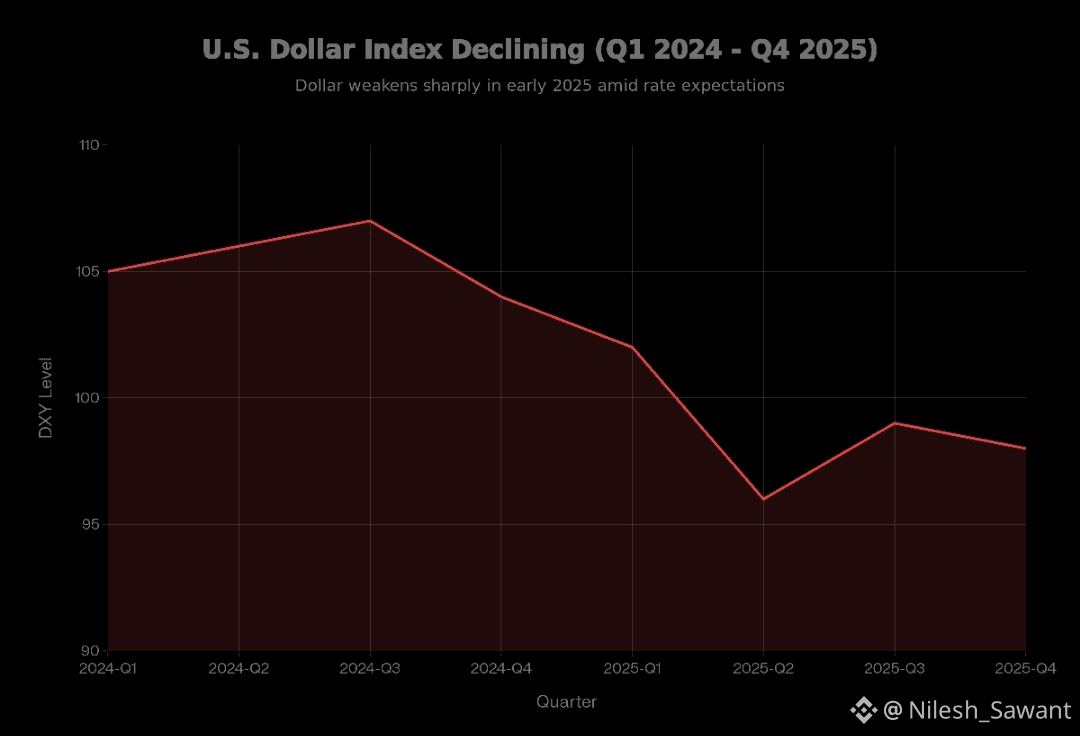

The U.S. dollar has dropped sharply in 2025 but it has not “crashed” or lost its global reserve-currency role, and most analysts see a significant weakening rather than a total collapse. That said, the speed of the decline and policy uncertainty mean individuals and investors should prepare for higher import prices, more volatility, and shifting opportunities in assets like foreign stocks, gold, and real assets. What is happening to the dollar?Major dollar indexes show that 2025 has been one of the worst years for the currency in decades, with the dollar index falling around 10–11% in the first half of the year, its steepest first‑half decline in over 50 years. This drop follows a long bull run from roughly 2010–2024, so part of the move is a reversal of earlier strength rather than an overnight collapse. Several forces are pushing the dollar down at once: aggressive new U.S. tariffs, worries about rising U.S. debt and fiscal policy, and concerns over pressure on the Federal Reserve’s independence and future rate cuts. These factors have made U.S. assets look riskier, encouraged some capital to move abroad, and increased interest in alternatives like gold and other currencies. Current level: context, not apocalypseLive benchmarks such as the DXY index still place the dollar near the high‑90s to low‑100s range, below its 2022 peak but not anywhere near zero. In other words, the dollar has weakened a lot in a short period but remains a strong, widely used currency by historical and global standards. Large banks and institutions broadly expect further pressure and volatility rather than a sudden end to dollar dominance, because there is still no clear alternative with comparable depth, liquidity, and legal infrastructure. At the same time, many warn that sustained deficits, politicized monetary policy, and growing “de‑dollarisation” efforts by some countries could gradually chip away at the dollar’s global role over the long term. Visual: dollar path 2024–2025Below is an illustrative chart of the U.S. Dollar Index (DXY) using approximate quarterly values that capture the recent slide and partial stabilization.

This stylized chart reflects a firm dollar through 2024, a sharp drop in early‑to‑mid 2025, and a modest recovery and stabilization around the high‑90s by late 2025, broadly consistent with reported moves of roughly a 10–11% fall in the first half of 2025 and current index readings near 98. Who gets hurt, who benefits?A weaker dollar affects groups differently, creating both risks and opportunities. U.S. consumers and import‑heavy businesses: Imports become more expensive, so goods like electronics, many household items, and foreign travel can cost more in dollar terms, and margins may get squeezed for retailers that rely heavily on imported stock. If companies pass these costs on, it can add to inflation pressure at home. U.S. exporters and firms earning abroad: A weaker dollar makes American goods and services cheaper to foreign buyers and boosts the dollar value of profits earned overseas, which can support exporters and multinationals. This can partially offset domestic weakness for globally diversified firms. Emerging‑market borrowers and commodity exporters: Countries and companies with dollar debts find those debts easier to service when the dollar falls, while higher dollar‑priced commodity revenues can help nations that export oil, metals, and agricultural products. This is why a weaker dollar often coincides with easier financial conditions in many emerging markets.

How to prepare as an individualWhile no one can predict currency moves with certainty, there are practical steps that help reduce vulnerability to a weaker dollar and broader volatility. Diversify assets: Spread investments across different asset classes (equities, bonds, cash equivalents, real assets) and regions, including some exposure to non‑U.S. markets and currencies through global funds or ETFs. This reduces reliance on any one country’s currency or policy choices. Hedge inflation and currency risk: Consider assets that can benefit from or at least keep up with a weaker dollar and higher prices, such as inflation‑linked securities, select commodities, and high‑quality real estate, sized appropriately for risk tolerance. Some investors also use limited allocations to gold or other precious metals as a hedge, given their historical tendency to rise when confidence in the dollar falls. Strengthen personal finances: In a world of higher borrowing costs and potentially higher inflation, paying down high‑interest debt, maintaining an emergency fund, and locking in fixed rates where sensible can improve resilience. This helps whether the dollar stabilizes, weakens further, or swings violently, since strong personal balance sheets are valuable in any macro environment.