We have all seen it, during festivals when people show off their red envelopes and transfers, they are all competing on: who has the larger amount!

However, today, if you do not love someone and hate them instead, then just transfer 250 yuan to their bank card with the note: Dogecoin. That's enough!

This is not a joke, this really happened a few days ago.

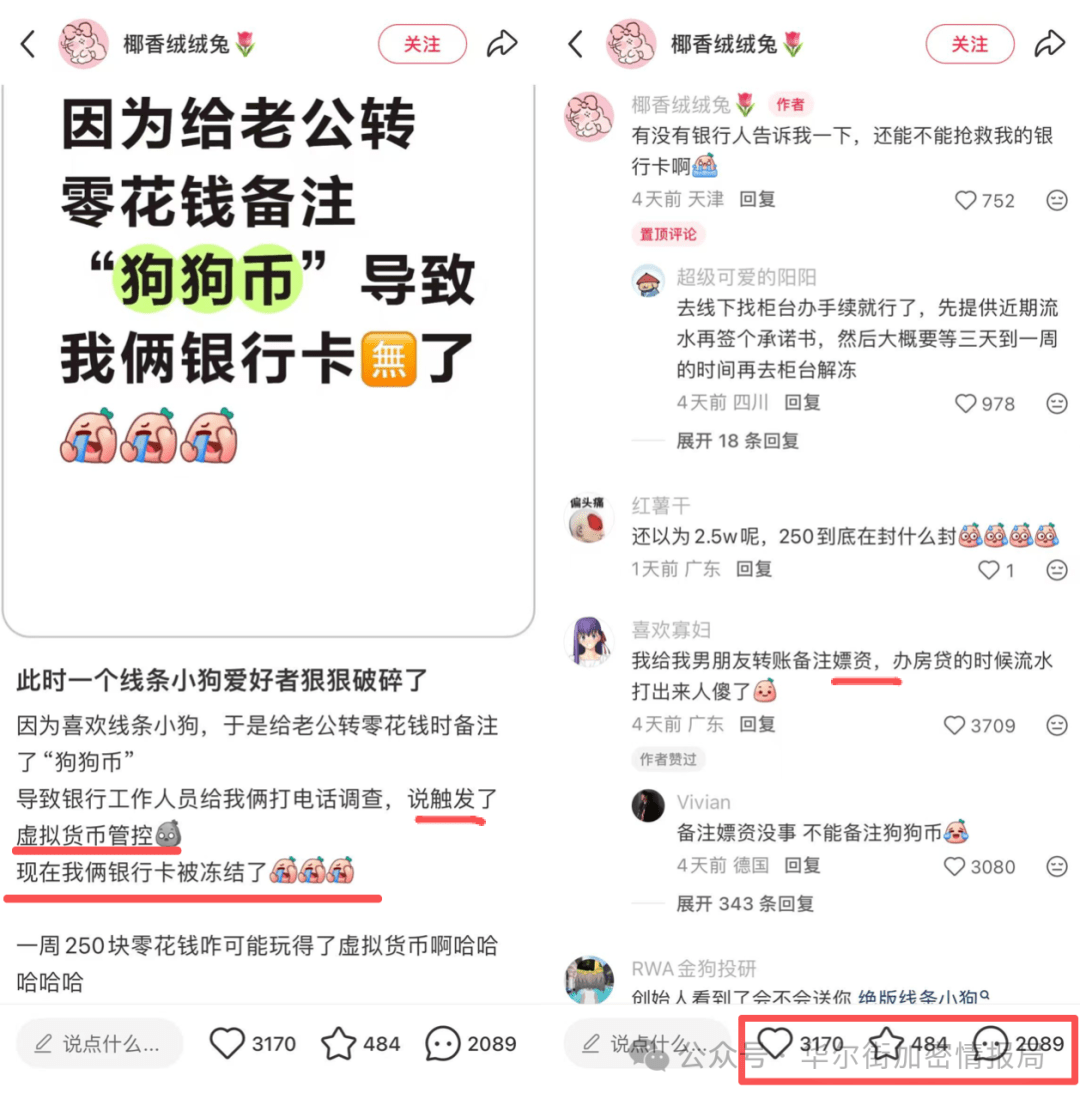

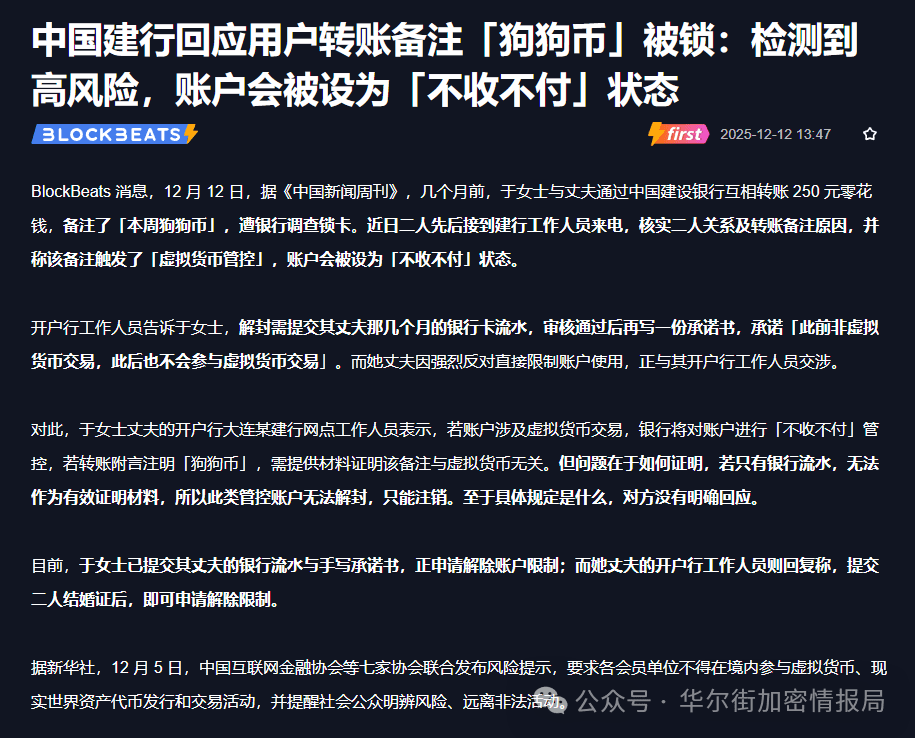

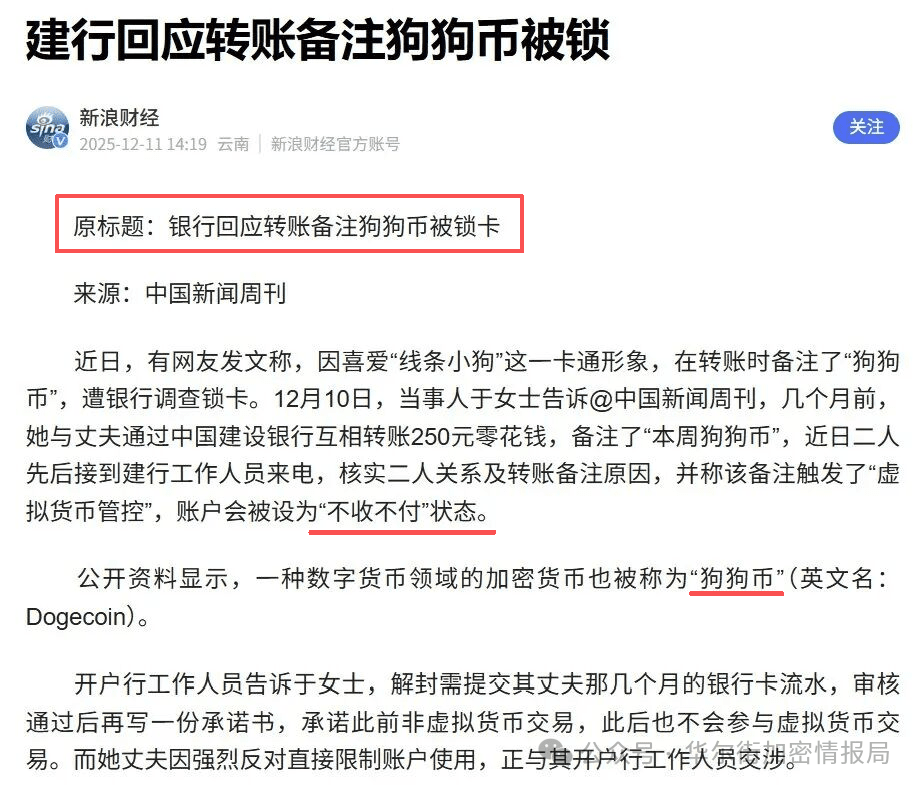

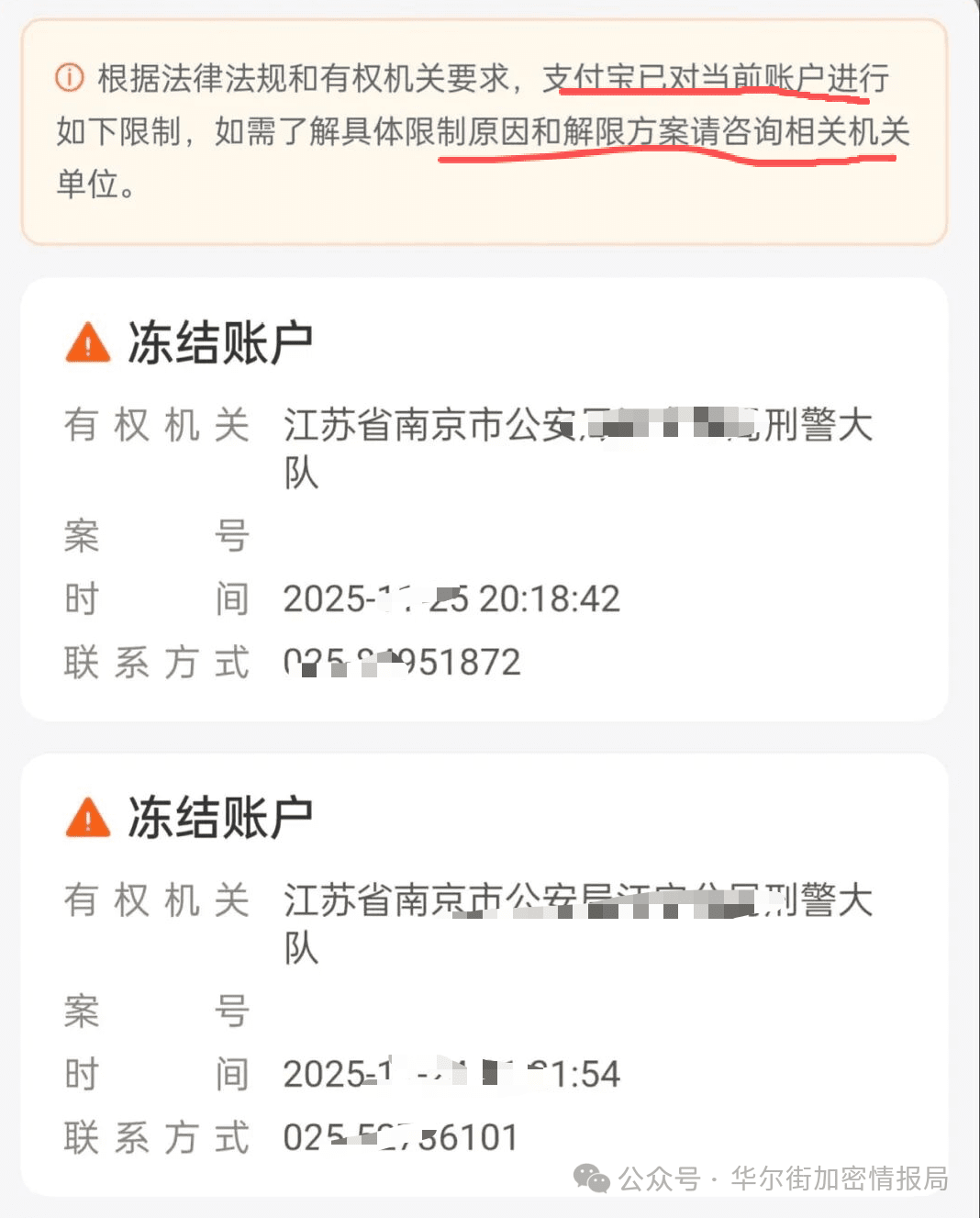

Ms. Yu from Dalian transferred 250 yuan to her husband through Construction Bank, with a note: Dogecoin, and then was put under lockdown, directly freezing both parties' bank cards.

The latest response from China Construction Bank is:

The amount is not large, there is no fraud, no money laundering, no virtual currency transaction records, and the two parties know each other. It was just because of an unintentional note that both spouses' bank cards were frozen.

This is not the first time we have witnessed a powerful risk control system!!!

Has regulation always been this strict, or has it suddenly become stricter recently?

Actually, Yongqi believes it's just one sentence: the economy is not good, the country does not want funds to flow out and also hopes you protect your funds well. Regarding regulation, I analyzed in a previous article: 13 ministries stopped, 7 major associations issued documents, institutions began investigations! Uncle Hat is taking action, 190 million USDT no one dares to claim... detailed analysis has been done.

The core of this farce lies in: when transferring money, noted: Dogecoin.

An unintended joke, or a note, caused both parties' bank cards to be frozen, and they had to explain the situation at the bank and write something.

It's really exhausting!!! But it also reflects three important directions of national regulation:

Attitude One: The regulatory attitude towards virtual currencies remains 'high pressure and strict control'.

Attitude Two: The bank's risk control system is undergoing a comprehensive upgrade and tends to 'rather mistakenly kill'.

Attitude Three: Users' daily behaviors are being incorporated into stricter risk control models.

This is a continuous game of chess between regulators, banks, and users.

Big data: what you did is not important,

But what you 'seem' to have done.

When frozen, the first reaction of the person concerned is confusion: 'I didn't buy or sell any coins, why am I frozen?'

The answer is just one sentence: it’s not about what you did, but what you 'seem' to have done.

So how does the anti-fraud system 'see' you?

You need to understand one thing first: the current anti-fraud and risk control is no longer 'manual judgment', but rather keywords + behavioral models + risk profiles.

It doesn't care whether you are wronged; it only cares: 'Do you meet high-risk characteristics?'

And 'virtual currency related vocabulary' itself is a high-weight risk label in the current regulatory context.

Especially the following combinations: small amounts multiple times or sudden transfers, non-wages, non-fixed transactions, notes contain virtual currency names.

The system logic is very simple and crude: 'Rather mistakenly kill than let go.'

Because in the eyes of banks and the anti-fraud system, freezing an ordinary person is very low cost; letting go of a node in a fraud chain is extremely high cost.

Thus, you become a 'reasonable sacrifice'.

The most frightening aspect: you cannot prove your innocence.

Once the card is frozen, you will discover something even more absurd: you have almost no absolutely effective means to prove your innocence.

It's very simple: if the bank asks you, how do you prove that this fund is not for buying Dogecoin? How do you prove it?

After freezing, banks usually only tell you one thing: 'This is a system risk control, we can't do anything about it.'

The police may ask: what is this money for? Have you participated in virtual currency trading? Have you helped someone with transactions?

Your answer 'no' cannot directly lead to unfreezing.

Because the logic is reversed: you have to prove 'no' instead of them proving 'yes'.

This is the most realistic side of modern financial risk control.

After this incident, what should ordinary people do when transferring money?

Let's be practical.

First: when transferring money, never write: virtual currency, USDT, Bitcoin, Dogecoin.

Even if it is a joke. Otherwise, it could turn serious!!!

Second: do not help others to collect or pay any 'unclear' funds.

Third: once frozen, immediately: keep chat records, clarify the source of funds, communicate proactively, but do not confront.

Fourth: Remember one thing: the system does not discuss emotions; you must discuss strategies, rules, and understand the law.

In the future, a 'more transparent risk control prompt mechanism' may be formed. Amidst the controversy, banks might optimize information prompts, for example:

Automatically remind when inputting sensitive words, provide secondary confirmation before risk triggers, system determines 'not real-time freezing' but 'prompt explanation.'

Otherwise, the continuous occurrences of collateral damage will only exacerbate user dissatisfaction.

In the future, such conflicts will occur more frequently.

For users, the most critical thing is: understand the logic of risk and avoid triggering sensitive systems.

For banks, what's more important is: to find a better balance between strict risk control and user experience.

'If you hate him, just transfer 250 yuan,

Note: Dogecoin.

This phrase became popular not because it is vicious,

But because it reveals a reality: in an era of high risk control, one word can change your identity in the financial system.

You do not need to break the law; you just need to 'look like' it. And this is the most alarming aspect.

The reason this event can ignite emotions is not because everyone likes to watch the excitement.

It's because it touches on a reality: ordinary people are being included in an extremely sensitive financial monitoring system that lacks space for appeal.

You did nothing wrong, but you must pay the cost for 'looking wrong'.

In-depth observation · Independent thinking · Value is more than just price.

Star #WallStreetCryptoIntelligence, good content not to be missed⭐

Finally: many of the viewpoints in this article represent my personal understanding of the market and do not constitute advice for your investment.