As the cryptocurrency market undergoes a correction, how are institutional investors across the Asia-Pacific region viewing current conditions?

One useful reference is Amber Group, the Singapore-based digital asset financial group providing institutional trading, market-making, and asset management services across APAC.

According to Amber Group’s latest report, the dominant theme is “higher rates for longer.”

Stronger-than-expected U.S. employment data has reduced expectations for Federal Reserve rate cuts, pushing Treasury yields and the U.S. Dollar Index higher. In response, investors have reduced exposure to risk assets, and Bitcoin briefly approached the $60,000 level.

Institutional demand is also slowing. Spot Bitcoin ETFs, which supported much of the market earlier this year, have continued to see net outflows.

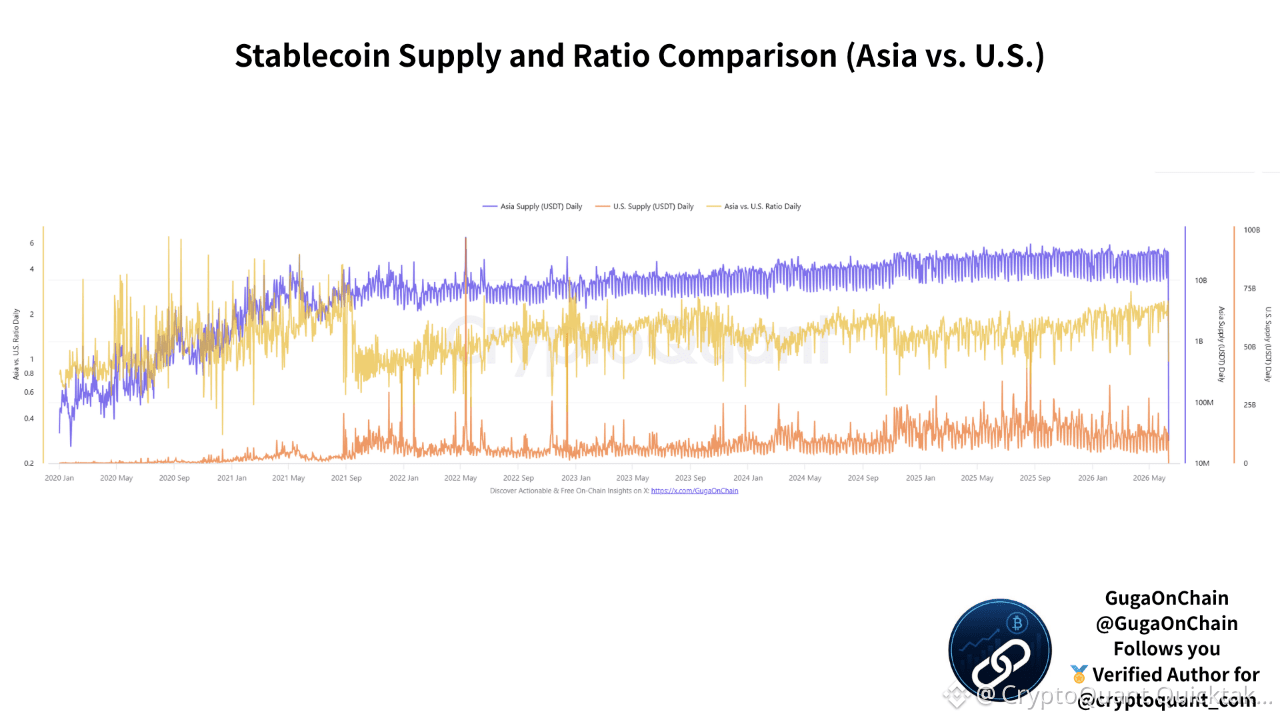

At the same time, XWIN’s on-chain analysis highlights a different trend. USDT supply during Asian trading hours has steadily increased and now rivals—or even exceeds—that of U.S. trading hours.

While crypto liquidity was largely U.S.-driven in 2020, the market may be gradually shifting toward a more Asia-centered liquidity structure.

Meanwhile, digital asset infrastructure continues to advance across APAC. Hong Kong is expanding tokenized bond initiatives, Japan is exploring blockchain-based finance, and South Korea is accelerating stablecoin development.

Although market sentiment remains weak in the short term, the long-term foundations of the digital asset ecosystem continue to strengthen. Going forward, investors should watch not only ETF flows, but also interest rates, dollar liquidity, and capital formation across Asia.

Written by XWIN Japan