This is the news that all serious investors were waiting for. Far from memes and short-term speculation, the American Congress has just launched a major offensive to integrate Bitcoin into the most sacred savings of Americans: their retirement.

If you thought that cryptos were still reserved for geeks or crazy traders, read on. The very definition of savings 'Good Family Man' is changing before our eyes.

Congress is putting pressure: 'Open the floodgates'

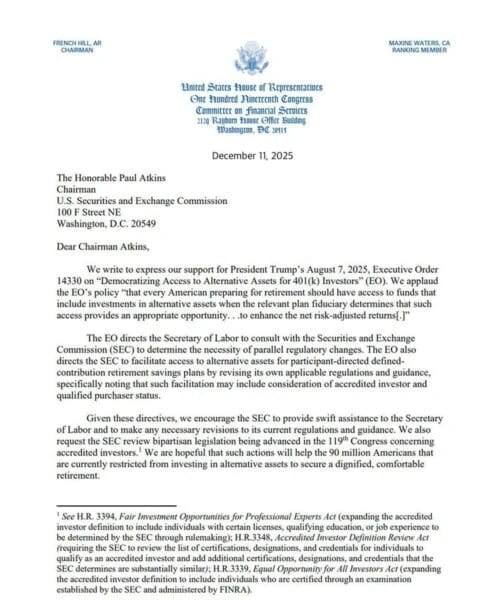

On December 11, an official letter was sent by Congress to Paul Atkins, the chairman of the SEC (the American stock market regulator). The message is clear: it is time to modernize the rules and allow Bitcoin and digital assets in 401(k) plans.

Official letter sent by Congress to Paul Atkins

Official letter sent by Congress to Paul Atkins

Why is this a seismic event? The 401(k) is not a trading account. It is the cornerstone of capitalized retirement in the USA, a colossal market of $12.5 trillion.

By pushing for this integration, lawmakers validate two things:

Bitcoin is now considered a sufficiently mature asset for the very long term.

Ordinary workers (nurses, engineers, teachers) must have the right to access it, and not just ultra-rich 'accredited investors'.

The end of the narrative 'Crypto = Casino'

This initiative follows the executive order from President Trump aimed at 'Democratizing access to alternative assets'. The SEC, under the impetus of Paul Atkins' 'Project Crypto', is already showing signs of openness by moving away from repression towards clear regulation.

For the French investor, the message is harsh: the world is moving forward. While Europe still hesitates, the United States is preparing to direct a portion of global savings towards blockchain.

The uncomfortable question: Will you wait for your French bank to offer you this type of product in 10 years (with exorbitant fees), or will you take the initiative?

What this changes for you

If Congress is fighting to include Bitcoin in retirement plans, it validates a crucial thesis:

Bitcoin is a value-preserving asset in the very long term.

This changes everything. One does not 'play' with their retirement, one builds it.

In the USA, 401(k)s will soon allow holding Bitcoin for 10, 20, or 30 years. However, holding an asset for such a duration without it generating a return is a financial mistake.

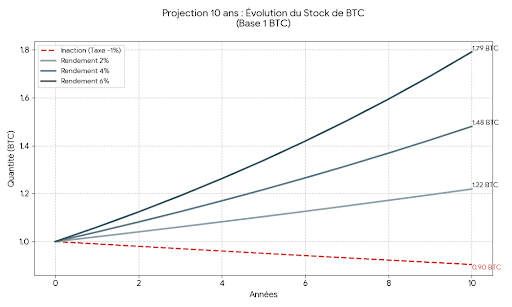

The hidden asset: The mechanics of 60%

This is where you can get ahead of institutions.

If you hold Bitcoin for the long term, you must activate the magic of compound interest.

Mathematically, a modest return of 5% per year on your Bitcoin (via a secure DeFi strategy) transforms your wealth over 10 years:

You do not simply earn 50% (5% x 10 years).

Thanks to compound interest, you accumulate more than 60% additional Bitcoin.

The calculation is simple: 1 BTC invested at 5% for 10 years becomes ~1.63 BTC.

This, without having reinvested a single euro, without trading, and without even counting the rise in Bitcoin's price.

Take the initiative for your retirement

The action of Congress is a green signal. But do not wait for your bank to offer these products in 10 years (with huge fees).

DeFi (Decentralized Finance) allows you, starting today, to apply this 'personal pension fund' strategy:

Secure your assets.

Generate this essential native return.

This is the mission of Club 25%: to make you autonomous in building a strategy capable of aiming for 15 to 25% per year (on stablecoins) and optimizing your crypto positions.

All this while dedicating less than an hour a month, far from the stress of trading.