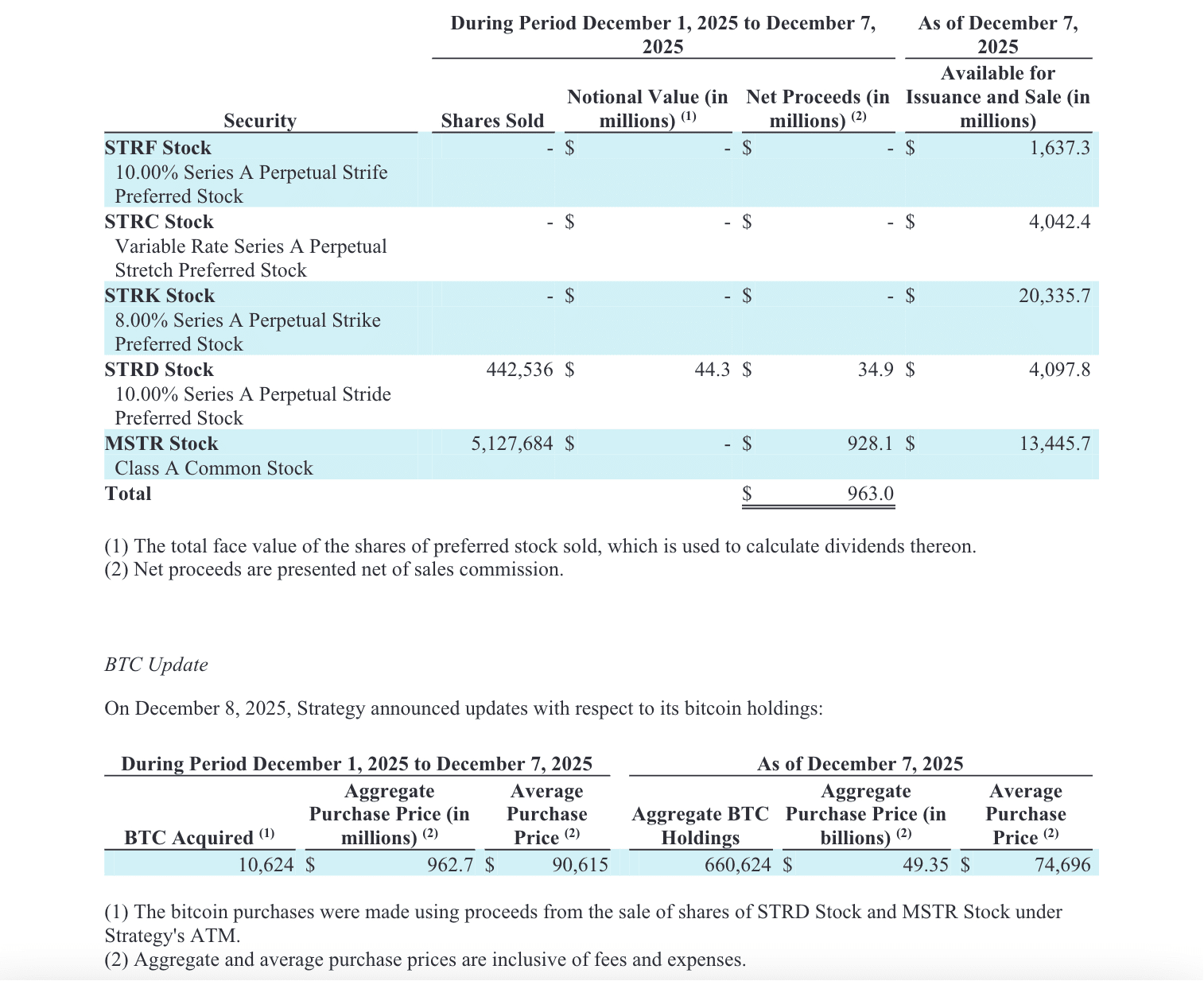

According to the Form 8-K document submitted by Strategy to the SEC, as of December 7, 2025, Strategy holds a total of 660,624 Bitcoins, with a cumulative cost of approximately $49.35 billion, and an average cost of about $74,696 per coin. The annualized return on Bitcoin (YTD 2025) has reached 24.7%. The funds for these purchases came from the sale of STRD and MSTR stocks in the company's ATM financing.

This significant increase in holdings indicates that the financing 'infinite bullet' model adopted by Strategy has not been completely restricted.

This significant increase in holdings indicates that the financing 'infinite bullet' model adopted by Strategy has not been completely restricted.

Previously, Strategy announced the establishment of a $1.44 billion cash reserve at the beginning of this month to pay preferred stock dividends and interest on existing debt. This decision has made Strategy controversial among the market and Bitcoin investor community. Many believe that Strategy did not 'buy the dip' when Bitcoin prices fell, but instead chose to build up cash reserves, which clearly deviates from the long-term investment philosophy that the company has always promoted.

Faced with a flood of questions, Strategy's recent large-scale increase in Bitcoin holdings can perhaps be seen as a silent yet powerful response. However, this increase also raises a question: is this merely a continuation of Strategy's consistent long-term buying strategy, or is it a positive signal to the market that it is optimistic about the near-term trend of the crypto market?

Furthermore, it's worth noting that while this increased holding has injected a boost into the market and improved market confidence to some extent, many of the challenges currently facing Strategy have not been fully resolved. Given this context, how will Strategy develop going forward?

Strategy: The Multiple Dilemmas Behind the Loss of Confidence

The market's gradual loss of confidence in Strategy is due to a variety of reasons, among which the slowdown in Bitcoin accumulation, falling stock prices, and limited financing have had the greatest impact.

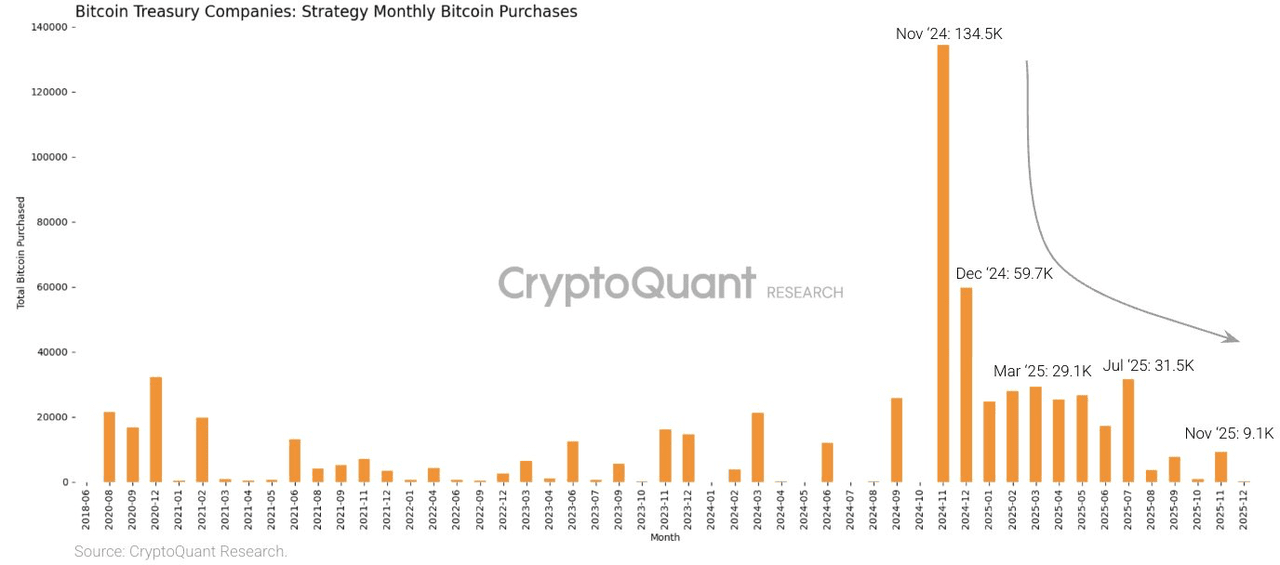

As of December 8th, Strategy has accumulated over 210,000 Bitcoins this year, bringing its total to 214,224. This figure is somewhat respectable; however, a closer look reveals a clear decline in Strategy's Bitcoin purchasing power.

According to CryptoQuant's monitoring, Strategy's Bitcoin purchases plummeted in 2025, with monthly purchases dropping from a peak of 134,000 Bitcoins in 2024 to 9,100 Bitcoins in November 2025. This decline in purchasing activity has become particularly pronounced since August. While it might have been understandable previously that Bitcoin's high price made further purchases unsuitable from a cost and risk perspective, the fact that Strategy, as the largest DAT company in the crypto industry, slowed its Bitcoin accumulation while Bitcoin prices continued to fall, and the market widely expected Strategy to "buy the dip," undoubtedly reflects a lack of confidence in the market. This directly impacted the sentiment of other DAT companies and institutional investors, hindering Bitcoin's upward movement and potentially leading to greater downward pressure.

So why hasn't Strategy bought Bitcoin recently? This is largely due to changes in its stock price and funding situation.

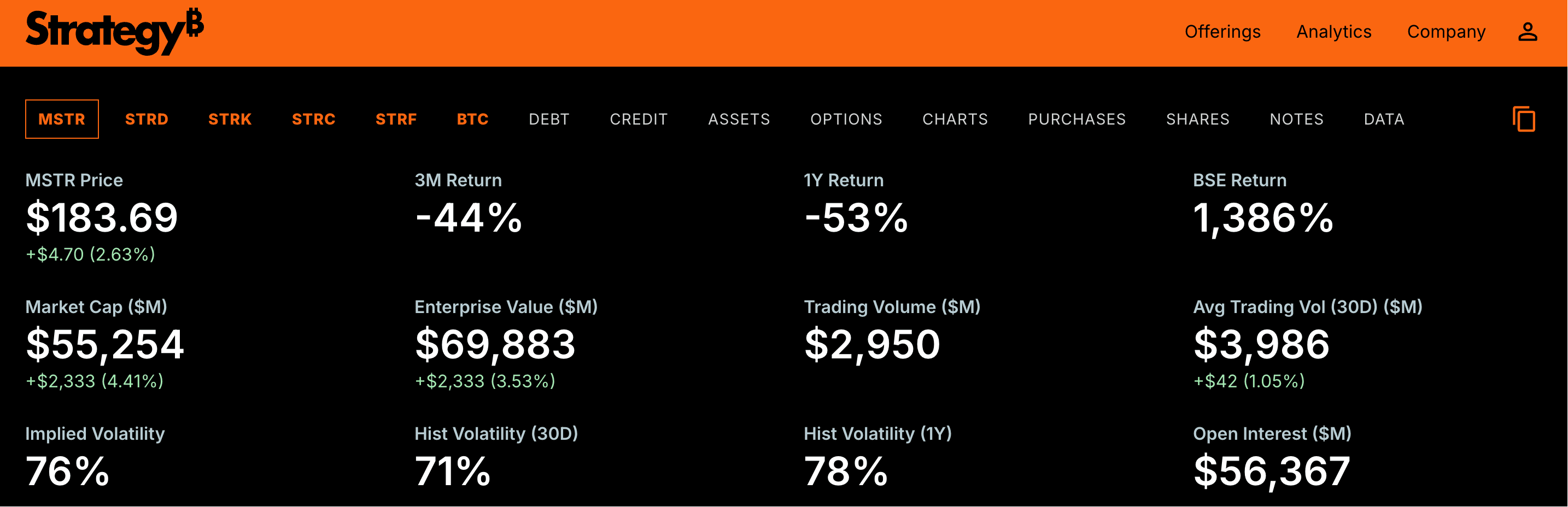

Market data shows that as of the time of writing, Strategy (MSTR) shares were trading at $183.69, down nearly 60% from their high of approximately $457 this year.

The direct impact of the declining stock price is that it has hampered Strategy's fundraising capabilities. Strategy announced the "21/21 Plan" fundraising initiative at the end of October 2024, aiming to raise $42 billion in new capital over the next three years to purchase Bitcoin.

As is widely known, Strategy's ability to continuously increase its Bitcoin holdings in the first half of this year stemmed from its ATM equity financing plan. The core logic of this plan is that when Strategy's stock price has a premium relative to its Bitcoin holdings, the company can raise funds by issuing new shares to increase its Bitcoin holdings.

This relates to Strategy's net asset value ratio (mNAV, the ratio of a company's market capitalization to the value of its Bitcoin holdings). Previously, Strategy's mNAV had reached over 2.5, reflecting a very high premium the market paid for its "stock issuance to buy Bitcoin" strategy. However, as Strategy's stock price and market risk appetite declined, this ratio began to decrease. Once mNAV falls below 1, Strategy will find it difficult to obtain funding through its ATM program.

As of December 8th, Strategy's market capitalization was approximately $52.254 billion, with a net monthly NAV of approximately 1.12. While this remains above 1, a concerning aspect is that Strategy's mNAV repeatedly fell below 1 in November. TD Cowen previously noted in a report that Strategy's premium has significantly declined from its peak at the end of last year and is gradually compressing to levels seen in late 2021 and early 2022.

Meanwhile, market sentiment regarding Strategy's future stock performance has shifted somewhat. Analysts at investment bank Cantor Fitzgerald set a 12-month price target of $229 for Strategy stock, a decrease of approximately 59% from their previous estimate of $560. Even though Cantor reiterated its "overweight" rating on MSTR, analysts generally expect Strategy to raise $7.8 billion from capital markets over the next year, down from the previously anticipated $22.5 billion.

Furthermore, JPMorgan Chase believes that Strategy's ability to maintain an mNAV above 1 and avoid dumping Bitcoin is a key driver of Bitcoin's recent price movement. This view reflects Strategy's Bitcoin centralization and the potential risk of a Bitcoin sell-off, a focus of recent market attention. Currently, Strategy holds approximately 3.14% of the total Bitcoin supply; a significant sell-off would undoubtedly trigger a chain reaction, leading to a market crash.

However, there's no need to be overly concerned about this potential risk. Strategy CEO Phong Le explicitly stated on the show "What Bitcoin Did" that the company would only consider selling Bitcoin as a "last resort" if its mNAV fell below 1 and it couldn't secure new funding. He emphasized that this wasn't a long-term policy shift or a proactive sell-off plan, but merely a "financial decision" to be made in extreme market and capital environment deterioration.

Strategy's move to acquire over 10,000 bitcoins through ATM financing demonstrates that the company is far from being "at its wit's end."

In addition, global securities index issuer MSCI is considering a rule that could exclude companies with more than 50% of their balance sheets comprised of digital assets from its main indices, and Strategy (MSTR) happens to be among those companies. This matter has sparked heated discussions in the industry. JPMorgan Chase stated that if MSTR is removed from mainstream indices such as MSCI USA or the Nasdaq 100, it could trigger an outflow of up to $2.8 billion in funds. Coupled with sell-offs by passive funds, the impact could be further amplified.

MSCI is expected to make its decision on January 15, and if other index providers follow suit, the resulting capital outflow could reach as high as $8.8 billion. According to Reuters, Strategy is in talks with MSCI regarding a potential removal from the MSCI index.

A long-term Bitcoin holding strategy seeking "balance"

Faced with these challenges, it's crucial to first clarify that Strategy's stance on Bitcoin is unwavering. Phong Le has explicitly stated that the company will hold Bitcoin until at least 2065, maintaining its long-term accumulation strategy.

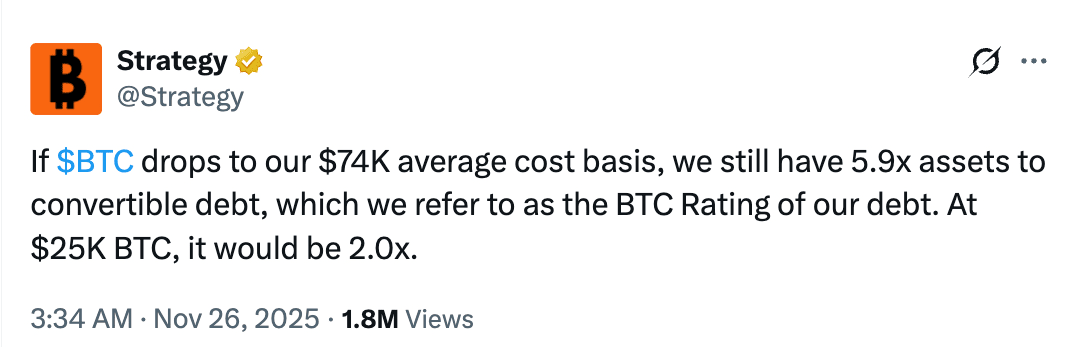

Strategy tweeted that even if Bitcoin falls to its average cost price of $74,000, its BTC assets would still be 5.9 times its convertible debt. Strategy founder Michael Saylor further emphasized at the event, "Strategy currently has approximately $60 billion in Bitcoin reserves and about $8 billion in debt, which is a fairly low leverage ratio."

Secondly, regarding dividend payments, Phong Le specifically pointed out that Strategy faces an annual dividend payment issue of approximately $800 million. With recently issued preferred stock maturing, the annual obligation is approaching $750 million to $800 million. He plans to prioritize paying these dividends through equity capital raised at a price higher than the mNAV. For this reason, Strategy has launched a $1.44 billion dollar reserve, the purpose of which is to pay dividends rather than sell equity, Bitcoin derivatives, or Bitcoin.

The funds for this dollar reserve come from proceeds from the sale of Class A common stock by the company in accordance with its market offering plan. Strategy plans to maintain a reserve size that covers at least 12 months of dividend payments. Building on this, Strategy intends to gradually increase the size of the reserve, with the ultimate goal of creating a buffer pool capable of covering 24 months or more of dividend payments, without having to use its $60 billion Bitcoin position.

This is undoubtedly a sound defensive strategy and an effective means of mitigating risk. Even though this move has made Strategy highly controversial in the market, it has indeed moved beyond the "blindly buy" phase. In fact, in the current market environment, the strategy of blindly "buying the dip" when Bitcoin falls sharply is no longer applicable to Strategy. The decline in Strategy's stock price is not only accompanied by the decline in Bitcoin, but also by the impact of the Bitcoin ETF market. With the development of US policies and increasingly fierce market competition, Strategy stock, once an important alternative to Bitcoin, is no longer the first choice for institutional investors seeking Bitcoin exposure.

Therefore, Strategy needs to explore a strategy more suitable for its own development and find a good balance between long-term Bitcoin purchases and maintaining normal company operations.

Currently, Strategy appears to be exploring more ways to improve asset utilization. Phong Le has stated that lending Bitcoin is not out of the question, thereby enhancing financial flexibility. Meanwhile, Michael Saylor is actively advocating for governments to develop Bitcoin-backed digital banking systems, aiming to provide high-yield, low-volatility accounts and attract trillions of dollars in deposits.

In addition, Strategy is also working to mitigate potential risks in its Bitcoin custody operations. According to Arkham, to reduce its over-reliance on Coinbase, Strategy is pursuing a diversified custody strategy. As of December 6th, Strategy had transferred approximately 183,900 Bitcoins to Fidelity Custody, representing about 28% of the company's total Bitcoin holdings.

It's worth noting that despite persistent doubts and concerns about Strategy, the overall market remains optimistic about the company. Taking the aforementioned "MSCI removal risk of MSTR" as an example, Bitwise's Chief Investment Officer, Matt Hougan, based on historical experience, points out that the impact of index inclusion and removal on stock prices is far less significant than investors generally fear. Last year, Strategy was included in the Nasdaq 100 index, with passive funds buying approximately $2.1 billion worth of shares, yet "the stock price saw almost no fluctuation." The recent decline in stock price may simply be the market anticipating the possibility of removal, and in the long run, significant volatility is not expected.

JPMorgan Chase holds a similar view, believing that the market has fully priced in the risk of Strategy being removed from the MSCI index, and its share price has already reflected the impact of being excluded from major stock benchmark indices. Furthermore, JPMorgan Chase views the upcoming MSCI decision as a potential catalyst for growth. While removal may lead to some passive capital outflows, a positive decision from MSCI could provide strong upward momentum for both Strategy's share price and Bitcoin's price.

Furthermore, Wall Street brokerage firm Benchmark expressed optimism about Strategy's solvency, believing that the company's debt is manageable and its structure is far more robust than critics claim. They also stated that concerns about Strategy's viability are merely noise that inevitably arises during a Bitcoin price drop.

Before Strategy disclosed its purchase of 10,624 Bitcoins last week, the above viewpoint might have been seen more as a mere attempt to boost market confidence. However, as the market widely expects Bitcoin to begin a new upward cycle early next year, Strategy's latest purchase not only further strengthens market confidence in Bitcoin, demonstrating its belief that "Bitcoin's price will not fall significantly," but also reflects its firm bet on Bitcoin's long-term value. When the market recovers and funds flow in again, Strategy may find itself in a more advantageous strategic position.