Written by: FinTax

In October 2023, the Council of the European Union adopted (EU) 2023/2226 Directive (DAC8), completing the seventh amendment to Directive 2011/16/EU (Directive on Administrative Cooperation in Direct Taxation, DAC), officially incorporating the Organization for Economic Cooperation and Development (OECD) Crypto-Asset Reporting Framework (CARF) into the EU tax cooperation system. In 2025, EU member states will gradually complete the domestic legal transformation of DAC8. On January 1, 2026, the provisions of DAC8 will officially come into effect, marking the start of the first tax information reporting year for crypto assets, leading the European crypto asset market towards substantial implementation.

DAC8 aims to strengthen the overall legal framework of automatic exchange of information (AEOI) by including crypto asset information in the scope of tax information exchange to combat tax fraud, evasion, and avoidance.

1. CARF and DAC8

CARF is an international standard for automatic exchange of tax information promoted by the OECD, aimed at regulating cross-border tax information disclosure related to crypto assets. DAC8 is based on CARF, specifying the rules and procedures for exchanging user information related to crypto assets, and standardizing the service providers and their users active in crypto asset trading through the implementation of due diligence procedures and reporting rules.

1.1 Main Content of DAC8

DAC8 specifies the due diligence and reporting obligations of crypto asset service providers. This directive requires EU countries to obtain information from Reporting Crypto-Asset Service Providers (RCASPs) and exchange that information annually with the taxpayer's EU country of residence. RCASPs need to collect transaction information about their non-resident investors during the reporting year and send this information to the tax authorities of their country within the next calendar year after the reporting year, and exchange information with the tax authorities of the EU countries where non-resident investors reside within 9 months after the end of the reporting year. That is, the information exchange related to the first reporting year (2026) will be completed by September 30, 2027.

Regarding the scope of tax information exchange under DAC8, this directive is based on the definition of cryptocurrencies in the European (Crypto Asset Market Regulation) (MiCA), covering a wide range of crypto assets, including electronic money tokens and some non-fungible tokens.

1.2 Relationship between CARF and DAC8

CARF itself has no legal effect and needs to be implemented through regional or national legislation in various regions and countries. The EU institutionalizes CARF through DAC8, integrating it into the EU legal framework.

DAC8 adopts CARF’s definitions of crypto assets, RCASP, and reportable users, maintaining consistency with CARF in terms of transaction categories, due diligence rules, and reporting data fields. DAC8 transforms CARF into a mandatory, enforceable extra-EU tax transparency mechanism, integrating it with MiCAR and existing DAC tools. DAC8 not only coordinates the EU's tax information exchange but effectively incorporates crypto asset reporting into the EU's fiscal regulatory system.

Additionally, DAC8 makes partial extensions to CARF based on EU characteristics. DAC8 imposes mandatory reporting obligations on non-EU crypto asset service providers when providing services to EU users, making compliance a condition for entering the EU market.

2. Overview of the EU Tax Information Exchange and Regulatory Framework

The EU began issuing a series of DAC directives in 2011. DAC itself does not involve tax collection but establishes a coordinated framework that allows EU member states to collect and exchange tax information related to individuals and companies, to meet the mutual assistance needs of EU countries in the tax field and ensure administrative cooperation between national tax authorities.

2.1 Evolution of the DAC Framework

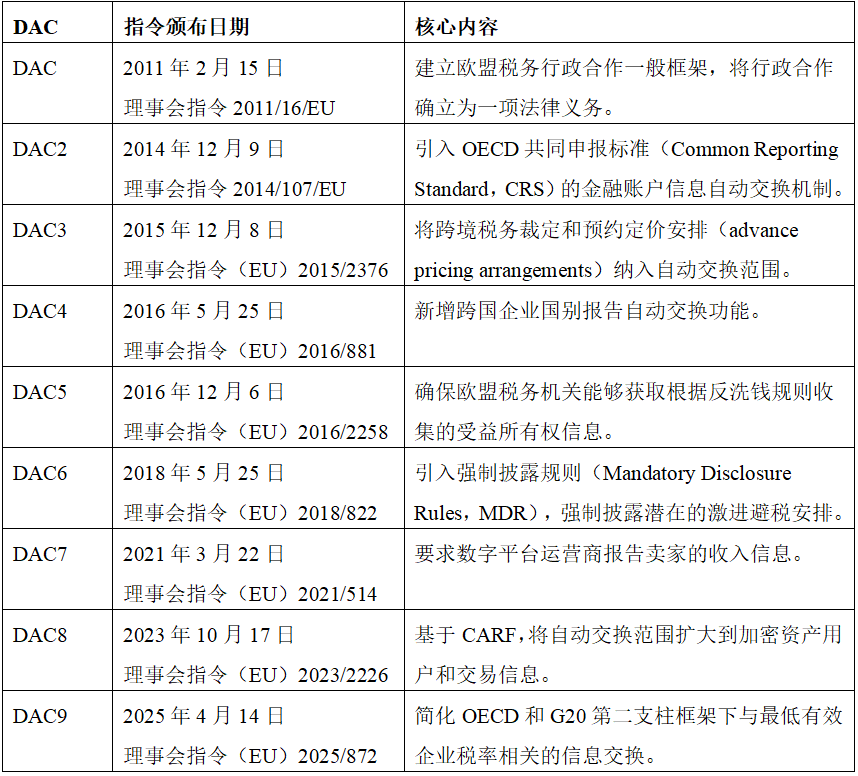

So far, DAC has undergone eight revisions, which expanded the scope of taxpayers and increased the types of data required for reporting. The specific evolution of the DAC system from DAC to DAC9 is shown in the table below:

The evolution of DAC reflects the EU's shift from passive information exchange to proactive, systematic, and technology-driven tax transparency, from traditional income to complex cross-border structures, and the gradual expansion into the digital and crypto economy.

2.2 Positioning of DAC8 in the DAC Framework

DAC8 expands the range of information subject to automatic exchange under the DAC framework, requiring RCASPs to report reportable transaction and transfer information related to crypto assets and electronic money. It ensures that crypto assets follow the same information logic as traditional financial assets, continuing the DAC's tax information exchange framework, improving the asset class coverage, and marking the complete inclusion of crypto assets into the EU's general tax transparency and administrative cooperation system, rather than being regarded as a special or marginal asset class.

Beyond crypto assets, DAC8 further improves some existing provisions of DAC. It refines the reporting and communication rules for Tax Identification Numbers (TIN) to facilitate tax authorities in identifying relevant taxpayers and assessing related tax amounts. At the same time, it grants member states flexibility in penalties and compliance to ensure the implementation of DAC.

3. The Development and Implementation Process of EU DAC8

The formulation and implementation of DAC8 is divided into EU-level and EU member state-level actions, specifically:

3.1 Formation of EU DAC8

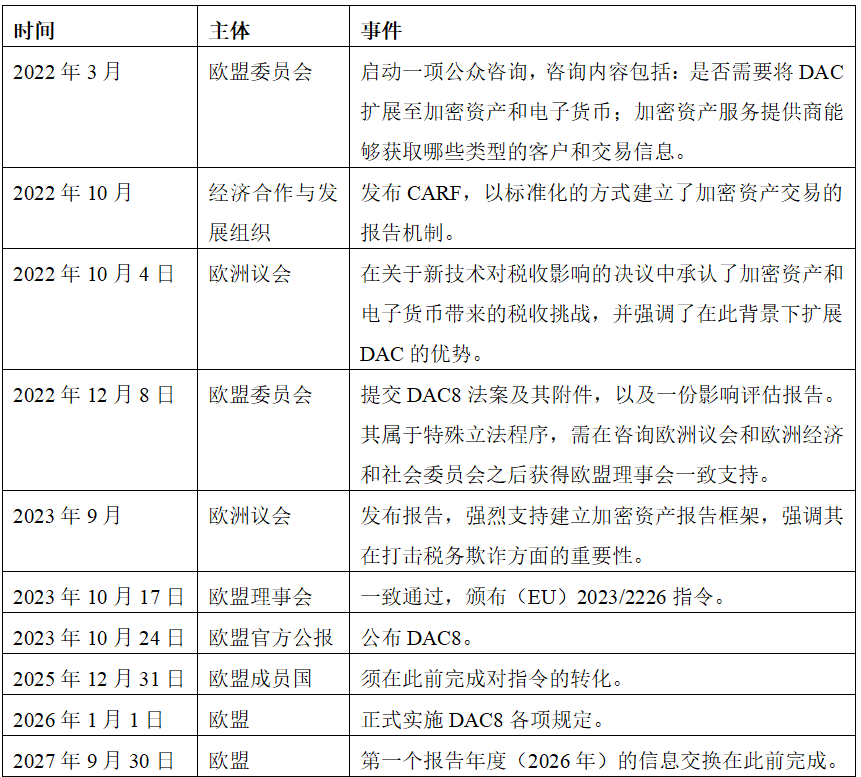

At the EU level, the origins of DAC8 can be traced back to 2022, and the timeline of relevant events for its formulation and implementation is shown in the table below:

3.2 EU Member States' Transposition of DAC8

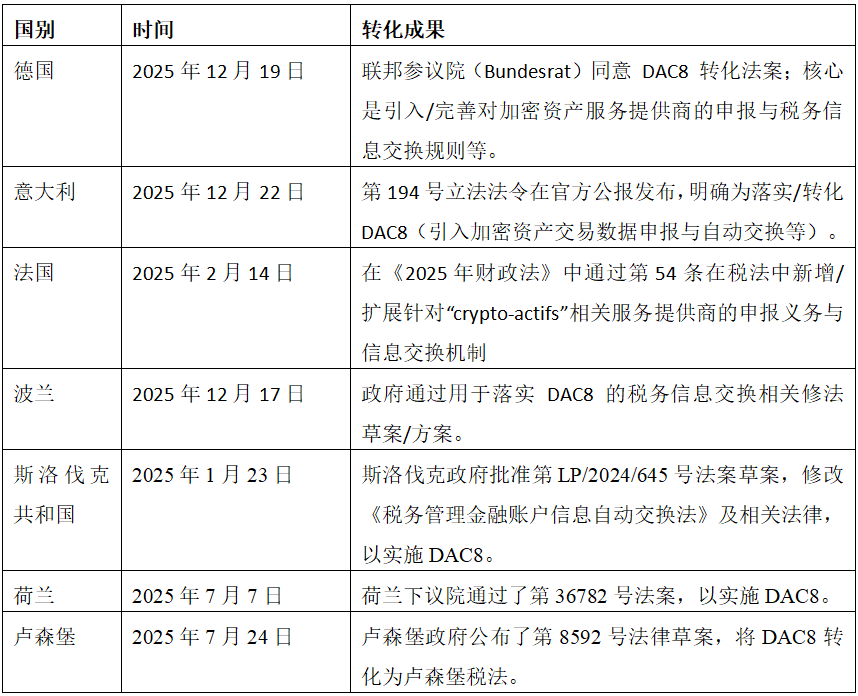

DAC8 sets a transition period for EU member states, requiring them to complete the transposition of DAC8 by December 31, 2025. The transposition results of some member states are as follows:

Overall, at the EU level, DAC8 serves as a tool for building a coordinated and unified system, integrating crypto asset reporting into the existing tax transparency framework of the EU; at the member state level, it is an administrative system oriented towards transposition, influenced by the law enforcement culture, administrative capacity, and policy priorities of each country. The effectiveness of DAC8 depends not only on a unified legal design but also on the ability of member states to transform crypto asset data into effective law enforcement.

4. Potential Impact of DAC8 on the EU Market

4.1 Impact on Cryptocurrency Service Providers

For crypto asset service providers, RCASP is the main channel for information transmission under DAC8. Crypto asset service providers will transform into tax reporting intermediaries, imposed with mandatory obligations to determine client tax residency status, collect tax identification numbers (TIN), and classify transactions, adhering to due diligence rules and submitting annual reports to tax authorities. RCASPs are incorporated into the EU's tax administration system.

DAC8 requires crypto asset service providers to possess IT systems capable of supporting, legal and tax expertise, and ongoing reporting capabilities. This brings high fixed compliance costs, raising the capital threshold for crypto asset service providers. Smaller crypto asset service providers may face mergers or market exit, somewhat accelerating the concentration and specialization of the EU crypto asset market.

DAC8 applies to crypto asset service providers established in the EU and non-EU crypto asset service providers serving EU users, globalizing the EU compliance standards for the crypto asset industry through market access conditions.

4.2 Impact on Traditional Financial Institutions

The implementation of DAC8 will also have an indirect impact on traditional financial institutions, imposing higher risk management requirements on them. This directive incorporates crypto assets into the regulated financial system, making crypto assets a compliance risk factor for traditional financial institutions, forcing them to reassess customers related to crypto assets and strengthen due diligence on clients with high transaction volumes in crypto assets.

4.3 Impact on Individual Investors

DAC8 eliminates the structural tax opacity of crypto assets, requiring the residency status of individual investors, the volume of crypto asset transactions, and cross-border transactions to be reported to tax authorities and automatically exchanged between EU member states. This somewhat increases the compliance burden on individual investors and regulates their cryptocurrency trading behavior.

Additionally, although DAC8 is not retroactive, the data it obtains may trigger audits for previous years. Historical non-compliance in crypto asset trading by individual investors may be reassessed and subjected to penalties.

5. Response and Outlook

In light of the potential impacts brought by the implementation of DAC8, market participants must enhance compliance awareness, work on data integration, and attempt to transform the compliance burden arising from tax transparency in crypto asset transactions into their own competitive and governance advantages. Specifically:

For crypto asset service providers, they need to register in one EU member state or designate an EU reporting intermediary to centralize DAC8 reporting. At the same time, they can try to tag transactions based on asset type, transaction nature, etc., to incorporate tax logic into product design for easier information collection.

For traditional financial institutions, they can collaborate with RCASPs that support DAC8 to carry out risk control related to crypto assets. By leveraging the compliance advantages brought by existing DAC infrastructure, they can develop businesses such as crypto asset brokerage and tokenized securities, re-entering the crypto asset market.

For individual investors, it is essential to fully understand DAC8 and recognize the transparency of crypto asset trading. The attitude towards crypto asset trading should shift from risk avoidance to compliance planning, choosing EU-regulated RCASPs as trading platforms for crypto assets. For historical compliance issues, voluntary disclosure and correction of documents should be considered. If necessary, professional tax advisors' assistance may be sought.

6. Conclusion

The importance of the crypto asset market is increasingly prominent, but the growth in the use of crypto assets should not come at the expense of tax transparency. The implementation of CARF through DAC8 marks a milestone in European crypto asset regulation. The EU incorporates crypto asset reporting obligations into the DAC framework, transforming a non-mandatory international standard into a legally binding, interoperable, and enforceable transparency mechanism. DAC8 eliminates the last major blind spot in European tax information exchange to date, accelerating the normalization of crypto assets as taxable financial instruments, and making the EU a global leader in crypto asset transparency governance.