In the evolving landscape of decentralized finance (DeFi), the battle is no longer just about "yield generation," but has shifted to a more complex level known as "Capital Efficiency." Falcon Finance stands out not just as a lending protocol, but as the first all-encompassing collateral infrastructure aimed at solving one of the biggest dilemmas in the digital economy: how to liquidate illiquid assets without giving up ownership or their underlying returns.

This article reviews the technical and economic architecture of Falcon Finance, the role of USDf as an over-collateralized synthetic dollar, and how this model represents a vital bridge between digital assets and real-world assets.

1. Economic philosophy: The shift from storage to activation

Traditionally, investors in digital assets face a strict binary choice: either hold the asset (HODL) to wait for its value to rise with no cash liquidity, or sell the asset to get cash (USD) while losing exposure to the future growth of the asset.

Falcon Finance comes to break this binary through the concept of "collateral monetization." The core idea here is to transform the investment portfolio—whether it consists of Ethereum (ETH), wrapped Bitcoin (WBTC), or tokenized treasury bonds—into an "active store of value."

Economically, this increases the velocity of money within the ecosystem. Instead of assets being "idle" in cold wallets, they become a base for printing new purchasing power (USDf) that can be used in yield strategies, hedging, or daily payments, all while the underlying asset continues to grow (or distribute its returns if it is of the type LSTs or RWAs).

2. The compounded dollar (USDf): The technical architecture of the stablecoin

The USDf currency is not an algorithmic stablecoin relying on risky burn and mint mechanisms (as happened with Terra/Luna), nor is it a fully cash-backed currency in banks (like USDT). It is an over-collateralized synthetic dollar.

Technical operating mechanism:

To issue 1 dollar of USDf, the protocol requires a collateral deposit exceeding 1 dollar (e.g., 1.50 dollars). This is known as the "Collateral Ratio - CR."

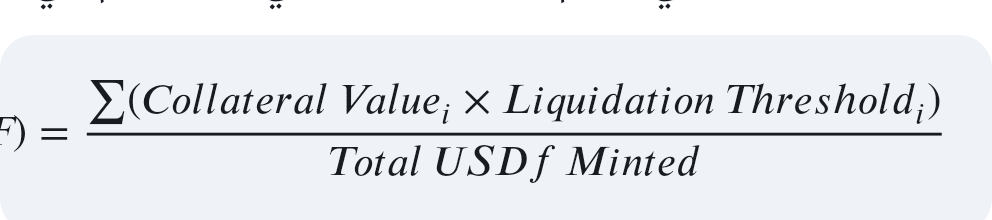

The fundamental equation governing the user's financial position is:

Where:

Collateral\ Value: The current market value of the deposited asset.

Liquidation\ Threshold: The allowable liquidation threshold for the asset (varies based on the asset's volatility).

Why the excess collateral?

In the volatile blockchain world, over-collateralization acts as a shock absorber. If the value of the deposited assets (like ETH) decreases, the value of USDf remains stable because it is backed by assets exceeding their nominal value. This model, which resembles the MakerDAO model but is more sophisticated and diverse in the accepted assets, ensures "peg robustness" to the US dollar.

3. Integration of real-world assets (RWAs): The new frontier

What technically distinguishes Falcon Finance is its "asset-agnostic" infrastructure. It is not limited to native cryptocurrencies but extends to include tokenized real-world assets (Tokenized RWAs).

This is a crucial integration for two reasons:

Reducing correlation: Crypto markets are highly correlated with each other. When Bitcoin drops, most currencies drop. However, integrating US treasury bonds or tokenized real estate as collateral provides stability to the system, as these assets do not move in the same direction as crypto.

External yield import: A user can deposit an RWA asset (yielding, for instance, 5% from bonds), and use it as collateral to mint USDf. Here, the user receives the real yield from the bonds + liquidity from USDf to invest in DeFi. This creates what is called "yield stacking."

4. The comprehensive infrastructure: How does it work?

Falcon Finance operates as a liquidity layer bridging multiple networks and protocols. The technical architecture consists of several modules:

Vaults Module: Where the collaterals are locked. These smart contracts are designed to accept various standards of tokens (ERC-20 and others) and handle different types of yield mechanisms (Rebasing tokens vs. Accumulating tokens).

Oracle Module: Relies on decentralized price feeds (like Chainlink) to ensure accurate and real-time valuation of the deposited assets, preventing price manipulation or flash loan attacks.

Stability Engine: Continuously monitors the system. If the value of the user's collateral approaches the danger threshold, the system enables liquidators to buy the collateral at a discount to rebalance the system and burn the corresponding USDf, maintaining the protocol's solvency.

5. The macroeconomic impact on DeFi

Presenting Falcon Finance as a comprehensive collateral infrastructure addresses the issue of "liquidity fragmentation." Instead of liquidity being trapped in isolated protocols, Falcon allows for a wide range of assets to mint a unified currency (USDf).

Capital efficiency: Institutions and hedge funds can use their long-term assets as collateral to fund short-term operations without needing to incur taxable events resulting from sales.

True decentralization: Relying on USDf reduces the DeFi sector's reliance on centralized stablecoins (like USDC and USDT) whose issuers have the ability to freeze funds.

6. Risks and hedging strategies

No financial system is without risks. In the case of Falcon Finance, the main risks lie in:

Smart contract risks: The likelihood of software vulnerabilities.

De-pegging risks: If the value of the collateral collapses faster than the speed of liquidation.

Custody Risk for RWAs: Real-world assets ultimately rely on a centralized off-chain custodian.

Falcon addresses these risks through:

Strict criteria for asset acceptance (Risk Parameters & LTV ratios).

Multiple security audits.

Insurance Funds to absorb bad debts in extreme market volatility.

Conclusion: The future of on-chain liquidity

Falcon Finance represents a qualitative leap from "experimental decentralized finance" to "institutional decentralized finance." By accepting liquid assets and real-world assets (RWAs) in a single collateral pool to issue USDf, it offers an elegant solution to the liquidity problem.

The ability to access instant liquidity via USDf without liquidating investment positions grants users the power of "healthy leverage," where debt is used not for blind speculation, but to maximize the efficiency of already-existing assets. In a world moving towards the tokenization of everything, the infrastructure that can absorb these tokens and convert them into liquid purchasing power will be the backbone of the new digital economy.

Would you like me to prepare a comparative analysis between USDf and other stablecoins like DAI or USDe to illustrate the differences in risks and returns?