Bitcoin’s major decline occurred before USDe price deviations, indicating USDe did not initiate the October 10 market crash.

USDe price dislocation remained largely isolated to one exchange and did not propagate across the broader market.

Exchange infrastructure stress, API disruptions, and rigid liquidation mechanisms amplified volatility and drove cascading liquidations.

A DELAYED DEBATE THAT EXPOSED A DEEPER DIVIDE

The sharp market crash on October 10 should have faded into history, like many previous episodes of extreme volatility. Prices eventually stabilized, and attention moved on.

Instead, months later, the event returned to the center of industry discussion. This time, the focus was not price, but responsibility.

OKX founder and CEO Star Xu publicly argued that the crash was not accidental. In his view, Binance’s yield campaign around Ethena’s USDe, combined with its collateral treatment, created structural leverage that amplified market stress and triggered cascading liquidations.

Dragonfly partner Haseeb Qureshi strongly rejected this explanation. He argued that the narrative fails on both timing and cross exchange transmission, and that it misidentifies correlation as causation.

As Binance founder Changpeng Zhao and Ethena founder Guy Young joined the discussion, the debate evolved into a broader question. Was the October 10 crash driven by risky product design, or by infrastructure failure under extreme stress?

The answer matters. It determines what the industry chooses to fix next.

THE OKX ARGUMENT: STRUCTURAL LEVERAGE AS THE ROOT CAUSE

Star Xu’s position can be summarized clearly. Yield incentives combined with incorrect collateral classification created systemic leverage.

According to this view, Binance offered temporary high yield on USDe while allowing it to function as margin collateral with treatment similar to USDT and USDC. This design encouraged users to view USDe as a low risk asset.

However, USDe is not a traditional fiat backed stablecoin. It is a synthetic dollar product supported by hedging and trading strategies. Its stability depends on execution conditions and market structure, not only on reserves.

Star Xu described a leverage loop that emerged from this setup. Users converted stablecoins into USDe to earn yield. They then used USDe as collateral to borrow stablecoins, which were again converted into USDe. This cycle repeated.

As long as markets were calm, the loop appeared profitable and safe. Reported yields increased, and risks remained hidden. But when volatility arrived on October 10, the accumulated leverage turned fragile. Liquidations accelerated, and USDe price deviations became part of a broader cascade.

In this narrative, the crash was not caused by a single shock, but by leverage that had been quietly built into the system.

THE TIMING AND TRANSMISSION PROBLEM

Haseeb Qureshi’s rebuttal focused on facts that challenge this story.

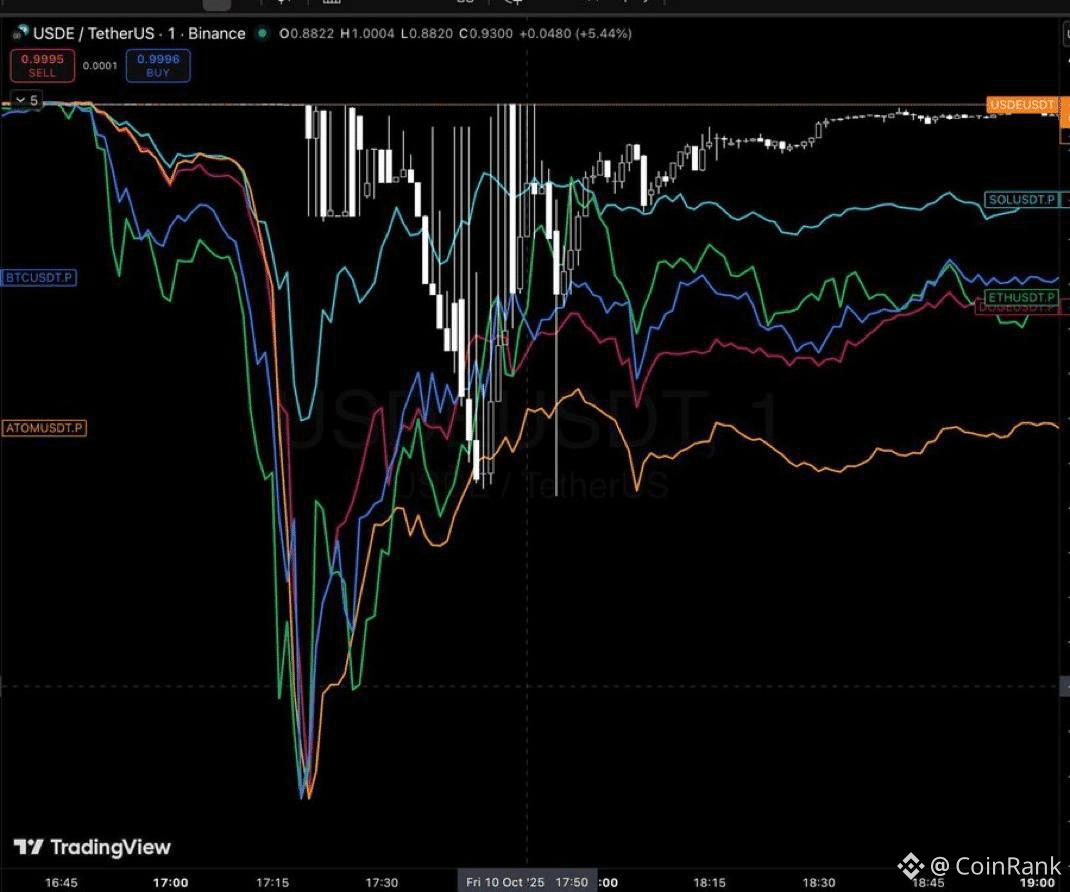

First, the timeline does not align. Public data shows that Bitcoin’s sharp decline and local bottom occurred roughly thirty minutes before USDe showed significant price deviation on Binance. This suggests that the major market move was already underway before USDe became unstable.

If USDe reacted after the primary sell off, it is difficult to argue that it initiated the crash.

Second, the scope of impact was limited. USDe price deviations were largely confined to Binance’s order book. Other major venues did not experience the same dislocation. A true systemic trigger would normally propagate across platforms.

Previous systemic failures such as Terra, Three Arrows Capital, or FTX affected balance sheets everywhere. USDe did not produce a similar global effect.

From this perspective, USDe appears less like the source of the fire and more like one of the first assets to show stress after the system had already begun to fail.

A MORE PLAUSIBLE EXPLANATION: INFRASTRUCTURE FAILURE UNDER STRESS

Rather than a simple cause, Haseeb Qureshi proposed a layered explanation that better fits market mechanics.

The initial shock came from outside crypto. Political and macro uncertainty spiked, and crypto markets were among the few risk assets still trading at full speed.

Trading volume surged. At the same time, key exchange infrastructure struggled. API availability and execution reliability degraded at critical moments. This impaired market makers’ ability to rebalance inventory across venues.

Without functioning arbitrage, prices diverged. Liquidation engines continued to operate mechanically, even as liquidity disappeared. Automatic deleveraging mechanisms further disrupted hedging flows.

In this environment, market makers could no longer act as buyers of last resort. Altcoin markets, which are highly path dependent, entered a vacuum. Once price discovery broke, declines became structural rather than incremental.

Within this framework, USDe was not irrelevant. But it functioned as an early stress indicator inside an already unstable system, not as the original trigger.

WHO WAS RIGHT AND WHO WAS NOT

Based on timing, transmission, and market structure, the weight of evidence favors Haseeb Qureshi’s interpretation of the October 10 crash.

This does not mean Star Xu identified a false risk. Leverage loops driven by yield incentives are real and dangerous. They deserve scrutiny.

However, elevating that risk into the primary cause of the October 10 crash overstates its role. The data does not support USDe as the initiating factor.

The more credible conclusion is that infrastructure failure and liquidation mechanics under extreme conditions played the dominant role. Binance’s responsibility, therefore, lies more in system reliability than in the existence of a yield campaign itself.

These are different categories of responsibility, and they imply very different fixes.

WHY THIS DEBATE MATTERS

The significance of this debate is not about assigning blame. It is about choosing the correct lesson.

If the industry concludes that the problem was simply USDe or similar yield products, it may avoid deeper reforms. The more uncomfortable truth is that crypto markets still lack robust stabilizing mechanisms during stress.

Liquidation systems are designed to minimize platform losses, not to protect market integrity. API resilience, liquidity backstops, and volatility buffers remain underdeveloped.

October 10 was not an anomaly. It was a stress test that arrived earlier than expected.

Understanding its true cause will determine whether the next shock becomes manageable, or catastrophic.

〈The October 10 Crash Revisited: Was USDe the Cause, or a Misplaced Blame?〉這篇文章最早發佈於《CoinRank》。