I. Interest rate decision: a scheduled rate cut but internal disagreements are pronounced

I. Interest rate decision: a scheduled rate cut but internal disagreements are pronounced

1. Benchmark interest rate adjustment

● The Federal Reserve's Monetary Policy Committee (FOMC) announced on December 11 at midnight in the Eastern Time Zone that it will lower the target range for the federal funds rate from 3.75%-4.00% to 3.50%-3.75%.

● This is the third rate cut following those in September and October this year, with each cut being 25 basis points. To date, the cumulative rate cut for 2024 has reached 75 basis points.

● Since the start of this round of easing in September 2023, the Federal Reserve has cumulatively cut interest rates by 175 basis points.

2. Rare disagreement among decision-makers

● This interest rate decision faced three dissenting votes, the first since 2019.

● Board member Milan (appointed by Trump) advocates for a 50 basis point rate cut; two regional Fed presidents and four non-voting members support keeping rates unchanged.

● A total of seven officials opposed the resolution, reportedly the largest divergence in 37 years.

3. Key changes in the policy statement

● Interest rate guidance adjustment: The statement no longer vaguely states 'will assess future data, outlook, and risk balance', but clearly changes to 'when considering the magnitude and timing of further adjustments to the federal funds rate target range, the committee will carefully evaluate the latest data, evolving outlook, and risk balance.' This wording is interpreted as setting a higher threshold for rate cuts.

● Labor market description: Removed the expression that the unemployment rate 'remains low', changing it to 'slightly up as of September', while acknowledging that 'the risk of employment decline has increased in recent months'.

● Inflation stance: Maintain the judgment that 'inflation remains slightly elevated', with no substantial softening.

II. Economic forecasts and dot plot signals: Slowing the pace of action

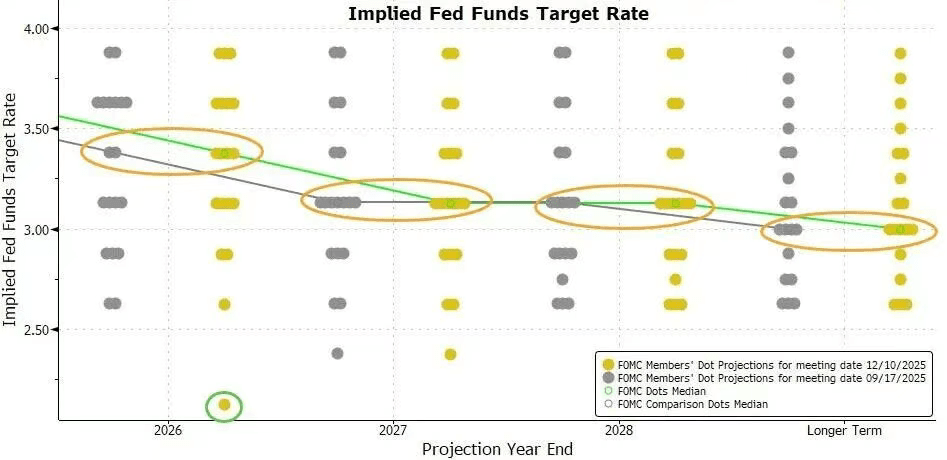

1. Interest rate path forecasts (dot plot)

● The latest dot plot shows that the median interest rate forecast for 2025-2027 among Fed officials is completely consistent with the September forecast.

● Specifically:

○ The end of 2025: The median interest rate forecast is 3.4%, suggesting only one 25 basis point rate cut next year.

○ The end of 2026: The median interest rate forecast is 3.1%.

○ The end of 2027: The median interest rate forecast is 2.9%.

● Among the 19 officials providing forecasts, 7 expect rates to remain in the 3.5%-4.0% range in 2025 (i.e., no rate cut), a decrease of 1 from September.

2. Economic outlook adjustment

● Economic growth: Raised GDP growth expectations for 2024 and the following three years, reflecting recognition of economic resilience.

● Unemployment rate: A slight downward adjustment of 0.1 percentage points in the 2026 unemployment rate forecast, while other years remain unchanged, indicating a more resilient labor market than expected.

● Inflation expectations: Slightly lowered the PCE inflation and core PCE inflation expectations for 2024 and 2025 by 0.1 percentage points, indicating a slight increase in confidence about inflation slowing.

3. Market expectations comparison

● Before the meeting, the CME FedWatch tool showed:

○ The probability of a 25 basis point rate cut in this meeting is close to 88%.

○ The market expects a 71% probability of another rate cut of at least 25 basis points by June 2025.

○ In meetings in January, March, and April 2025, the probability of a rate cut did not exceed 50%.

● This resolution fits the characteristics of a 'hawkish rate cut': implementing a rate cut while suggesting a possible pause in actions afterwards.

III. Reserve management plan: Purchasing short-term bonds to maintain liquidity

1. Operation initiation and purpose

● The Federal Reserve added a paragraph to the statement, announcing that 'the reserve balance has dropped to adequate levels and will begin purchasing short-term Treasury bonds as needed to maintain adequate reserve supply'.

● This operation is defined as reserve management purchases (RMP), aimed at rebuilding liquidity buffers for the monetary market to address possible market pressures at year-end.

● Powell emphasized that this operation is separate from the monetary policy stance and 'does not represent a change in policy direction', with the sole purpose of ensuring the Fed can effectively control policy rates.

2. Specific implementation arrangements

● Start time: Starting this Friday (December 13).

● Initial scale: The New York Fed plans to purchase $40 billion in short-term Treasury bonds over the next 30 days.

● Subsequent arrangements: The purchase scale may remain high in the coming months to alleviate seasonal monetary market tightness; subsequently, it will gradually decrease according to market conditions.

● Background considerations: Banks usually reduce repurchase market activities at the end of the year to meet regulatory and tax settlement demands, which can easily lead to liquidity tightness.

IV. Key points from Chairman Powell's press conference

1. Policy stance calibration

● Patience in waiting: 'Our current position allows us to be patient and observe how the economy will evolve next.'

● Denying rate hike tendencies: Clearly stated that 'not considering that the next action will be a rate hike is not anyone's baseline assumption', emphasizing that they have not heard such viewpoints.

● Risk balance assessment: 'Inflation risks are skewed to the upside, while employment risks are skewed to the downside, which is a challenging situation.'

2. Internal divergence elaboration

● There are three main views within the committee:

○ Some members believe the current policy stance is appropriate, advocating to maintain the status quo and observe further.

○ Some members believe that there may be a need for another rate cut in 2024 or 2025, perhaps more than once.

○ Expectations primarily focus on scenarios of 'maintaining the status quo, slight rate cuts, or larger cuts'.

3. Inflation and employment interpretation

● Tariff impacts: It is believed that the impact of tariffs on inflation is 'relatively short-lived', essentially a one-time price level increase; the Federal Reserve's duty is to prevent it from evolving into a persistent inflation issue.

● Labor market: Pointed out that although the official employment data for October and November has not been released, existing evidence shows that both layoffs and hiring activities are at low levels; households and businesses' views on the labor market continue to cool.

4. Asset purchase clarification

● Reiterated that short-term Treasury bond purchases are an independent decision and not quantitative easing (QE), not changing the monetary policy stance.

● Indicated that monetary market tightness 'came a bit quicker than expected', but not strictly a 'concern'.

V. Market analysis and outlook

V. Market analysis and outlook

1. Policy path assessment

● This meeting conveys a clear signal: The Federal Reserve is about to enter an observation period after three consecutive rate cuts.

● The dot plot shows that only one rate cut is expected in 2025, in sharp contrast to three rate cuts in 2024, indicating a consensus on slowing the pace of action.

● The new wording of 'considering magnitude and timing' sets a higher threshold for future policy adjustments, potentially requiring clearer evidence of labor market weakness.

2. Economic environment assessment

● The Federal Reserve faces a balancing challenge between inflation and employment:

○ The process of inflation retreat has stalled, limiting further easing space.

○ Signs of cooling in the labor market appear, caution against downside risks.

● Economic forecasts raised growth, lowered inflation, reflecting an increased possibility of a 'soft landing', but uncertainty remains.

3. Initial market impact

● After the resolution announcement, the short end of the US Treasury yield curve reacted mildly, while the long end dipped slightly, reflecting the market digesting the expectations of a slowed rate cut.

● The US dollar index remains relatively strong, with limited stock market fluctuations, indicating that the market generally accepts the 'hawkish rate cut' narrative.

● Reserve management operations are expected to alleviate year-end liquidity pressures, avoiding a repeat of the 2019 repurchase market turmoil.

4. Future focus

● Data dependence: Subsequent policies will heavily rely on inflation (especially core PCE) and employment data performance.

● Internal coordination: How to bridge the internal divergence within the decision-making body and form a more unified forward guidance.

● External risks: The impact of global economic growth trends, geopolitical developments, and changes in financial conditions.

● Technical operations: Adjustments to the actual scale and pace of reserve management purchases, and their effects on stabilizing monetary market rates.

This Federal Reserve meeting completed the third rate cut as expected, but through dot plot forecasts, adjustments in the wording of the policy statement, and the chairman's remarks, it clearly conveyed signals to slow the pace of easing.

The rare divergence among decision-makers highlights the difficulty of balancing inflation resilience and cooling employment. Meanwhile, initiating short-term Treasury bond purchases to manage reserves indicates the Fed is taking precautionary measures to address structural pressures in the monetary market.

Join our community to discuss and become stronger together!

Official Telegram community: https://t.me/aicoincn

AiCoin Chinese Twitter: https://x.com/AiCoinzh

OKX benefits group: https://aicoin.com/link/chat?cid=l61eM4owQ

Binance benefits group: https://aicoin.com/link/chat?cid=ynr7d1P6Z