Imagine a typical extreme market scenario:

A macro black swan is coming, the sentiment index soars, and the group chat only has two words—'liquidate.'

The instinctive reaction of many users is to immediately convert all non-USDT assets back to 'cash,' frantically clicking Redeem in every protocol.

But in the logic of FalconFinance's sUSDf vault, users will hit a 'soft wall':

Redemption requests need to go through a 7-day cooling period (about 168 hours) to be completed.

On social media, this kind of design can easily be criticized as 'fund kidnapping';

But if you have reviewed the collapses of UST / various vaults during runs, you'll understand—

These 168 hours are more like an 'ABS anti-lock braking system' coded into the system:

When everyone slams the brakes simultaneously, try to avoid the whole car tipping over directly.

One, why can't FalconFinance let you 'redeem instantly'?

On the surface, sUSDf looks like a 'savings and earning' DeFi product;

But from the asset-liability structure perspective, sUSDf is closer to a cross-chain on/off-chain structured fund:

Asset side:

Hold spot, hedge short positions, arbitrage positions in CEX (such as Binance, Bybit, etc.);

May also add some RWA / notes / market making strategies.

Liability side:

The on-chain sUSDf shares can be redeemed at any time by user requests.

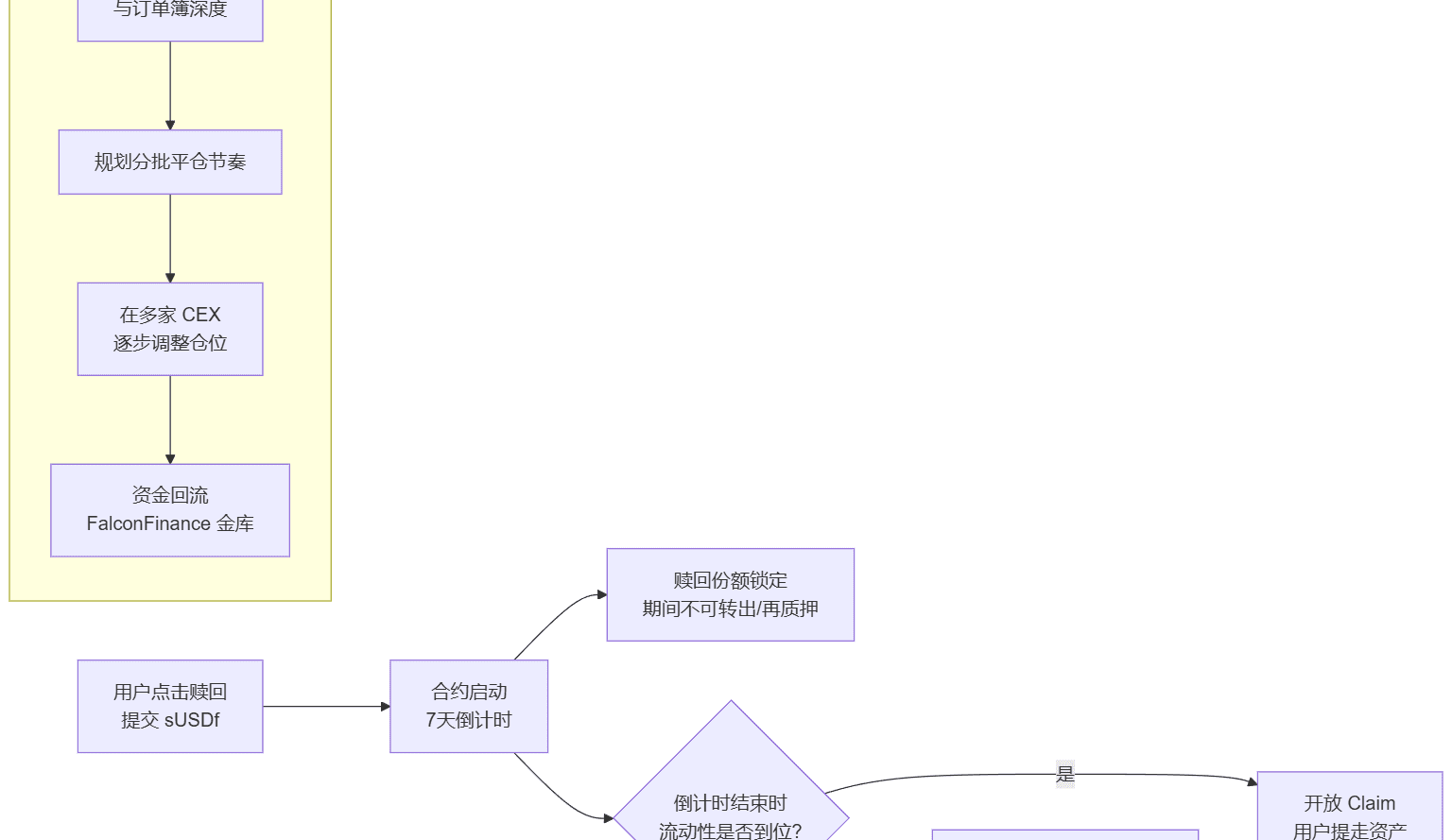

When you submit a redemption in FalconFinance, FalconFinance is not simply 'taking some money out' from the treasury, but needs to complete a series of real operations:

Liquidate related positions in batches across multiple CEXs (Unwind Positions);

Consider trading depth to avoid smashing prices into the market at the worst liquidity;

Bound by CEX withdrawal limits, bank settlement cycles (T+1 / T+2), and other real constraints;

Funds must return to the chain to finally complete the redemption.

If no cooling period is set, allowing billions of dollars to surge towards exits in panic, FalconFinance can only liquidate all positions at the worst prices and worst liquidity:

Panic redeemers may receive payouts far below intrinsic value;

Users who remain in the pool bear the losses from being impacted by 'spillover risks'.

The 7-day cooling period is essentially FalconFinance's engineering answer to the asset-liability mismatch problem:

Using time buffers to trade for a smoother exit closer to fair value.

Two, from a professional perspective: what problem does FalconFinance's 'liquidity buffer' solve?

There is an old problem in traditional finance: short-term redeemable + long-term investment = term mismatch.

Banks use demand deposits to buy long-term bonds;

Money market funds promise 'T+0 / T+1 redemption', but behind this is T+N assets;

When everyone comes together to withdraw money, assets are forced to be sold at the wrong time.

FalconFinance is making a very clear trade-off:

Not pretending to be 'instant deposit and withdrawal', nor hiding the real positions across CEXs / cross-markets;

By implementing a 'redemption cooling period' at the contract level, term mismatch is made explicit:

Want high returns + complex strategies → must accept a 7-day exit period;

Don't want to bear this time cost → use USDT / other highly liquid assets.

This has two important effects for FalconFinance:

Give the trading and risk control teams a time window

to reduce positions in batches according to market fluctuations, rather than a one-price suicide liquidation;

Can prioritize handling leverage, hedging, and highly correlated positions to reduce systemic risk.

Screening funding structures

Short-term panic funds will naturally reduce participation in FalconFinance;

More allocation-oriented, institutional long-term funds are more willing to accept such constraints.

FalconFinance uses a cold 'T+7 rule' to publicly place the liquidity risks originally hidden in the black box on the table.

Three, what has FalconFinance done behind the scenes in 168 hours?

From the user's perspective, there are only two things:

Clicked Redeem;

Wait 7 days;

During this time, a complete scheduling system is actually working at FalconFinance's core.

This diagram reflects several key design points of FalconFinance:

Locking, not disappearing:

Redeemed shares are 'marked' and locked by contracts, no longer participating in new profit distributions, and cannot be transferred to others;

Risk control is continuous, not a one-time shot:

FalconFinance reduces positions in batches under different exchanges and market conditions, rather than dumping all positions at the worst moment;

What if there is still a gap after 7 days?

In ideal design, FalconFinance would reserve risk buffers / insurance pools to fill short-term gaps in extreme situations, avoiding users directly bearing the 'systemic run on the bank discount'.

For users, this process only has one intuitive feeling:

Time has been extended, but the quality of redemption is more guaranteed.

Four, conflict in user experience: instant gratification vs payment security

The on-chain world of 2025 has trained everyone's expectations to be extremely extreme:

L2 second-level confirmation

DEX real-time transactions

Wallet balances refresh in real time

Against this experience baseline, FalconFinance's '7-day wait' will certainly seem very discordant.

But from a financial engineering perspective, this is a typical three-choice-two problem:

High yield (Yield)

High liquidity (Liquidity)

High security (Security)

FalconFinance's options are:

Provide stable returns + risk resistance as much as possible;

Clearly tell users that liquidity is not 'instant', but 'rhythmic T+7'.

This is equivalent to a public 'social contract':

Do you want 'instant entry and exit + high returns'? Such long-term sustainable products probably do not exist in the world;

If you are willing to accept 'returns + safety', then FalconFinance asks you to pay the 'time cost' for it.

In the long run, FalconFinance uses this mechanism to block out short-term funds that 'withdraw at the slightest wind' and 'only take a bite before leaving',

which instead creates a more stable return environment for truly willing long-term allocation funds.

Five, compared to CEX's 'pulling the plug', FalconFinance at least provides a predictable timeline

Many people will ask:

'Can't I just open a position and arbitrage on CEX, thus avoiding the 7-day cooling period?'

The problem is:

No rules ≠ more freedom; many times it simply means 'more uncertainty'.

In extreme market conditions, you have seen too many times:

CEX pauses withdrawals;

Certain trading pairs are temporarily removed;

Users in some regions are subject to risk control;

Withdrawal review queues take days or even weeks.

These 'cooling periods' are completely black-boxed:

Not written in any smart contract;

No transparent end time;

Completely depends on the platform's own discretion.

FalconFinance's approach is:

Clearly state the cooling period in advance, written into the contract logic;

Every redemption request has a clear timeline and processing rules;

FalconFinance converts the 'indefinite cooling' that may occur at any time in CEX into a predictable 'limited countdown'.

For many users who have experienced FTX / various withdrawal suspension incidents,

predictable slowness is safer than unpredictable 'might never come out'.

Six, in the world of FalconFinance, 'slow' is a form of risk management, not procrastination.

168 hours sounds long,

But in the whole risk cycle, it is actually doing three things:

Leave operational space for FalconFinance's trading and risk control;

Give emotions time to return from extreme panic to rationality;

Use visible rules to replace invisible human intervention.

For FalconFinance, this is a proactive system design choice:

Not catering to the short-term impulse of 'give me all liquidity immediately';

But rather leaning towards 'let the protocol survive the next black swan'.

For you using FalconFinance, this is also a simple but important question:

Do you care more about 'freedom of withdrawal in the next hour',

or 'in the coming years, will this protocol still exist'?

In an era where everyone is chasing 'faster',

FalconFinance uses a 168-hour period that many criticize as 'slow',

to provide another answer:

Sometimes,

putting panic into an 'anti-lock braking system'

is the real protection for your capital.

I am a sword seeker, an analyst who focuses only on essence and ignores the noise.@Falcon Finance $FF #FalconFinance

(This article is an analysis of mechanisms and risk structures and does not constitute any investment advice or guarantee of returns. Before using FalconFinance, please fully understand the product terms and liquidity rules, and make decisions based on your own risk tolerance.)