In the previous tweet, we mentioned that MSTR and ETF are the core forces continuously providing new demand for BTC in this cycle, and they are also important support for the price to continue rising (see citation).

Although on December 9, MSTR announced the purchase of 10,624 BTC again, the frequency and scale have clearly slowed down compared to the active levels from the third quarter of 2024 to early 2025. The recent performance of the ETF side has also been weaker.

This fully demonstrates that under the current macro backdrop, traditional capital's attitude towards BTC is becoming more hesitant and cautious, with an overall decrease in risk appetite. In addition, there is another equally important but easily overlooked reason — basis convergence.

The funds for buying ETFs can generally be divided into two categories:

1. Directional funds: Simply replacing direct holding of BTC with spot ETFs, essentially bullish on BTC;

2. Hedging arbitrage funds: Buying spot ETFs while shorting BTC futures on CME to earn basis income.

When market risk appetite declines, the first type of funds will naturally decrease; while when the basis continues to converge and arbitrage yields decline, the second type of funds will gradually exit.

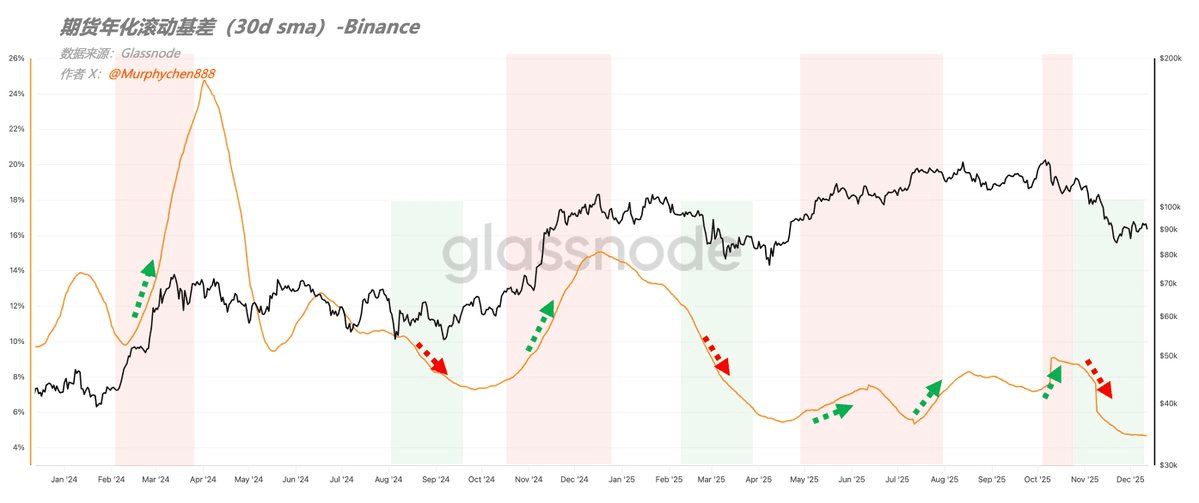

Figure 1 takes the annualized rolling basis of Binance's 3-month futures as an example: In March 2024, the basis yield peaked at 25% (30D SMA); in December 2024, it recovered to about 15%; but currently, it is only 4.7%.

In a typical bull market, a high basis often indicates that the market bulls are willing to buy forward contracts at a high premium, using them as a leverage tool. A continuously declining basis reflects a simultaneous decline in bullish sentiment, risk appetite, and willingness to leverage.

Against this backdrop, the market gradually entered a negative feedback loop:

Bullish sentiment declines → Basis converges → Arbitrage funds exit → ETF purchasing power declines → BTC price comes under pressure → CME hedging short positions take profits → Spot selling under hedge structure → Bullish sentiment further declines

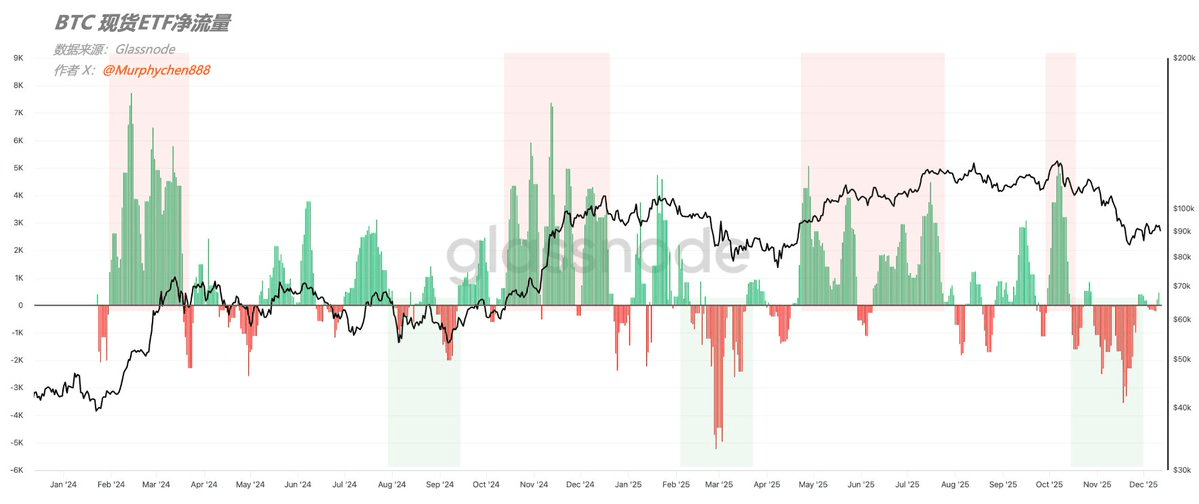

Therefore, in the comparison between Figure 1 and Figure 2, we can see: the red shaded area, where the basis rises, corresponds to a significant net inflow into ETFs; the green shaded area, where the basis falls, corresponds to a continuous net outflow from ETFs.

How can we break this cycle?

In the short term, it is not easy. It requires clearer market expectations for the macro environment, an increase in risk appetite, new demand entering the market, and stronger bullish sentiment, which will naturally bring in money.