Bitcoin is caught in a tug-of-war

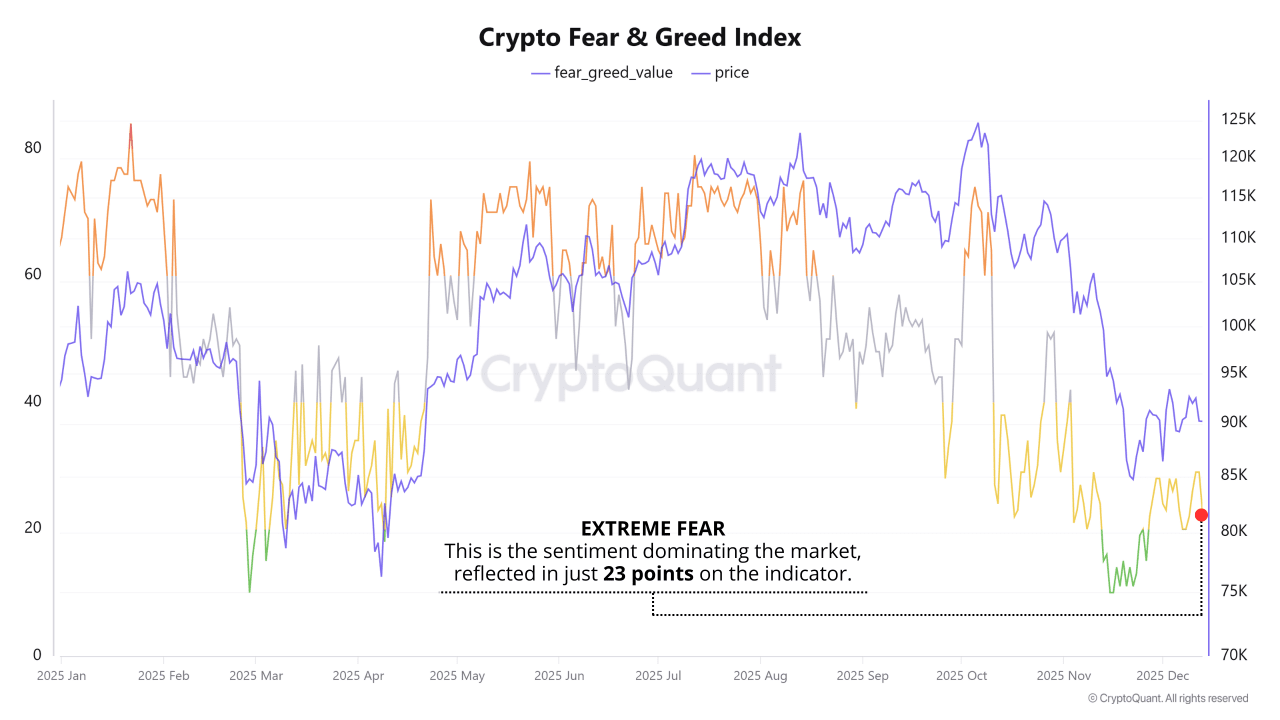

The current Bitcoin, to put it bluntly, is being kept in a "tug-of-war" mode by the macro environment. The price has retraced from 126,000 to 89,000, and the fear index has dropped directly to 23. Although no one is saying it out loud, everyone is feeling anxious inside. The bears have strong reasons: the Bank of Japan is planning to raise interest rates to 0.75%, a height not seen in nearly 30 years. Historically, when the yen tightens, Bitcoin tends to get hit hard; coupled with the fact that U.S. Treasury yields are stubbornly high, global liquidity is continuously being drained, and the deleveraging has conveniently pushed the price down to below 84,000. However, the bulls are not giving up either; the Federal Reserve has ended quantitative tightening, initially injecting 13.5 billion dollars, with the possibility of injecting more later on.

40 billion; institutions are also starting to probe, Vanguard

Launched a crypto ETF, US banks allow a maximum allocation of 4% to Bitcoin. The options market is at 100000–115000

Ten thousand bets on a rebound, spot funds are deadlocked at 80000–85000

Ten thousand chips are being acquired. It's not a crash now, but rather being squeezed in the middle by policies and liquidity 'holding direction'.

New buyers are picking up at low prices

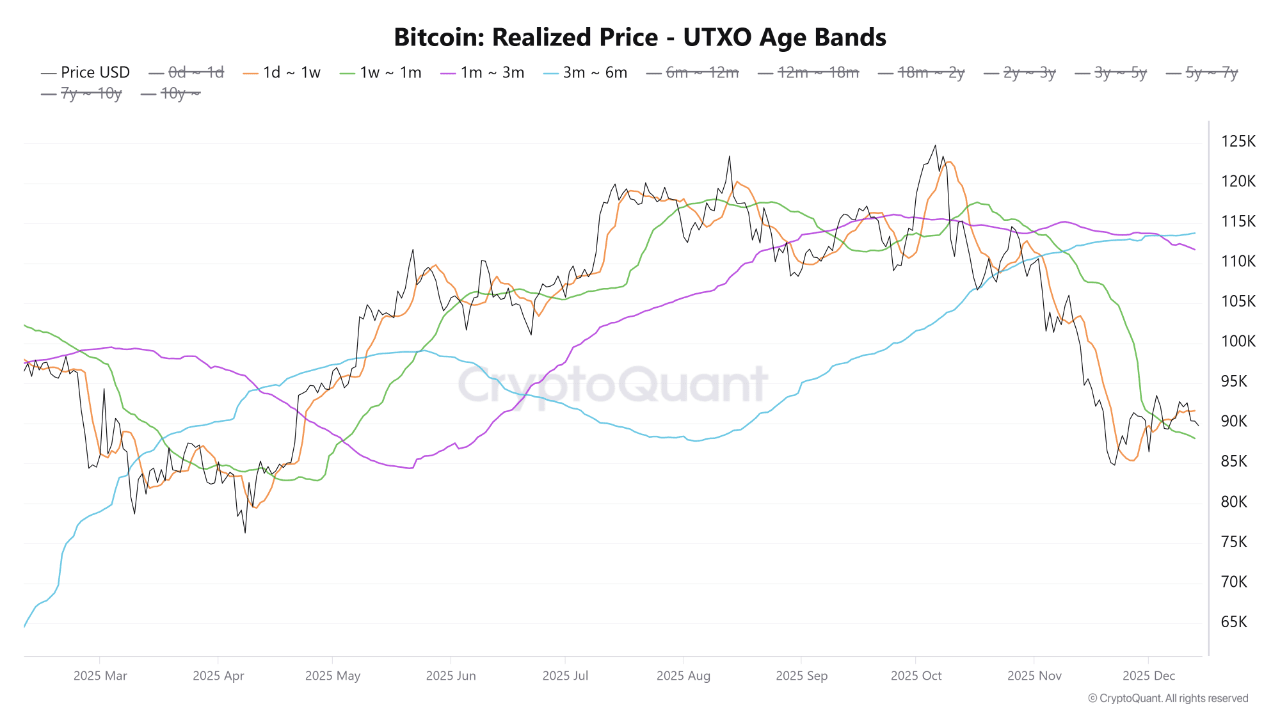

The most significant signal for Bitcoin now is not in the price rise or fall, but in the on-chain 'who has the lower cost'. The latest data is very unusual: new buyers from 1–3 months have a cost that is even lower than that of old buyers from 3–6 months. The normal script should be that new investors take over at a higher price, historically averaging $2500 more expensive, but this time it has flipped. In the entire history, this situation has only occurred 9 times, averaging 145 days, and during this period, the price was particularly volatile, with the most extreme cost difference reaching -19,500 dollars. But don't rush to call it a bear market; this is more like the market 'cramping' rather than 'fracturing'. Chips are transferring from those who can't withstand volatility to those with lower costs and stronger patience, and mid-term holders are not collectively selling at a loss. The current market, to put it simply, is just holding back to strengthen fundamentals, consolidating sideways, compressing structure, rather than sliding into the abyss. No matter how fierce the price disputes are, the on-chain structure is actually improving quietly.

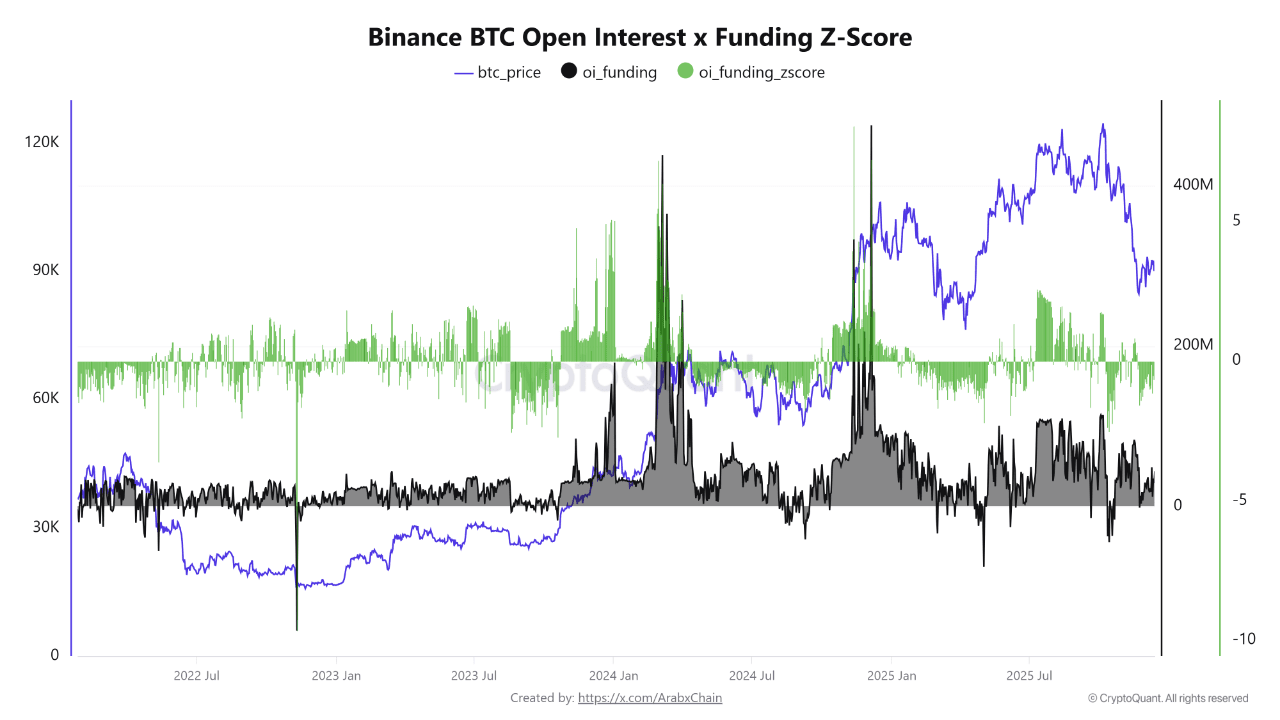

The exit of leverage makes the market more resilient

The current derivatives market for Bitcoin, to put it plainly, is actively lowering leverage. The calculated Z-Score from open interest and funding rates has dropped to -0.28, the signal is very direct: people are not as daring to speculate anymore. In the past, once the Z value turned positive, the market was basically pushed hard by high leverage, rising sharply and falling quickly; now it has reversed, leverage is exiting, and risks are slowly being digested. More crucially, all of this is happening around $90,000, which indicates that this pullback was not caused by forced liquidations but rather the market hit the brakes itself. Such a decline is actually healthy; first, it clears out the easily explodable positions, making it less likely to trigger a chain of liquidations later. In simple terms, it doesn't look stimulating now, but it doesn't seem like an impending crisis either; rather, it feels like making space for the next phase of the market.