on tokens in the past year, including VCs. Altcoins have plummeted this year. Therefore, the other half of the zeitgeist on CT is arguing over who should be blamed. Who got greedy? Was it the VCs? Was it Wintermute? Was it Binance? Was it the farmers? Was it the founders?

The answer, of course, is the same as before.

Everyone is greedy. Everyone. VCs, Wintermute, farmers, Binance, KOLs, they are all greedy, and so are you. But that's okay. Because no well-functioning market requires anyone to act against their self-interest. If we are right about cryptocurrency, we can all be greedy, and investing will still succeed. Trying to analyze a declining market by figuring out 'who is greedy' is about as effective as starting a witch hunt. I assure you, no one suddenly started being greedy in 2025.

So, this isn't what I want to write about either.

Many people want me to write an article explaining why $MON should be valued at X or why $MEGA should be valued at Y. I'm not interested in writing such articles, nor do I advocate you buy any specific thing. In fact, if you don't believe in them, you probably shouldn't buy.

Will the new challenger public chains win? Who knows. But if it has a substantive chance of winning, it will be priced on that basis. If Ethereum is worth $300 billion, and Solana is worth $80 billion, then a project with a 1-5% chance of becoming the next Ethereum or Solana will be priced according to those probabilities.

Somehow, CT is shocked by this, but it’s no different from biotech. A drug with less than a 10% chance of curing Alzheimer’s, even if it has a 90% chance of not passing phase three clinical trials and going to zero, will be priced in the billions. That’s how math works — it turns out the market is very good at doing math. Binary outcomes are priced based on probabilities rather than extrapolated annual revenue or moral depravity. This is the 'shut up and do the math' school of valuation.

I really don't think this is an interesting question worth writing about. '5% chance of winning? No way, it's clearly a 10% chance!' The market, not the article, is the best way to assess any individual token.

So what I really want to write is: CT seems to no longer believe that public chains have value.

I don't think it's because they don't believe new chains can gain market share. We just saw Solana dominating the market less than 2 years after rising from the ashes. It's not easy, but it's certainly possible.

More so, people are starting to believe that even if a new chain wins, there aren’t any prizes worth winning. If $ETH is just a meme, if it never generates real income, then even if you win, you won’t be worth $300 billion. This race isn’t worth winning because these valuations are nonsense, and everything will collapse before you claim your prize.

Being optimistic about public chain valuations has become passé. It's not to say there aren’t optimists — clearly, there are certainly some out there. Where there are sales, there are purchases, and even though the cool kids of CT like to mock L1, people are still quite willing to buy SOL at $140 and ETH at $3000.

But now there's a notion that all the smartest people have stopped buying smart contract public chains. The smart money knows the game is over. If not now, then soon. The only people buying here are fools — Uber drivers, Tom Lee, and those KOLs who say things like 'trillions.' Maybe even the U.S. Treasury. But definitely not smart money.

This is nonsense. I don't believe it, and you shouldn't either.

So I feel I must write a manifesto for the smart people, explaining why general public chains are valuable. This article isn't about Monad or MegaETH. It's actually defending ETH and SOL. Because if you believe ETH and SOL are valuable, everything else naturally follows.

Feel the exponential growth.

My partner Bo has personally experienced the boom of the Chinese internet as a venture capitalist. I have heard countless times that 'cryptocurrency is like the internet,' to the point where I am numb to it. But when I hear his stories, it always reminds me how expensive the cost of getting these things wrong can be.

One story he often tells is that in the early 2000s, all the early e-commerce VCs (it was a small circle at the time) gathered together for coffee. They debated: how big will the market for e-commerce be?

Is it mainly electronics (maybe only tech geeks use computers)? Does it work for women (maybe they're too focused on touch)? What about food (maybe perishables are hard to manage)? For early VCs, these are crucial questions in determining what to invest in and at what price.

The answer, of course, is that each and every one of them was wildly wrong. E-commerce will sell everything, and the target audience is the whole damn world. But at the time, no one really believed that. Even if they did, it was too ridiculous to say it out loud.

You just need to wait long enough for exponential growth to show you results. Even among believers, few imagined e-commerce would become as big as it is now. And among those few believers, nearly all became billionaires simply for not selling. Every other VC — as Bo told me, because he is one of them — sold too early.

In the realm of cryptocurrency, believing in exponential growth has become outdated.

I believe in the exponential growth of cryptocurrency. Because I have experienced it.

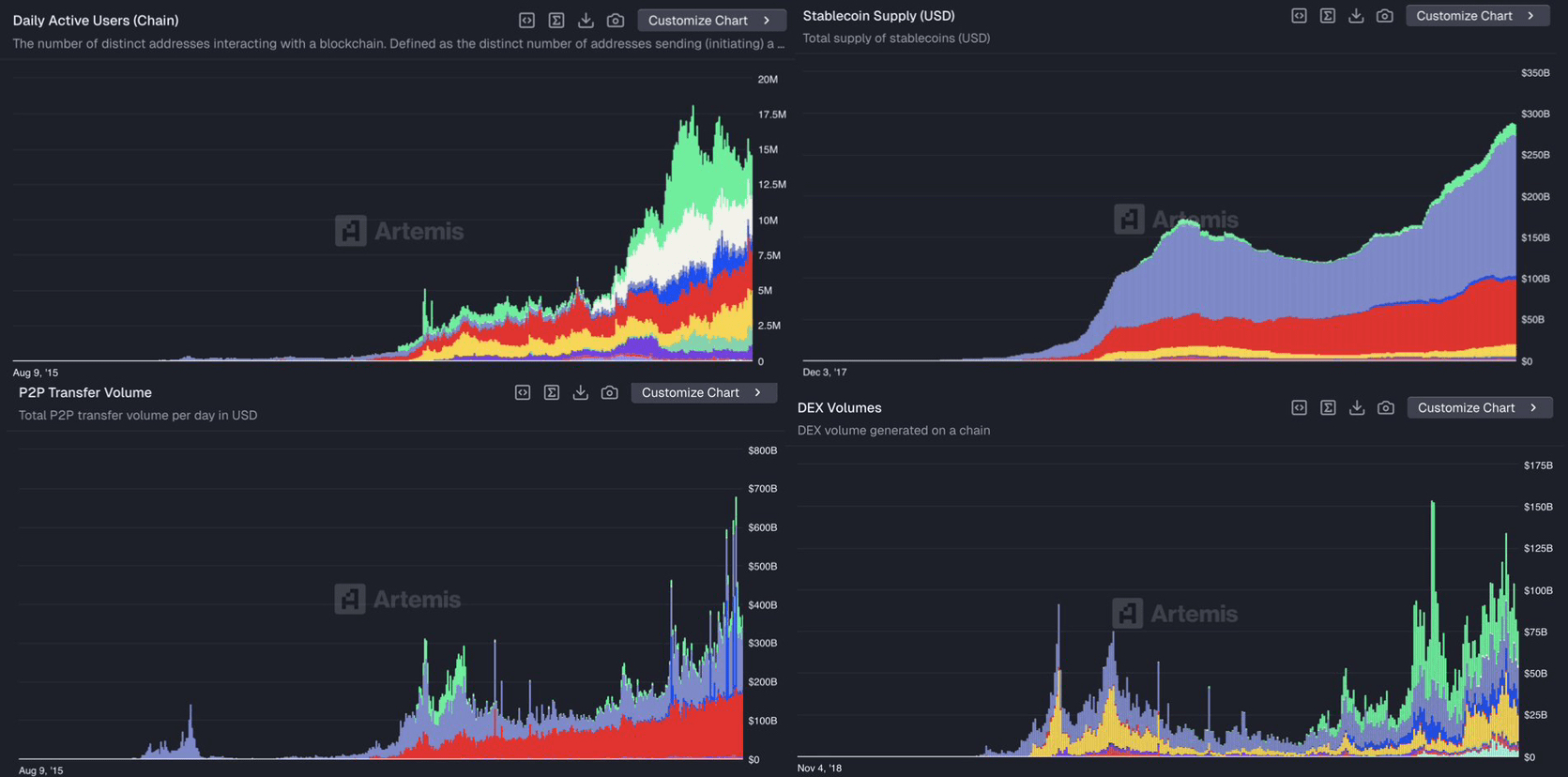

When I first got into cryptocurrency, no one was using this stuff. It was tiny, fractured, and terrible. The on-chain TVL was only a few million. We invested in the first generation of DeFi, MakerDAO, Compound, 1inch, when they were just scientific experiments. I remember playing on EtherDelta when DEXs had only a few million dollars in daily trading volume, which was considered a huge success. That experience was just garbage. Now our daily on-chain trading volume usually reaches hundreds of billions of dollars. I remember thinking it was crazy when Tether's issuance hit $1 billion, (The New York Times) even wrote an article saying it was a Ponzi scheme on the brink of collapse. Now stablecoins are over $300 billion and regulated by the Federal Reserve.

I believe in exponential growth because I have experienced it. I have seen it happen time and time again.

But you might argue — well, the growth of stablecoins might be exponential, and maybe the trading volume of DeFi is exponential, but they won't accumulate to ETH or SOL. The value is not captured by public chains.

My answer to this is: you still don't believe in exponential growth.

Because the answer to exponential growth is always the same: it doesn’t matter. This stuff is going to be much bigger than today. When it becomes absolutely huge, you will make money through economies of scale.

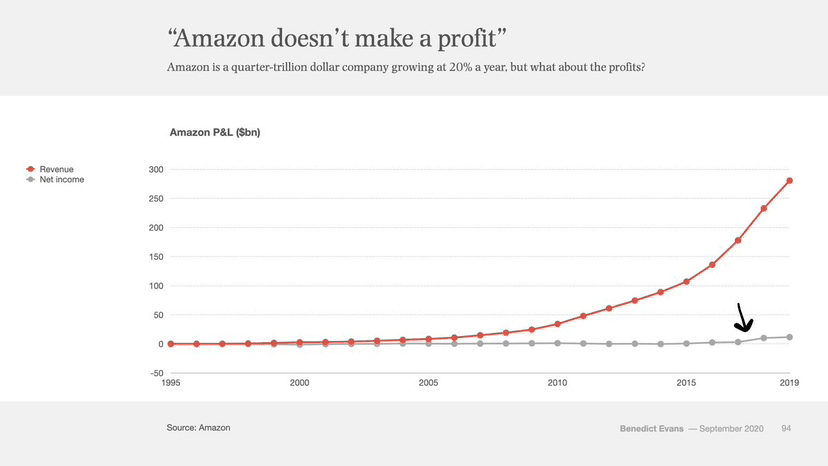

Take a look at this chart.

This is Amazon's profit and loss statement from 1995 to 2019. That's 24 years. The red is revenue, the gray is profit. Do you see that little bump at the end of the gray line? That was when Amazon really started making a profit, 22 years after its founding.

When the little gray line representing net income first deviated from the 0 axis, Amazon was already 22 years old. In every year prior, there were column articles, critics, and short-sellers claiming Amazon was a Ponzi scheme that would never make money.

Ethereum just turned 10. This is what Amazon's stock looked like in its first 10 years:

10 years of turmoil. All the way, Amazon was surrounded by skeptics and non-believers. Is e-commerce a charity subsidized by VCs? They sold low-priced, low-quality trinkets to bargain hunters, who cares? How could they ever make real money like Walmart or General Electric?

If you’re arguing about Amazon's price-to-earnings (P/E), then you’re in the wrong category. That’s the realm of linear growth. But e-commerce is not a linear trend, so every debate about the P/E over the past 22 years has been wildly wrong. No matter how much you paid, no matter when you bought, you weren’t bullish enough.

Because that's the power of exponential growth. When it comes to truly exponential technologies, no matter how big you think they will become, they will only get bigger.

This is something that Silicon Valley has always understood better than Wall Street. Silicon Valley grew up in exponential growth, while Wall Street grew up in linear thinking. Over the past few years, the focus of cryptocurrency has shifted from Silicon Valley to Wall Street. You can feel it.

Admittedly, the growth of cryptocurrencies doesn't look as smooth as the growth of e-commerce. It's explosive, intermittent. This is because cryptocurrency is about money, closely tied to macro forces, and it faces a much more intense regulatory tug-of-war than e-commerce. Cryptocurrency strikes at the core of nations — currency — so it unnerves governments more than e-commerce.

But exponential growth is equally inevitable. This is a rough argument. But if cryptocurrency is exponential, then this rough argument is correct.

Zoom out.

Financial assets want freedom. They want to be open. They want to be interconnected. Cryptocurrency transforms financial assets into file formats, making sending a dollar or a share as easy as sending a PDF. Cryptocurrency makes everything interconnected possible. It makes everything 24/7, global, interconnected, and open.

This will win. Openness always wins.

If I've learned anything from the internet, it’s this. The vested interests will oppose it, the government will bluff, but ultimately they will surrender to the adoption, productivity, and sheer efficiency that this technology brings. This is what the internet has done to all other industries. Blockchain is how this trend will consume all finance and currency.

Yes — given enough time — all of finance and currency.

There's an old saying: people overestimate what can happen in two years and underestimate what can happen in ten.

If you believe in exponential growth, if you pull your vision wide enough, then everything still seems cheap. What should humble you is that every day, holders outlast sellers and opponents. The time horizons of large capital are much longer than the swing traders on CT would have you believe. Large capital is trained by history and does not dismiss great technologies. You know that grand story that initially made you buy $ETH or $SOL? Large capital believes that story and has not stopped believing.

So what exactly am I arguing?

I am arguing that applying price-to-earnings ratios to smart contract public chains (the so-called 'revenue meta') is to abandon exponential growth. It means you have categorized this industry into linear growth. It means you believe that having 30 million daily active users (DAU) on-chain and less than 1% of M2 is the endpoint. Cryptocurrency is just one of the things in the world. A supporting role. It hasn’t won. It’s not inevitable.

Most importantly, I'm arguing to be a believer. Not just a believer, but a long-term believer.

I am arguing that this exponential growth will be greater than anything else you've ever participated in during your life. This is your 'e-commerce moment.' When you're old, you'll tell your kids — I was there when it all happened. Not everyone believes this is possible: the whole society can change, and all currencies and finance will be transformed by programs running on decentralized computers we all own.

But it did happen. It changed the world.

And you were part of it.

Disclosure: The above represents personal views only. Dragonfly is an investor in $MON, $MEGA, $ETH, $SOL, $HYPE, $SKY, and many other tokens. Dragonfly believes in exponential growth. This is not investment advice, but rather another kind of advice.