Liquidation (also commonly referred to as 'forced liquidation' or 'margin call') refers to the situation in leveraged trading when an investor's losses reach a certain level, causing the margin in their account to be insufficient to maintain their position. To protect themselves (to avoid the investor owing money, commonly known as being 'underwater'), the trading platform will forcibly liquidate the contracts held by the investor (regardless of whether they are long or short positions).

Core Principle: Margin and Leverage

To understand liquidation, you must first understand the two core elements of contract trading:

Margin (Margin)

Margin is the collateral that investors use to open and maintain contract positions. You only need to invest a small portion of funds as margin to operate larger amounts of contracts.

Leverage

Leverage is an amplification effect. For example, using 10x leverage, you only need 1,000 USDT of margin to open a contract position worth 10,000 USDT. Leverage greatly amplifies your potential profits but also amplifies your potential losses by the same factor.

How does liquidation occur?

The trading platform will set a **'Maintenance Margin Rate'**. This rate is the minimum fund requirement that your account must always maintain.

The calculation logic for liquidation is as follows:

When the market price fluctuates in the opposite direction of your opening position, your position will incur losses. This loss will be deducted from your **account equity**.

Account equity - initial margin + unrealized profit and loss

When your account equity (net value) falls below the maintenance margin level required by the platform, the platform will issue a forced liquidation notice (Margin Call) and automatically sell your position at the market price.

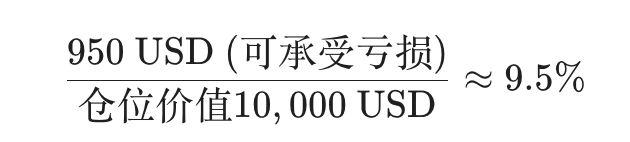

In simple terms: (as shown in the image, Binance's article editor does not support formula rendering)

Consequences: After liquidation occurs, you lose almost all of your initial margin (principal), and you miss the chance to wait for the market to return. (Partial liquidation is better; in full liquidation, you lose all your money.)

Calculation of liquidation point (example explanation)

Assuming:

Current BTC price: 60000 USDT

Your initial funds (margin): 1000 USDT

Your chosen leverage: 10 times

Your opening direction: Long

Position value: 1000*10=10000 USDT (position worth 10,000 dollars)

Platform maintenance margin rate: Assume 0.5% (different platforms and leverage rates vary)

Maintenance margin: 10000*0.5%=50

The maximum loss your account can withstand is: 1000-50=950

Liquidation trigger point:

Your position value is 10000 USDT, a loss of 950 corresponds to a price reversal fluctuation:

This means that when the Bitcoin price drops by about 9.5% from 60000 USDT (i.e., down to about 54300), your position will trigger liquidation.

Differences between liquidation and options trading

Contract (futures) trading: uses leverage, has forced liquidation (liquidation) risk, and potential losses can consume all your margin.

Options buyer trading: does not involve margin leverage and has no liquidation risk. Options buyers pay premiums, and the maximum loss is just the premium, without losing more than the premium amount.

Understanding the liquidation mechanism and strictly enforcing risk management is a prerequisite for conducting contract trading.

What is the liquidation trigger price?

This issue touches on the key differences and roles of 'Mark Price' and 'Last Price' in contract trading.

The mark price is used to determine whether liquidation is triggered;

However, when executing the liquidation operation, the platform must transact at the current market price (i.e., the latest price).

Let me explain in detail the roles of the two and the execution process during liquidation.

Mark Price

The establishment of the mark price is mainly to solve two problems that may arise in the cryptocurrency contract market:

1. Prevent malicious manipulation of market prices

The cryptocurrency market is highly volatile, and liquidity is relatively dispersed. If only the exchange's last traded price is used to calculate profit and loss and determine liquidation, large investors or malicious traders can temporarily raise or lower the price through large buy or sell orders, causing a large number of users' positions to be unreasonably liquidated.

2. Smooth out short-term drastic fluctuations

The contract price can sometimes deviate significantly from the spot price (premium or discount) due to market sentiment or sudden events.

The role of the mark price:

It is calculated based on the spot index price (Index Price, derived from the weighted average of multiple major spot exchanges) and combined with a reasonably moving average premium to reflect the fair value of the contract.

Its function: The platform uses the mark price to calculate your unrealized profit and loss and determine whether your margin level has reached the maintenance margin rate, thus deciding whether to trigger liquidation.

Last Price

The latest price is the most recent transaction price in the contract market, which is the real-time buy and sell price you see on the order book.

The execution process of liquidation (from mark to market price)

When the mark price reaches your liquidation price line, the forced liquidation procedure will immediately start, and the steps are as follows:

Stage 1: Triggering liquidation (based on mark price)

Judging criterion: Your account net value (equity) is below the maintenance margin.

Calculation price: The platform uses the mark price to calculate your current net value and determine if liquidation is triggered.

Stage 2: Executing liquidation (based on latest price/market price)

Execution method: Once liquidation is triggered, the trading platform's risk control system will immediately take over your position and, in the form of a market order, will put your contract position into the trading market for closure.

Transaction price: Since it is executed with a market order, the actual transaction price is the best bid/ask price currently in the market, which is the latest price, or more precisely, the price quoted by the counterparty.

Conclusion: The mark price determines 'when' liquidation should occur; however, when actual liquidation is executed, it must be matched at the market price (latest price) at that time to effectively close your position.

Slippage risk

Under normal circumstances, the gap between the mark price and the latest price is small. However, if the market fluctuates violently or your position is very large, the following issues may arise:

Transaction deviation: Forced liquidation is executed at market orders, and if the market liquidity is poor, the market order may 'consume' many levels of depth on the order book, resulting in your actual closing price being worse than the mark price at the time of triggering liquidation, which is called slippage.

Cross-collateral risk: In extremely rapid market conditions (such as a flash crash), the latest price may instantly skip the mark price, leading to the system not being able to close the position on time. The final closing price is far below the liquidation price, causing your loss to exceed the initial margin, resulting in a cross-collateral situation (i.e., account net value becomes negative).

To cope with cross-collateral risk, many large trading platforms have established **'risk reserves' or 'insurance funds'** to cover potential losses the platform may incur in such situations, ensuring that clients' losses do not exceed their invested margin (provided the platform promises not to distribute the losses).

The next article will discuss:

What is margin?

What is the actual leverage?

What is maintenance margin?

What is margin rate?

Why was there a liquidation before reaching the forced liquidation price?

Why is there still money left in the account after a full liquidation?

What is the liquidation clearing fee?