Key points from the speech of the head of the U.S. Federal Reserve, Jerome Powell, after another reduction in the interest rate by 0.25 percentage points.

- Available data suggests that the forecast has not changed.

- Macroeconomic data indicate moderate economic growth. The GDP growth forecast for 2026 has been revised upwards.

- Inflation is still elevated. Inflation for goods has accelerated, while disinflation in the services sector continues. Little data on inflation has been published since October.

- Most long-term inflation expectations align with the 2% target. Risks for inflation are skewed to the upside. Due to rising risks of employment decline, there has been a shift in the balance of risks in recent months.

- The labor market is gradually cooling, and sentiment in the labor market is worsening. The level of layoffs and hiring remains low. Demand for labor has clearly decreased. We have a less dynamic and somewhat softer labor market.

- Risks threaten both of the Fed's goals, creating a challenging situation.

- Labor market data for September showed that the unemployment rate has slightly increased, while job growth has significantly slowed.

- The recent drop in rates should help stabilize the labor market. Rates are in the range of neutral assessments.

- The consequences of the shutdown should be offset by higher growth in the next quarter due to the resumption of operations.

- The Fed believes that reserve balances have declined to a sufficient level.

- The purchase of short-term Treasury securities will be carried out to support effective control over policy rates.

- Consumer spending is stable, and investment in capital goods is expanding.

- The housing construction sector remains weak.

- There is no risk-free path for conducting monetary policy - the Fed will make decisions based on the outcomes of each meeting. Monetary policy does not follow a predetermined course.

We await responses to journalists' questions.

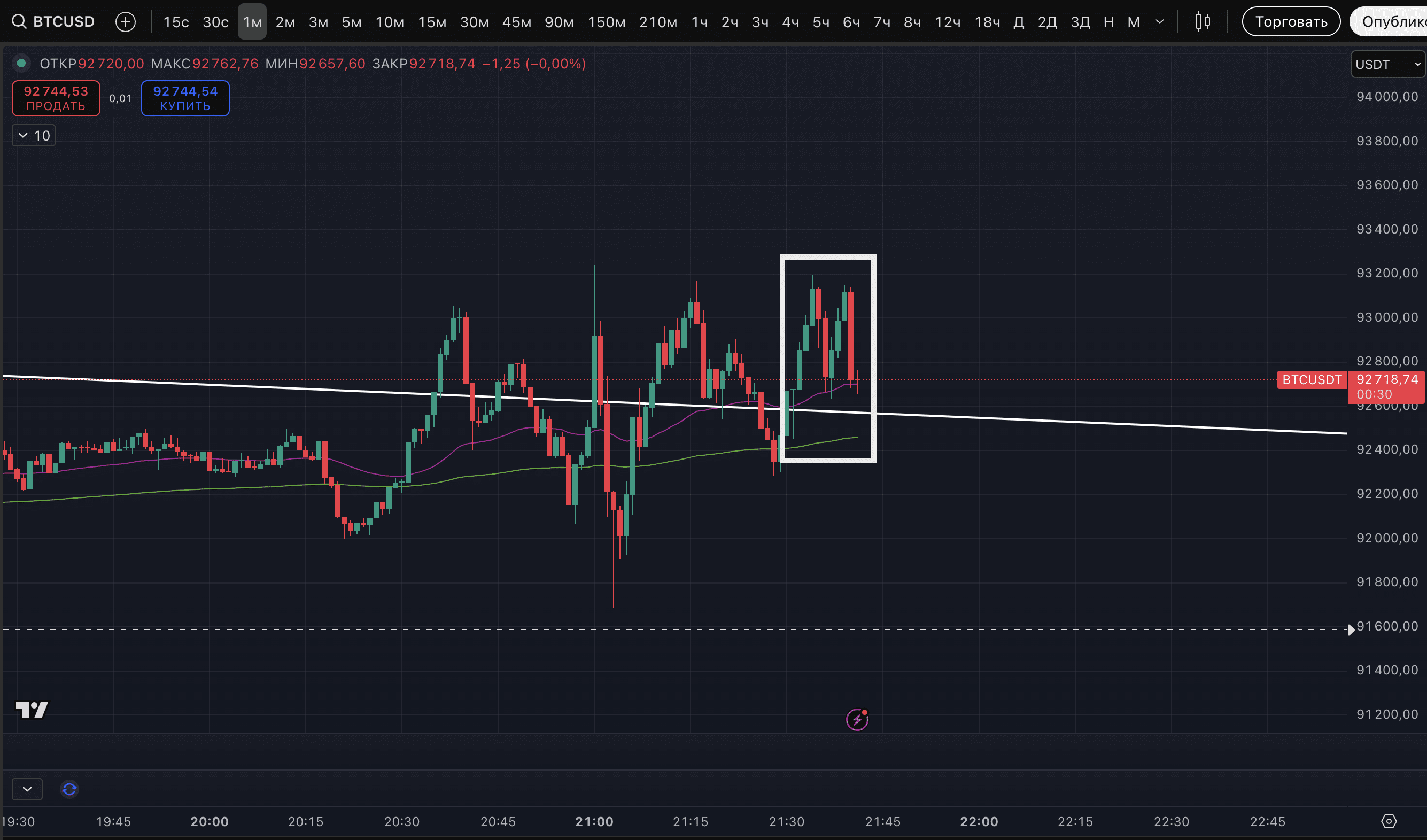

BTC movement during Powell's speech is currently uncertain.