Highlights from History

The new guidelines from the OCC and CFTC signal a more friendly stance from the U.S. towards regulated cryptocurrencies, which may accelerate Ripple's process to obtain a national banking license.

A banking license from Ripple, along with access to the Fed, could unlock the adoption of RLUSD, expand the use cases for XRP settlement, and position Ripple as a leading native cryptocurrency bank in the U.S.

The Office of the Comptroller of the Currency (OCC) in the U.S. has issued new guidelines that may reshape how traditional finance interacts with digital assets. The regulatory body stated that banks can now act as intermediaries in cryptocurrency transactions through "riskless principal" activities. This means that a bank can temporarily purchase a crypto asset and sell it to a customer without taking on market risk.

The timing is important. Earlier this week, the Commodity Futures Trading Commission (CFTC) also launched a pilot program allowing bitcoins, stablecoins, and other digital assets to be used as collateral in derivatives markets. Together, these measures could signify a more open stance from Washington regarding regulated crypto activity.

Why is this important for Ripple's banking ambitions?

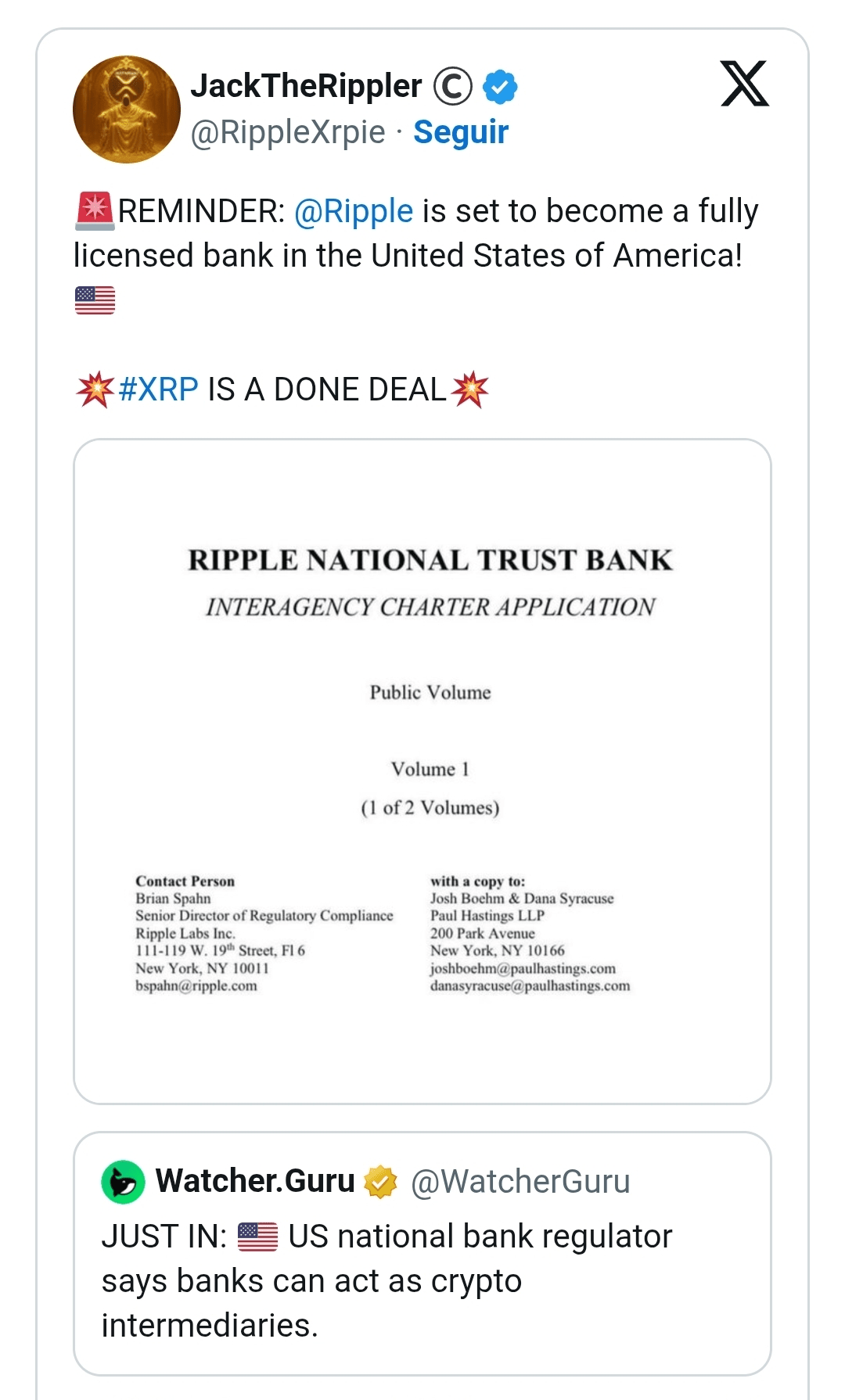

Ripple could be one of the biggest beneficiaries of this change. In July, CEO Brad Garlinghouse confirmed that Ripple applied for a national banking license from the OCC (Office of the Comptroller of the Currency). If approved, Ripple would be subject to state oversight from the NYDFS (New York Department of Financial Services) and federal oversight from the OCC. This would make Ripple one of the first companies in the stablecoin sector to operate with all banking permissions in the U.S.

Garlinghouse also revealed that Ripple applied for a Master Account from the Federal Reserve through Standard Custody. This would allow Ripple to hold RLUSD reserves directly at the Federal Reserve. Direct access to the Fed is rare and would provide Ripple with a stronger foundation to operate RLUSD as a regulated stablecoin ready for institutional use.

Ripple states that its focus is on building a 'reliable, battle-tested, and secure infrastructure.' With the stablecoin market now above $250 billion, the company argues that RLUSD can stand out by placing regulation at the center of its design.

What a banking license could unlock

If Ripple obtains a national banking license, it could custody digital assets, offer lending services, and have direct access to the Fed's systems. This includes FedNow, the U.S. instant payments network. This could increase the number of payment and settlement use cases linked to XRP, especially in international flows.

The license could also give Ripple access to the Federal Reserve's credit line during liquidity crises, a privilege typically reserved for banks. This would make Ripple one of the most rigorously regulated companies in the digital asset market.

Clearer cross-border rules, helping Ripple grow even further.

In a second development, the CFTC (Commodity Futures Trading Commission) enhanced its rules for cross-border swaps. The updated framework reduces uncertainty for institutions looking to settle trades using digital assets. This represents a direct boost for Ripple, whose business model is based on cross-border settlement in compliance with regulations.

Clearer rules, combined with more favorable banking guidelines for cryptocurrencies, lower the barriers for banks to adopt RLUSD and explore XRP-based settlement in a regulated environment.

Is Ripple about to become one of the first native cryptocurrency banks in the United States? Regulatory processes are being implemented.

Remember folks, that nothing said here represents a recommendation to buy, sell, or hold assets.

Thank you all!

\u003cc-49/\u003e