On the first trading day of December, Bitcoin BTC, Ethereum ETH, and other major tokens continued to decline on Monday morning (December 1), extending the sharp decline from the end of November. This flash crash had no obvious news trigger, and some analysts pointed out that the DeFi platform Yearn Finance has once again triggered market panic.

As the largest cryptocurrency by market capitalization, Bitcoin fell more than 3% in early Asian trading, approaching $85,000. According to CoinDesk data, Ethereum fell by 5%, while Solana (SOL), Dogecoin (DOGE), and Ripple (XRP) all dropped over 4%.

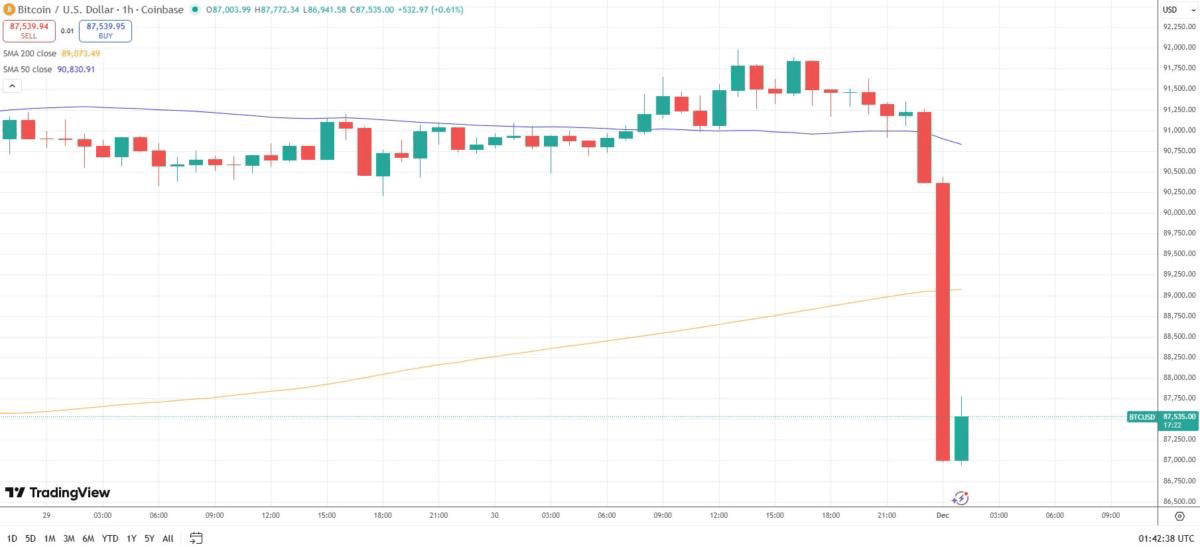

The cryptocurrency market suddenly crashed.

Bitcoin failed to break through a key resistance level over the weekend, and within three hours, it plunged nearly 5%. TradingView data shows that the asset spent most of the weekend fluctuating around $91,500, seemingly preparing for a month-end close, but then suddenly dropped to $86,950 on Coinbase.

This nearly 5% drop occurred just as the first weekly gain was recorded after four consecutive weeks of red weekly closes. According to TradingView, Bitcoin closed that week at $90,411.

The Kobeissi Letter noted, 'This year we have seen countless times that Friday nights and Sunday nights are often accompanied by significant volatility in the crypto market.' The institution added that this decline had no obvious news-triggering factors.

Kobeissi attributed the flash crash to 'a sudden surge in sell orders that triggered a domino-like sell-off, further exacerbated by a large number of leveraged positions being liquidated.'

'The current crypto 'bear market' still has structural characteristics. We do not believe this is a fundamental-driven decline.'

Over 180,000 traders were liquidated in the past 24 hours, with a total liquidation scale of $539 million, most of which occurred in the last few hours, according to CoinGlass. About 90% were long positions, primarily concentrated in Bitcoin and Ethereum (ETH).

CoinGlass data shows that Bitcoin recorded its worst monthly performance this year, also its worst November since 2018, with a monthly decline of 17.49%. In November 2018, Bitcoin had plummeted 36.57% in a brutal bear market.

Analyst 'Sykodelic' remains bullish, stating, 'In fact, this is a good start to the month.'

He mentioned that the market could not rebound on Sunday, the CME gap has been filled, and long positions worth $400 million have been liquidated. 'The liquidity below was swept first—this is exactly what we wanted to see.'

Yearn Finance exacerbates panic.

Some analysts also believe that the DeFi platform Yearn Finance has exacerbated market panic, becoming the trigger for a new round of sell-offs. Yearn's X (formerly Twitter) account issued an alert hours ago stating that its yETH liquidity pool had experienced an 'event,' but its V2 and V3 vaults remained safe and unaffected, after which the sell-off accelerated.

Discussions on social media indicate that attackers exploited vulnerabilities to mint large amounts of yETH in a single transaction, draining the liquidity pool and extracting about 1,000 ETH (worth around $3 million), which was then transferred via a mixer. yETH is a user-governed liquidity pool token composed of various Ethereum liquid staking derivatives (LSTs).

According to data from blockchain security firm PeckShield, the protocol suffered losses of $9 million, of which 1,000 ETH was transferred to the mixing service Tornado Cash. The attacker's address (0xa80d...c822) still holds about $6 million in tokens.

The issues with Yearn occurred just days after Korea's largest exchange, Upbit, suffered a multimillion-dollar hacking attack, highlighting the influx of institutional capital pushing up crypto asset valuations, while security infrastructure has not been strengthened accordingly.

The drop came unexpectedly.

The sell-off in Asia's early trading caused the liquidation scale of cryptocurrency leveraged contracts to exceed $400 million, mostly from long positions, according to Coinglass data. This indicates that many traders were betting on a rebound but were caught off guard by the sudden drop.

Bitcoin's performance in November, measured in UTC, fell by 17.5%, marking the largest monthly decline since March of this year; despite this, Bitcoin's price briefly rose from nearly $80,000 to over $90,000 at the end of the month. Ethereum fell by 22%, marking its worst performance since February.

The weak trend is backed by a significant reduction in institutional demand. According to SoSoValue data, Bitcoin spot ETFs listed in the U.S. experienced a net outflow of $3.48 billion in November, marking the second-largest redemption in history; the outflow of Ethereum ETFs set a record, reaching $1.42 billion.

Sean McNulty, head of derivatives trading for FalconX in the Asia-Pacific region, believes that as we enter December, the market is shrouded in risk-averse sentiment. 'The biggest concern is the lack of inflows into Bitcoin exchange-traded funds (ETFs) and the absence of buyers stepping in to buy on dips. We expect structural resistance to persist this month. We see $80,000 as the next key support level for Bitcoin.'

Policymakers are weighing the direction of interest rates before 2026, and this week will provide critical guidance for the momentum of the U.S. economy. Some data may influence the market's expectations regarding whether the Federal Reserve will continue its rate-cutting cycle. On Sunday (November 30), U.S. President Trump stated that he had identified a candidate for the next Federal Reserve Chair, having previously expressed anticipation that the nominee could push for rate cuts.

China pledges to intensify efforts to crack down on crypto activities.

According to the China Daily, mainland China reiterated its anti-crypto stance and pledged to intensify efforts to crack down on speculative activities involving virtual currencies.

At a cross-departmental meeting held on Friday, officials from the People's Bank of China, the Ministry of Public Security, and the Central Cyberspace Affairs Commission emphasized that virtual currencies do not have legal tender status and cannot be used as currency in the market; all related activities are considered illegal financial businesses.

Officials warn that the recent surge in speculative trading has brought new financial risks and challenges.

Beijing has long maintained an anti-crypto stance, cracking down on mining activities and speculative trading. However, recent data shows that China has once again become the world's third-largest Bitcoin BTC mining center.

During the meeting, the People's Bank of China specifically pointed out that stablecoins—tokens pegged to fiat currencies—lack sufficient customer identity verification and anti-money laundering protections, making them susceptible to money laundering, cross-border illegal capital flows, and fraud. These statements sharply contrast with the increasingly friendly regulatory environment for stablecoins in the United States.

Despite the mainland reiterating its anti-crypto stance, Hong Kong operates under an independent legal system. The Hong Kong government has consistently supported the development of the crypto industry, with stablecoins becoming a key topic at the government-supported 'Hong Kong FinTech Week' event. Hong Kong's Financial Secretary Paul Chan also served as the keynote speaker at the Consensus Summit hosted by CoinDesk.