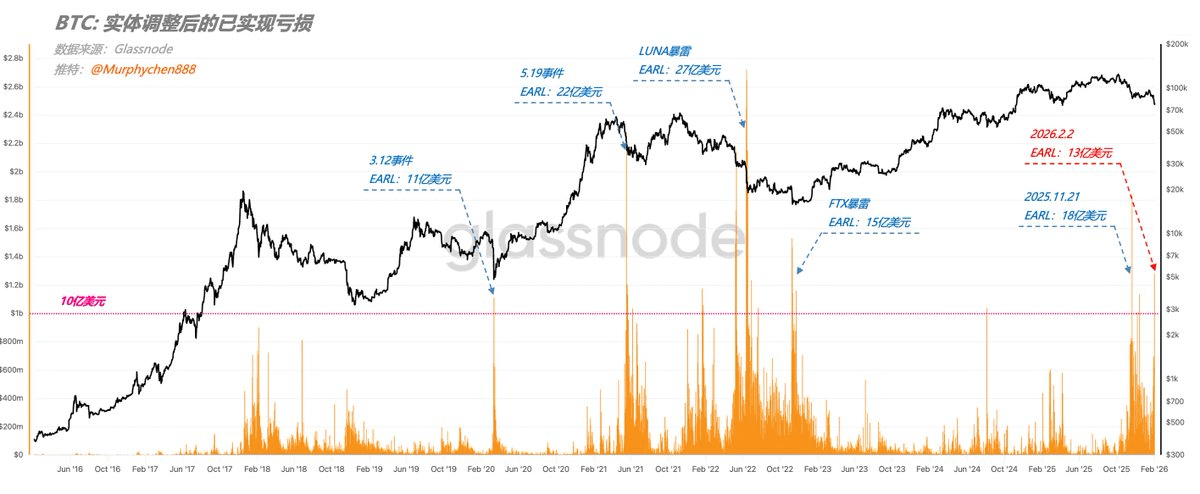

On February 2, the on-chain 'Entity Adjusted Realized Loss (EARL)' for BTC — excluding internal transfers between the same entity — reached as high as $1.3 billion.

Although it is much smaller than the $1.8 billion EARL generated when BTC plummeted to $85,000 on November 21, 2025, it is still not insignificant. Even in the past ten years, the number of days when BTC's daily EARL exceeded $1 billion is limited.

It can only be under a bearish market background that so many fearful sellers are forced to sell. However, the clearing of panic selling can also provide BTC, which is in a downtrend, with a hard-won opportunity to breathe. Reduced selling pressure is conducive to a temporary stabilization in the short term, which naturally creates expectations for a rebound.

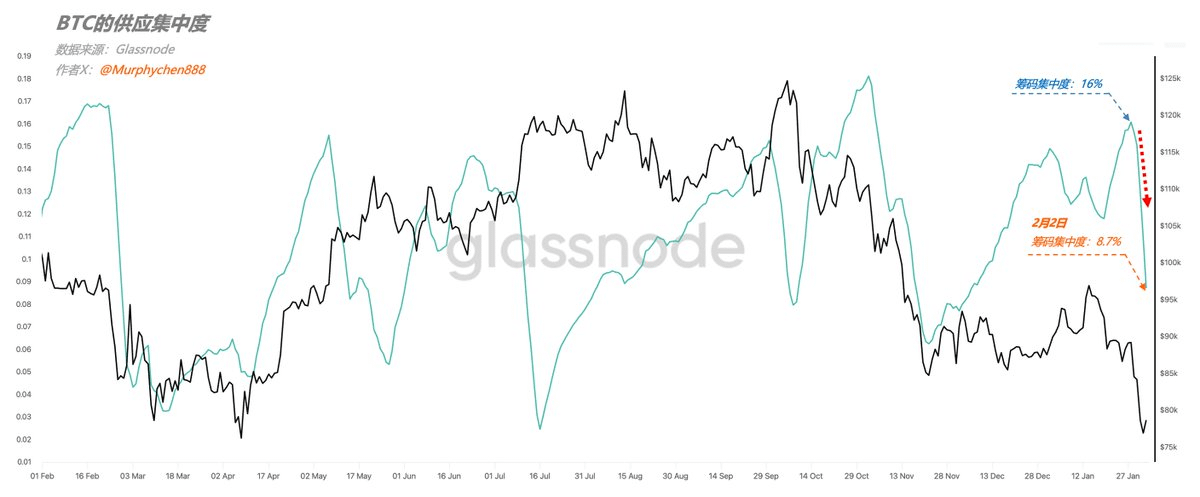

Additionally, as the concentration of BTC holdings has decreased from 16% on January 28 to 8.7% yesterday, it indicates that the probability of significant price fluctuations caused by overly dense chip structures is decreasing.

Of course, there are many factors that amplify fluctuations, including contract leverage liquidations, options Short Gamma status, market liquidity shortages, and so on, while the concentration of holdings is just one of them (here it is emphasized that fluctuations caused by this reason, not that other reasons won't cause fluctuations).

The fluctuations are decreasing, and the panic selling is all about stabilizing the price. The short-term rebound creates favorable conditions, but whether it is strong or weak is another matter, as it still depends on how much demand and momentum there are.