New macro data from the USA: inflation expectations are cooling, the economy is holding up. For the Fed, this is, if not ideal, then a good mix. However, let's emphasize right away that such data alone is insufficient; a trend is needed.

First to the numbers, then to the conclusions:

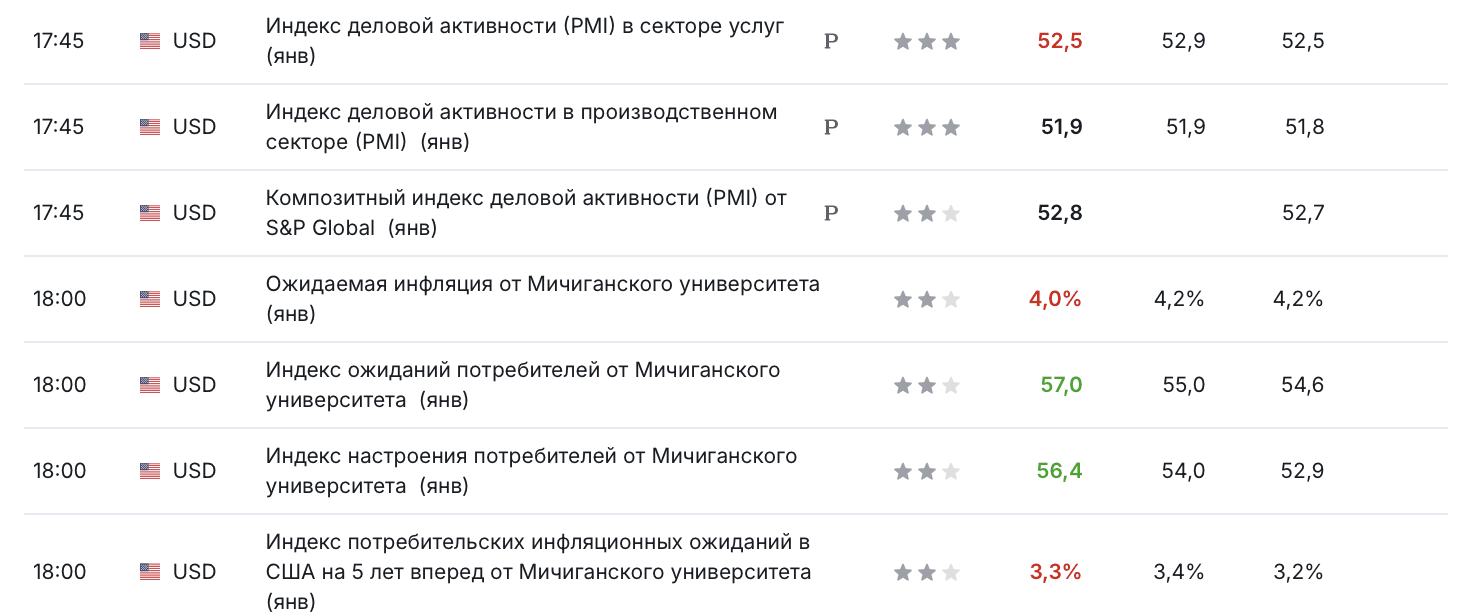

- Business Activity Index (PMI) in the services sector (January): 52.5 against a forecast of 52.9 and a previous figure of 52.5.

- Manufacturing sector business activity index (PMI) (January): 51.9 against a forecast of 51.9 and a previous figure of 51.8.

- Composite business activity index (PMI) from S&P Global (January): 52.8 against a previous figure of 52.7.

- Expected inflation from the University of Michigan (January): 4.0% against a forecast of 4.2% and a previous figure of 4.2%.

- Consumer expectations index from the University of Michigan (January): 57.0 against a forecast of 55.0 and a previous figure of 54.6.

- Consumer sentiment index from the University of Michigan (January): 56.4 against a forecast of 54.0 and a previous figure of 52.9.

- Consumer inflation expectation index in the USA for 5 years ahead from the University of Michigan (January): 3.3% against a forecast of 3.4% and a previous figure of 3.2%.

The data package for January provided the market with a rare combination - business activity remains in the positive, while consumer inflation expectations are decreasing. Business activity in the services sector (key for the USA) is slightly weaker than expected, but the main thing is that it is not declining. Services remain in a growth zone, which means the American economy is not sliding into recession. In the manufacturing sector, it is exactly according to plan and even with a slight improvement. Industry hints at an exit from stagnation, without overheating.

Data from the University of Michigan (which, as acknowledged by the head of the US Federal Reserve, Powell, they consider but do not prioritize) provide the greatest positivity regarding inflation expectations. Consumer inflation fears are decreasing, and this is exactly what the Fed would like to see. AT THE SAME TIME, the indices of expectations and sentiments show that consumers are beginning to believe in "normal life" again. And consumers in the USA account for half of the economy. Increased confidence reduces the risk of a hard landing. Plus, belief in a normal life leads to readiness, capability, and desire to invest in risky assets.

For the cryptocurrency market, all of this together is not exactly a full risk-on. But it's positive. Especially if these data are further confirmed by new ones (including from other sources) and form a trend.