The Office of the Comptroller of the Currency (OCC) released an investigation report this morning on 12/11, stating that from 2020 to 2023, the nine major banks in the United States have implemented account closures or restrictions on financial services for several politically controversial industries, including the cryptocurrency industry. The OCC pointed out that some banks continue to distinguish between compliant industries, requiring additional scrutiny or directly limiting transactions, which involves unreasonable discrimination. In the future, they will hold these behaviors accountable and ensure that illegal account closures do not continue.

Banks have raised service thresholds for specific industries, and the OCC accuses them of unreasonable discrimination.

The OCC pointed out that between 2020 and 2023, several major banks in the U.S. raised the thresholds for account opening and providing financial services, even directly refusing transactions, citing customers' engagement in "politically controversial legal businesses" as the reason.

OCC certification, these practices are not only unreasonable but also involve discrimination, as the responsibility of banks should be based on risk rather than the political sensitivity of the industry itself. This investigation was initiated because in August of this year, U.S. President Trump signed an executive order requiring a review of whether banks have taken account closure actions due to customers' political, religious, or other non-risk factors. The OCC's investigation is conducted under this executive order.

(Wall Street Journal: Trump plans to sign an executive order to halt Chokepoint 2.0, supporting the crypto industry against bank discrimination)

The crypto industry is also heavily affected, with multiple controversial industries similarly impacted.

The OCC further explained that the industries listed as restricted from banking relationships are not limited to the cryptocurrency industry. The report pointed out that oil and gas exploration, mining, firearms-related industries, private prisons, tobacco and e-cigarette manufacturers, and adult entertainment operators are all on the restriction list.

In the crypto industry, the OCC stated that banks not only restrict cryptocurrency issuers but also adopt the same attitude towards exchanges and management. Banks usually classify reasons as "preventing financial crime" or "compliance risk review," thus raising the threshold for relevant operators to obtain financial services.

OCC Director Jonathan Gould expressed regret, believing that it is inappropriate for the largest banks in the U.S. to use their licenses and market power to push these account closure policies.

(U.S. OCC: Fully end de-banking and reputational risks, assist the development of crypto banking business)

The nine major banks are the subjects of the investigation and will continue to pursue legal accountability.

The OCC examined the nine largest commercial banks in the U.S. during this investigation:

JPMorgan

Bank of America

Citibank

Wells Fargo

U.S. Bank

Capital One

PNC Bank

TD Bank

BMO Bank

These banks are the most influential institutions in the U.S. financial system, thus the investigation is receiving high attention. The OCC stated that the investigation is not yet over and is continuing to gather more evidence and pursue legal accountability.

(Strike CEO was closed by JPMorgan, U.S. Senator warns Chokepoint 2.0 may resurface)

The OCC report still has gaps, not covering other sources of regulatory pressure

Nick Anthony, a policy analyst at one of the five major think tanks in the U.S., the Cato Institute, stated that this report still has many parts that need to be supplemented. He pointed out that the report criticizes banks for cutting off controversial customers but does not mention that regulators themselves require banks to assess "reputational risks," which may also be one of the reasons banks take action.

He also mentioned that the report claims banks restrict crypto services, yet does not mention that the "Federal Deposit Insurance Corporation" (FDIC) had explicitly warned banks to avoid dealings with crypto operators. Additionally, the Republican chairman of the U.S. House Financial Services Committee, French Hill, previously pointed out that the "pause letters" sent by the FDIC during the Biden administration made banks maintain more distance from crypto operators, further reinforcing the so-called "crypto account closure."

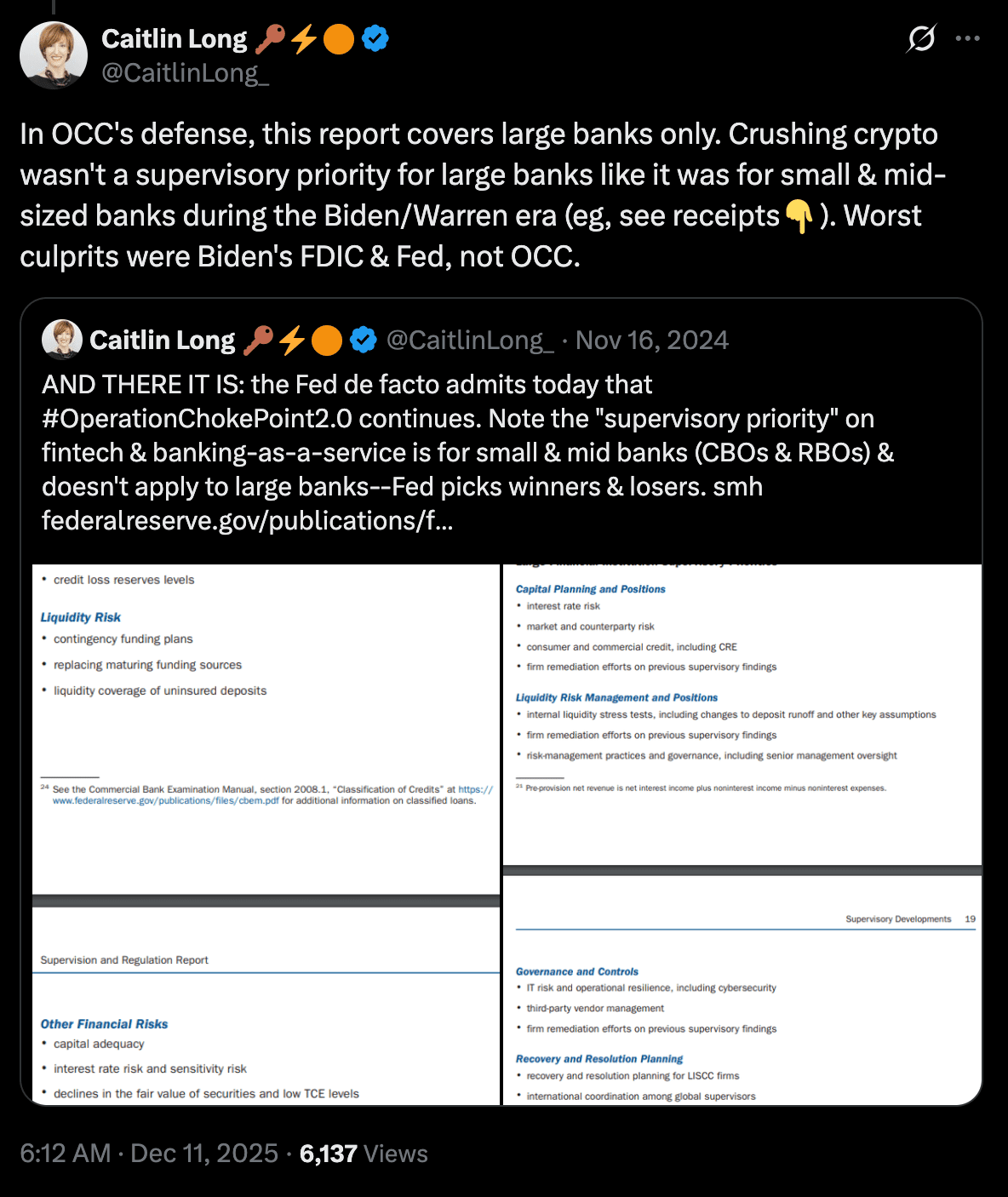

The real pressure comes from the FDIC and the Federal Reserve, not the OCC

Caitlin Long, founder of the U.S. crypto-friendly bank Custodia Bank, also commented on the report. She believes that the unit responsible for the most severe account closures against the crypto industry during the Biden administration is not the OCC, but the FDIC and the U.S. Federal Reserve (Fed).

She stated that this OCC report only targets large banks, but the greatest pressure on the crypto industry in the past actually came from the FDIC and the Federal Reserve's covert pressure on small and medium-sized banks, leading these banks to distance themselves from crypto-related businesses.

(JPMorgan's Dimon: Current regulations force banks to close accounts, not political and religious factors)

This article from OCC: JPMorgan, Citigroup, and other nine major banks suppressing the crypto industry will continue to pursue legal accountability. It first appeared in Chain News ABMedia.