Michael Saylor's BTC Prague 2026 keynote, titled "Digital Capital, Equity, and Credit," made an argument that quietly marks a shift in how the most prominent corporate Bitcoin advocate talks about the asset.

Key Takeaways

Saylor says Bitcoin has won the monetary race; the work now is building products.

Bitcoin holds $1.2T of a $1,000T global capital pool, roughly 10 basis points.

Four product layers, digital capital, credit, money, and yield, channel that capital in.Adoption comes through products people love, not Bitcoin ideology.

The thesis in one sentence: Bitcoin has already won, and the only job left is building the financial products that channel the world's conventional capital into the network. What makes that framing notable is what it concedes. After years of evangelism, Saylor, executive chairman of Strategy (formerly MicroStrategy), is effectively saying the persuasion phase is over and the plumbing phase has begun.

He opened by placing himself within a framework he had published a week earlier, four Bitcoin ideologies he labels the maximalists, capitalists, technologists, and fundamentalists. He counts himself as all four, but framed this talk as the capitalist's case: how Bitcoin reaches its full potential by integrating with every company, country, and capital market in the world. That self-positioning matters, because it signals the speech is a business argument, not a values sermon.

Bitcoin as Capital, Not Currency

Saylor reframed Bitcoin not as money to spend but as the highest form of capital ever created, the longest-duration capital in human history, carrying none of the liabilities of physical assets: no taxes, tenants, corrosion, or political risk. He anchored the claim in hard network figures, a market cap near $1.2 trillion, realized value around $1.1 trillion, backed by 16 gigawatts of power and 940 exahash of computing. "Bitcoin is money, everything else is credit," he said, deliberately echoing the century-old J.P. Morgan line about gold and porting it to the digital age.

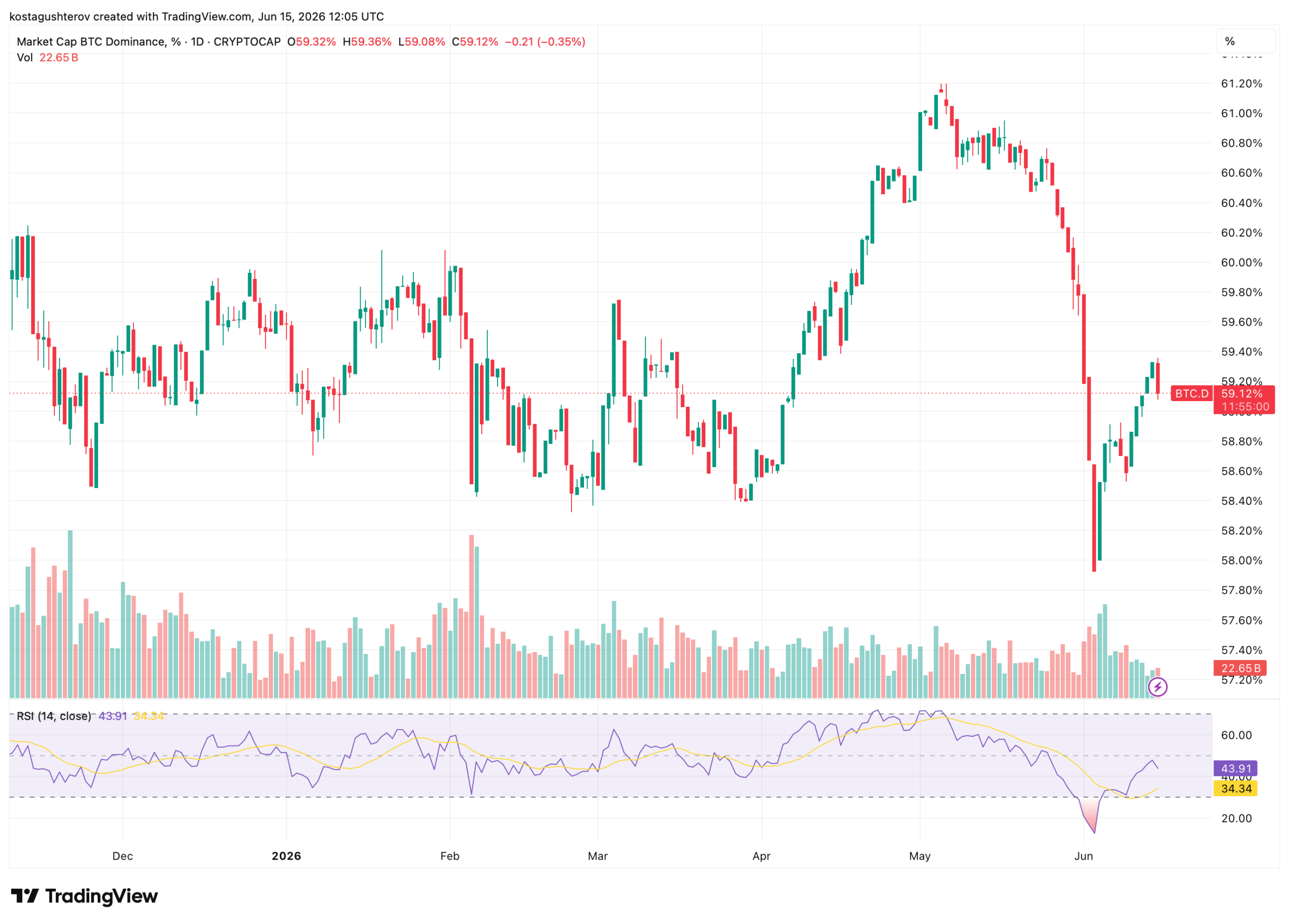

On dominance he was absolute, citing a climb from 40% crypto dominance at the FTX trough back to roughly 68%, "headed towards 70%," with what he sees as no credible rival. Notably, Saylor himself flagged the caveat on stage, conceding the figure is "a little bit less if you exclude the stablecoins." That admission tracks with the standard market trackers: TradingView and CoinGecko place Bitcoin dominance near 59% (59.12% on TradingView's BTC.D metric on June 15, 2026, easing from a May peak above 61%), with the gap to his 68 to 70% figure explained by exactly the stablecoin adjustment he referenced.

The roughly $300 billion in stablecoins sits in the denominator of the standard reading; removing or adjusting for it lifts dominance several points. "There is no close competitor, there is no second best, there is not going to be a flippening." He likened Bitcoin's position to Amazon and Apple around 2010 to 2012, both dominant networks that the mainstream market failed to value correctly until their network effects were already insurmountable.

The Capital Gap Is the Whole Argument

The number anchoring the speech is the gap between what Bitcoin holds and what exists. By Saylor's framing, Bitcoin sits at roughly $1.2 trillion of an approximately $1,000 trillion global capital pool, about 10 basis points; the figure aligns with Bitcoin's market capitalization on trackers like CoinGecko against widely cited estimates of total global wealth across equities, bonds, real estate, and gold. Saylor's entire framework is built on closing it, stepping from 0.1% to 1%, then 2%, 5%, 10%. "If we attract $10 to $20 trillion of that, the Bitcoin network is going to expand to be a $100 trillion network. Your Bitcoin goes from $70,000 to $700,000 to $7 million a coin."

This is where a reader should apply some pressure. The math is arithmetically clean but assumes the migration happens, and the word "inevitable" is carrying enormous weight. The more defensible reading of the speech is not the price target but the structure beneath it: Saylor has stopped arguing that Bitcoin deserves capital and started detailing the mechanics of how capital would actually move, which is a more serious and more falsifiable claim than a price prediction. Underpinning it is what he calls a 10-dimensional model of how capital is stratified, by asset type, custody, jurisdiction, distribution channel, account form, risk, liquidity, investor, and product characteristics, with each cell of that matrix representing capital that needs a purpose-built product to reach.

The Real-Time Footnote: Strategy Sells, Then Buys

After Strategy's last 1,550 BTC purchase from past week, his company put the thesis into action again. In a June 15 post on X, Saylor announced that Strategy had acquired 1,587 BTC for $100 million, lifting its Bitcoin reserve to 846,842 BTC, while also raising its USD reserve by $100 million to $1.1 billion.

Strategy has acquired 1,587 BTC for $100 million to increase our $BTC Reserve to ₿846,842. We have also increased our USD Reserve by $100 million to $1.1 billion. $MSTR $STRC https://t.co/27PYXJN7GD

— Michael Saylor (@saylor) June 15, 2026

The timing matters because of what preceded it. Between May 26 and May 31, Strategy sold 32 BTC for roughly $2.5 million, its first Bitcoin sale since a tax-loss move in December 2022. The disposal, though a rounding error against a treasury of more than 840,000 BTC, was symbolically loud: it appeared to clash with Saylor's long-standing "never sell" mantra, and it sent MSTR shares lower as investors questioned whether the accumulation-only identity was cracking. Saylor addressed it directly at Prague, clarifying that the "never sell" advice was always meant for individual holders, not for a public company with dividend obligations and a fiduciary duty to manage its capital structure. The proceeds, he noted, went toward distributions on Strategy's preferred stock.

Seen together, the sale and the purchase illustrate the exact mechanism Saylor described on stage. The product layers he champions, the dividend-paying credit and money instruments, create obligations that occasionally require selling a sliver of Bitcoin, while the capital those products raise funds far larger purchases. A 32 BTC sale to cover dividends followed by two bigger BTC buys in 2 weeks is not a contradiction; it is the four-layer model running in miniature, with credit instruments feeding the digital-capital base underneath them.

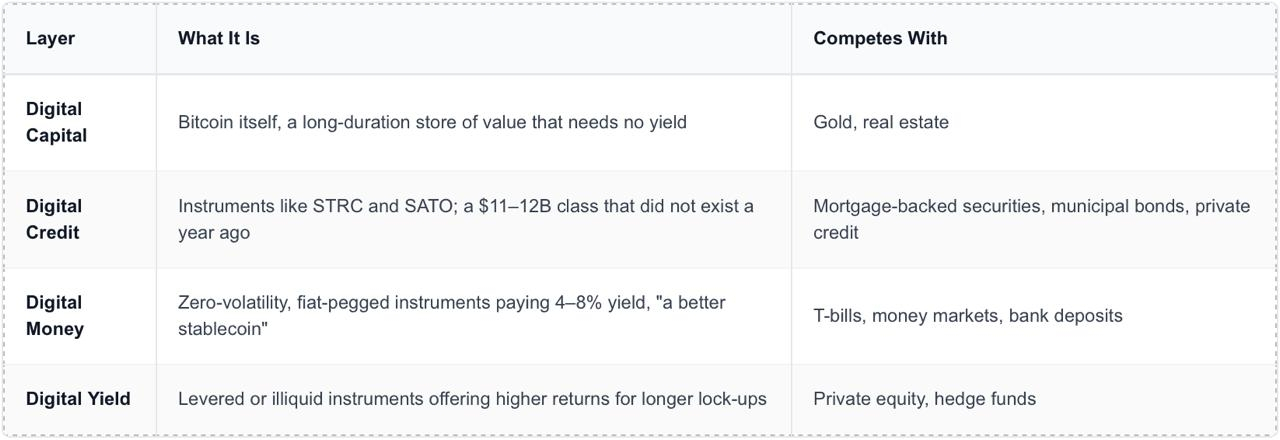

The Four-Layer Economy: The Substance

The most concrete part of the talk was a framework dividing the Bitcoin economy into four product categories, each built to compete with a specific conventional instrument.

On Digital Money specifically, Saylor pointed to $350 billion sitting in stablecoins earning zero as the immediate target, arguing that audience already accepts stability for nothing and would take the same stability with a Bitcoin-backed yield. The digital-credit figure is the one worth watching, because unlike the price targets it is checkable. An asset class going from zero to roughly $11 billion in a year is the kind of measurable traction that either continues or stalls, and it is a better gauge of whether the thesis is working than the coin price.

Why the Aluminum Story Is the Real Point

Saylor's sharpest passage was an analogy. Nobody buys aluminum because they believe in aluminum; they buy an airplane ticket. "The way to sell aluminum to the world is not to preach the merits of the commodity. You create an airplane." Bitcoin, in this telling, spreads not through ideology but through products people fall in love with, insurance policies, pension products, credit instruments, money-market equivalents, that happen to run on Bitcoin without the buyer needing to know or care. "People are going to buy the product. It's going to be powered by Bitcoin. And it will delight them."

This is the genuinely new emphasis, and it doubles as a quiet admission. The implication is that direct Bitcoin evangelism has reached its ceiling: the people persuadable by argument have already bought. As he put it, the people who think for themselves already bought Bitcoin and are already in the room, so the task is to reach the capital that still disagrees. For an audience that prizes conviction, telling them conviction is no longer the growth lever is a pointed message.

https://www.youtube.com/watch?v=r2X04I6yGdY

The Scale, and the Catch

Saylor closed by mapping the barriers as opportunities: 664,000 jurisdictions with different laws, $200 trillion in bank capital that cannot currently touch Bitcoin, insurance companies locked out, retirement accounts still barred from direct exposure. Each, in his framing, is a product waiting to be built, requiring what he estimated as 100,000 corporate efforts to create the roughly 10,000 products the world needs.

The catch sits inside the optimism. Every one of those barriers is regulatory, and regulation does not yield to product design alone. The same speech that frames 664,000 jurisdictions as 664,000 opportunities is also describing 664,000 separate legal fights, and the timeline for those is measured in years, not quarters. Saylor's framework is coherent and, in the digital-credit numbers, already showing early proof. Whether it compounds into the migration he describes depends less on the products being built than on the regulators and institutions that have so far kept the capital out, which is the one variable his framework cannot itself control.